Written by:

- Weekly Outlook

- April 24, 2026

- 5 min read

Central Banks Hold Steady as Growth Signals Diverge

Next week brings a dense economic calendar across developed markets, with a strong focus on central bank decisions and key growth and inflation indicators. While markets have spent much of the past month debating the timing of future rate moves, the coming week is more likely to reinforce a different narrative: patience.

Across the US, eurozone, UK, and Canada, policymakers are widely expected to hold rates steady, reflecting a shared uncertainty about the balance between slowing growth and persistent inflation pressures—particularly those linked to energy markets and global geopolitical developments.

At the same time, incoming data—especially US GDP and eurozone inflation—will provide important signals on whether the global economy is stabilising, softening, or beginning to reaccelerate.

United States: Policy Decision (Wednesday) & GDP Release (Wednesday)

The spotlight in the US will fall on both the Federal Reserve decision (Wednesday) and the advance estimate of first-quarter GDP (Wednesday).

The Federal Reserve is expected to leave interest rates unchanged in what should be a relatively uneventful meeting. Policymakers continue to highlight downside risks to employment, while also acknowledging that inflation progress may be slower than expected.

Markets should expect a continuation of the Fed’s “wait-and-see” stance, with little indication of any imminent policy shift.

On the data side, Q1 GDP (Wednesday) is expected to rebound to around 2.5–3.0% annualised, following a weak 0.5% print in Q4 2025.

- Government spending should bounce back after prior disruptions

- Business investment, especially in tech, remains strong

- Net trade is likely neutral

- Consumer spending may be softer due to weather effects

- Housing continues to drag

In addition, the Fed’s preferred inflation gauge, core PCE, may tick slightly higher—reinforcing expectations that policy will remain unchanged in the near term.

Eurozone: Data Releases (Thursday) & ECB Decision (Thursday)

Thursday will be a key session for the eurozone, with GDP (Thursday), inflation (Thursday), and unemployment (Thursday) all released ahead of the rate decision.

The European Central Bank is expected to hold rates steady, with policymakers signalling no urgency to act given the current data backdrop.

- Q1 GDP (Thursday): Likely to show modest growth, reflecting conditions before the recent energy price surge

- Inflation (Thursday): Expected to rise, driven primarily by energy

- Unemployment (Thursday): Expected to remain broadly stable

The key risk for markets is whether higher headline inflation begins to feed into core prices, although evidence of this remains limited for now.

United Kingdom: BoE Rate Decision (Thursday)

The Bank of England is expected to keep rates unchanged in an 8–1 vote on Thursday.

Recent communication from Governor Andrew Bailey suggests that markets may have been too aggressive in pricing further tightening, and the Bank is unlikely to strongly validate those expectations at this stage.

Instead, the focus will remain on:

- Persistent inflation risks

- Elevated economic uncertainty

- A potentially more divided Monetary Policy Committee

While internal disagreements may become more visible over time, the immediate outlook points to continued caution.

Canada: BoC Rate Decision (Wednesday)

The Bank of Canada is expected to leave its policy rate unchanged at 2.25% on Wednesday.

The domestic backdrop remains relatively stable:

- Inflation is broadly in line with target

- The labour market is stabilising

- Growth remains moderate

Although markets are pricing in a possible rate hike later this year, the base case remains that the Bank of Canada will stay on hold through 2026.

