Written by:

- Weekly Outlook

- May 8, 2026

- 7 min read

The Central Bank Narrative May Be Shifting Again

Markets Are Repricing the Fed — But Are They Looking at the Right Inflation Story?

Over the past two weeks, markets have aggressively shifted back toward a more hawkish central bank outlook.

The catalyst has been straightforward:

- Rising geopolitical tensions

- A sharp rebound in oil prices

- Renewed concerns about inflation persistence

Only a few weeks ago, markets were confidently pricing multiple rate cuts for later this year. Now, expectations have shifted materially higher, with cuts being pushed further into the future and some traders even reopening the discussion around additional tightening risks.

But the key question heading into this week is whether markets are reacting to the right inflation driver — or potentially overestimating the persistence of this latest energy shock.

Why This Oil Spike May Be Different From 2022

The current market narrative assumes that higher oil prices automatically translate into broader inflation pressure and therefore force central banks to remain restrictive for longer.

That logic makes sense on the surface.

However, this environment still looks materially different from the 2022 energy crisis.

Back then, the inflation shock was not driven by crude oil alone. Europe experienced a full-spectrum energy crisis as:

- Natural gas prices exploded higher

- Electricity prices surged

- Industrial energy costs skyrocketed

- Consumer inflation expectations became unanchored

That broader energy transmission mechanism created persistent inflation pressure across nearly every sector of the economy.

This time, however, the picture is more contained.

While crude oil prices have moved sharply higher due to geopolitical tensions, natural gas prices remain relatively stable compared with the extreme levels seen in 2022.

That distinction matters enormously for central banks.

Policymakers are not simply reacting to oil prices in isolation. What they care about is whether higher energy prices begin feeding into:

- wages

- consumer inflation expectations

- services inflation

- and broader demand-side inflation pressures

So far, that transmission effect still appears limited.

Growth Beneath the Surface Still Looks Softer

At the same time, several underlying economic indicators continue pointing toward slower growth conditions beneath the headline data.

The US labour market still appears resilient at first glance, but internally the picture is becoming less convincing.

Several softer trends continue developing:

- Job openings continue declining

- Hiring activity has slowed

- Temporary employment remains weak

- Wage growth momentum has moderated

- Job gains are increasingly concentrated in healthcare and government sectors

This creates an important divergence in market expectations.

Right now:

The market narrative

focuses on:

- sticky inflation

- stronger headline employment data

- rising oil prices

- and higher-for-longer central bank policy

The alternative narrative

suggests:

- growth is gradually slowing

- labour demand is weakening

- inflation outside energy remains contained

- and central banks may still eventually pivot back toward cuts later this year

That tension will likely define market direction over the next several months.

The UK Faces a Similar Dynamic

The Bank of England is facing many of the same concerns.

Markets have aggressively repriced UK rate expectations higher because Britain remains highly sensitive to energy shocks.

But again, the current backdrop differs significantly from 2022.

Natural gas prices have not experienced the same type of parabolic move that previously triggered the broader UK inflation spiral.

That weakens the argument for the Bank of England needing to tighten aggressively again.

If inflation expectations remain relatively anchored while growth continues slowing, markets may eventually need to reverse some of this hawkish repricing.

The Real Market Battle: Temporary Shock or Structural Inflation?

The biggest macro question now is whether this latest oil surge becomes:

Scenario 1: A Temporary Geopolitical Shock

or

Scenario 2: A Broader Inflation Regime Shift

That distinction will likely determine:

- the direction of bond yields

- whether rate cuts return later this year

- whether growth and technology stocks continue outperforming

- and whether broader risk appetite can remain elevated into the second half of the year

If inflation expectations remain contained, central banks may tolerate temporarily elevated oil prices without tightening further.

But if energy prices remain elevated long enough to impact consumer behaviour and inflation psychology again, markets may ultimately be correct to expect a more hawkish policy path.

Economic Calendar: Key Events This Week

Tuesday — Inflation Report (CPI)

Markets are expecting another strong headline inflation print.