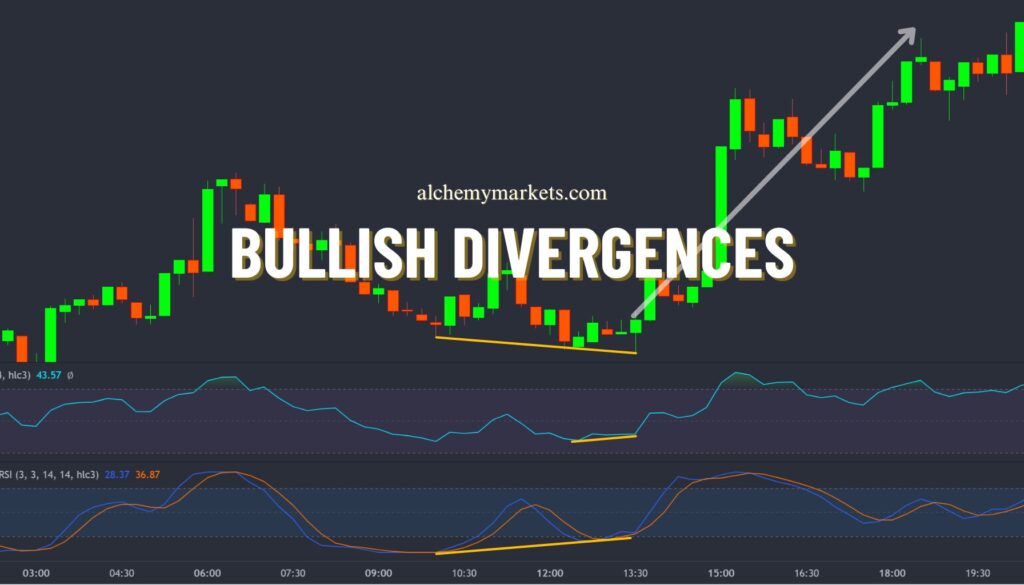

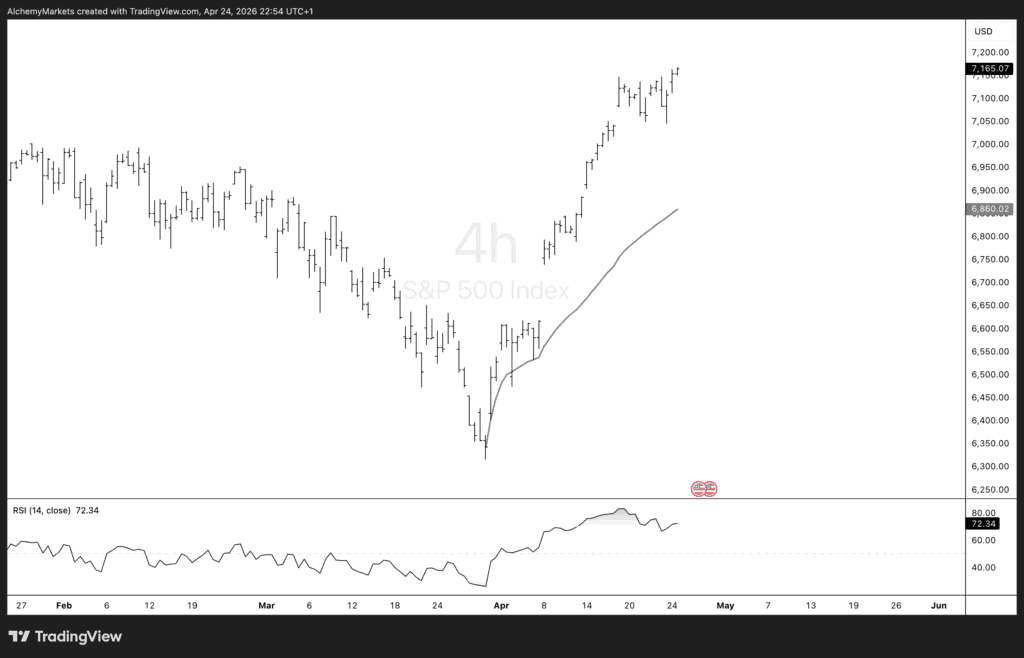

Technical Analysis: S&P 500 (SPX) – Momentum Divergence Signals Exhaustion

From a technical standpoint, the S&P 500 continues to trade in a strong short-term uptrend on the 4-hour timeframe, with price action printing a clear sequence of higher highs and higher lows since the March 30th low (~6,320 area).

However, the structure is now showing clear signs of late-stage trend behaviour.

Price Structure & Trend

- The rally from late March has been impulsive and steep, with minimal retracement phases

- Price is now extending well above the rising trend support (AVWAP on chart)

- Recent candles show compression near highs (~7,150–7,200 zone), indicating slowing upside momentum

This type of price action—strong trend followed by tight consolidation near highs—often precedes either:

- A final exhaustion push, or

- A breakdown into corrective structure

RSI Divergence (Key Signal)

The most important technical development is the bearish divergence on the Relative Strength Index (14):

- Price: Continuing to print higher highs

- RSI: Failing to confirm, instead printing lower highs

- Current RSI reading remains elevated (~72), still in overbought territory

This divergence signals that:

- Momentum is weakening beneath the surface

- Buying pressure is no longer accelerating with price

- The trend is becoming increasingly fragile

Historically, this setup often leads to:

- Short-term pullbacks, or

- A transition into range-bound consolidation

Momentum & Positioning

- RSI has rolled over slightly from recent peaks, reinforcing loss of momentum

- The move into overbought territory has been sustained, increasing mean-reversion risk

- The rally has lacked deep pullbacks, suggesting positioning may be stretched

Key Levels to Watch

- Resistance:

- 7,150 – 7,200 (current highs / rejection zone)

- Initial Support:

- ~7,000 (psychological + minor structure)

- Stronger Support:

- 6,850 – 6,900 (prior consolidation + trend support zone)

A break below initial support would likely confirm a loss of short-term trend control, opening the door to a deeper retracement.

Technical Outlook

While the broader trend remains intact, the current setup suggests the rally is running out of steam:

- Momentum divergence is a leading warning signal

- Price is extended from trend support

- Upside follow-through is becoming less convincing

Our base case is for:

- Near-term consolidation, or

- A corrective pullback toward trend support

This is not yet a confirmed reversal, but the risk/reward for chasing upside at current levels appears increasingly unattractive.