Consensus Expectations

- Headline CPI: +0.9% MoM

- Core CPI: +0.3% MoM

- Core annual inflation expected to rise toward 2.7%

The primary drivers are expected to be:

- Higher gasoline prices

- Rising diesel prices

- Increased airline fares

- A rebound in medical care and recreation services

However, the broader view remains that this inflation acceleration may still prove temporary if underlying demand conditions continue weakening.

The critical market focus will be whether inflation broadens beyond energy-related categories.

Thursday — Retail Sales

Retail sales may appear stronger at the headline level primarily because gasoline prices mechanically boost nominal spending figures.

However, underlying discretionary demand may remain softer.

Potential areas of weakness:

- autos

- discretionary retail

- consumer goods spending

Markets will watch closely for signs that consumers are beginning to pull back under higher financing costs and slower income growth.

Friday — Industrial Production

Industrial production is expected to rebound modestly, helped by continued strength in manufacturing activity and stabilization within supply chains.

The ISM manufacturing data has recently shown signs of resilience, though broader industrial momentum still remains mixed.

Major Central Bank Event: Powell’s Final Week

One of the most important developments this week is political and symbolic.

Jerome Powell enters his final days as Federal Reserve Chair before Kevin Warsh officially takes over on Friday, May 15.

Markets will be closely monitoring:

- Powell’s final communication tone

- whether he reinforces patience on cuts

- and how the transition to Warsh may shift future policy expectations

Any signal that the incoming leadership may tolerate higher inflation or prioritize growth stabilization differently could materially impact yields, equities, and the dollar.

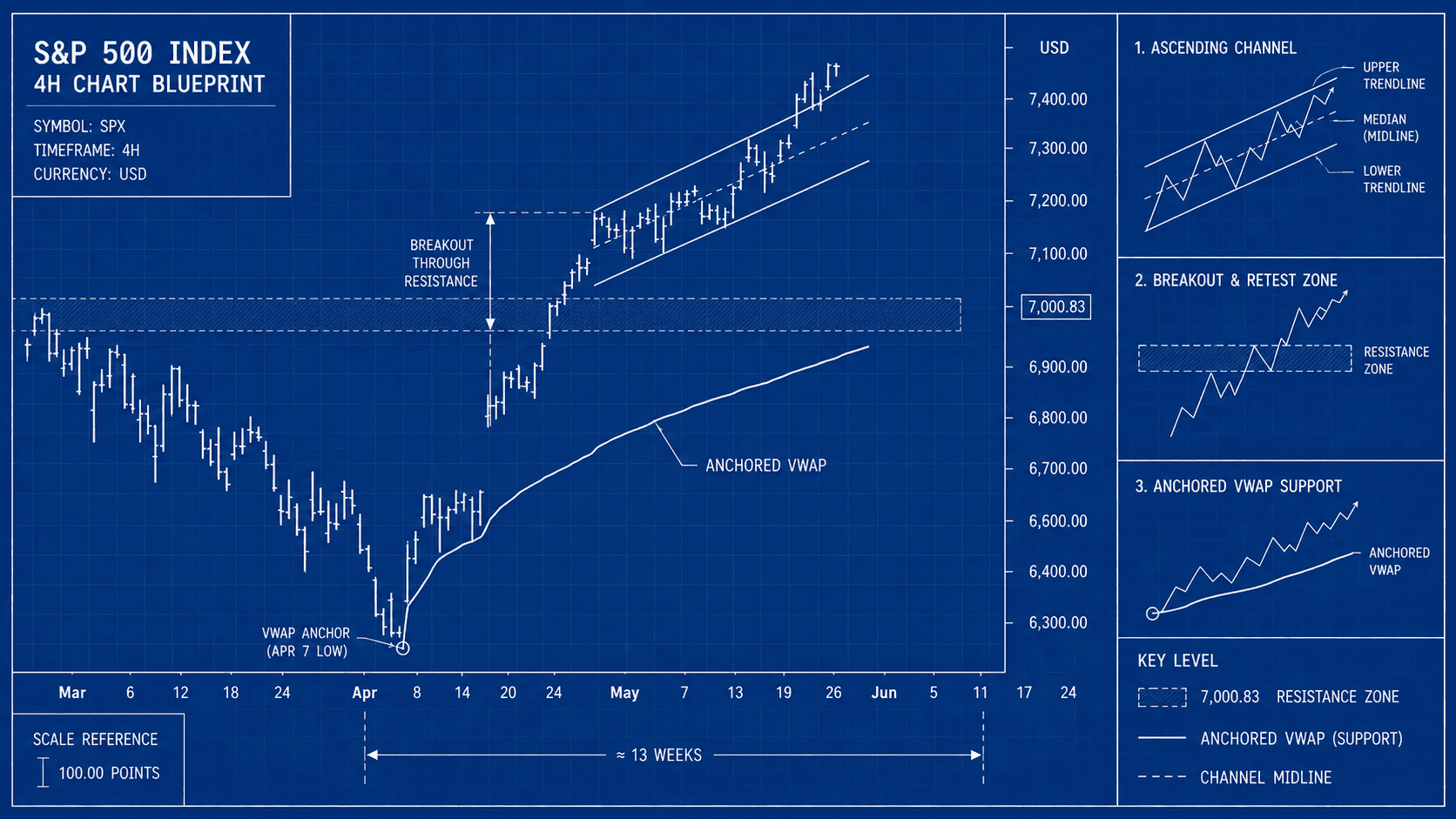

SPX Technical Outlook

The SPX continues trading inside a strong ascending channel structure on the 4-hour timeframe, with momentum remaining firmly bullish despite increasingly overbought conditions.

The index has now broken significantly above prior resistance and continues respecting higher lows while riding above anchored VWAP support.

RSI remains elevated near overbought territory, reflecting strong momentum but also increasing sensitivity to any macro disappointment.

Bullish SPX Scenario: Rally Extension Continues

The bullish case remains structurally intact as long as:

- inflation does not materially broaden

- labour market deterioration remains gradual

- and yields stabilise rather than break aggressively higher

Under this scenario, markets may conclude:

- the oil spike is temporary

- central banks remain cautious but not aggressively hawkish

- and eventual rate cuts later this year remain possible

Technically, the chart structure still favours continuation higher.

The ascending channel remains intact, and buyers continue stepping in at shallow pullbacks.

If momentum persists:

- SPX could continue grinding higher within the current channel

- leadership may remain concentrated in growth and technology

- and liquidity conditions could continue supporting risk assets into summer

A softer inflation interpretation this week could act as another catalyst for upside continuation.

Bearish SPX Scenario: What Could Trigger a Correction

The bearish risk emerges if markets begin believing this oil shock is evolving into a broader inflation regime shift.

That would likely require:

- sustained energy strength

- rising inflation expectations

- stronger-than-expected CPI

- or a reacceleration in wage pressures

Under that scenario:

- yields would likely move sharply higher

- rate cuts would be repriced even further out

- financial conditions would tighten again

- and equity valuations would face pressure

Technically, the market is already extended.

RSI is elevated, positioning is increasingly crowded, and price is trading near the upper boundary of the channel.

If a correction develops, the first major downside area becomes:

7000 Horizontal Support

This zone aligns closely with:

- prior breakout structure

- the anchored VWAP

- and broader dynamic trend support

The anchored VWAP currently acts as a critical institutional support area.

A clean hold there would likely preserve the broader bullish trend structure.

However, if price loses both:

- horizontal support

- and anchored VWAP support

then a deeper corrective phase could begin as momentum positioning unwinds.

Final Thoughts

Markets are entering a critical macro phase where the debate is no longer simply about inflation.

The real debate is whether:

- higher oil prices create another lasting inflation cycle

or - whether slowing growth ultimately forces central banks back toward easing later this year.

That distinction will drive:

- yields

- equities

- risk appetite

- and central bank expectations throughout the summer.

For now, SPX remains technically bullish — but increasingly sensitive to macro data surprises and inflation expectations.

This week’s inflation data and central bank communication may determine whether the rally extends further or finally enters a corrective phase.