Written by:

- Opening Bell

- June 22, 2026

- 7 min read

Can Wall Street Outrun a Stronger Dollar This Week?

Three forces are shaping this week’s narrative:

- Iran says the Strait of Hormuz remains closed, but negotiations with the United States are still progressing towards a wider agreement.

- The dollar has strengthened towards 101, while short-term Treasury yields are rising as markets price a greater chance of another Federal Reserve rate increase.

- US equities remain within four-hour uptrends, with Micron and other semiconductor shares climbing ahead of this week’s earnings.

Oil has fallen as traders price a lower probability of prolonged supply disruption, although the situation on the ground remains far from settled. Meanwhile, investors are returning to the dollar. DXY has pushed into and briefly above a major resistance zone, while USD/JPY is approaching 162.

Yet US equities have not broken down. At least not yet.

The S&P 500 and Nasdaq remain within four-hour uptrends, while Micron and other semiconductor shares are climbing ahead of this week’s earnings. Perhaps the market can remain resilient despite the stronger dollar and higher yields.

The New York market open will provide the first meaningful test.

Is the Strait of Hormuz Open or Closed?

This is where much of the current confusion begins.

Early headlines focused heavily on Iranian negotiators walking out of the meeting, creating the impression that talks had broken down completely. However, the walkout was a temporary protest rather than Iran’s definitive withdrawal from the negotiations.

Discussions continued through Qatari and Pakistani mediators, and Iranian officials remained involved in technical talks. Foreign Minister Abbas Araghchi said the first round had made major progress, while Qatar and Pakistan announced a roadmap aimed at reaching a final agreement within 60 days.

The Strait of Hormuz is also not completely sealed. Iran has declared it closed and commercial traffic has fallen sharply, but selected vessels have continued to pass. It is therefore more accurate to describe the strait as politically closed and heavily restricted, rather than physically closed to every ship.

The negotiations suffered a serious interruption, but did not collapse. Markets are responding to the possibility of a wider agreement and reduced disruption, although both the talks and shipping situation remain fragile.

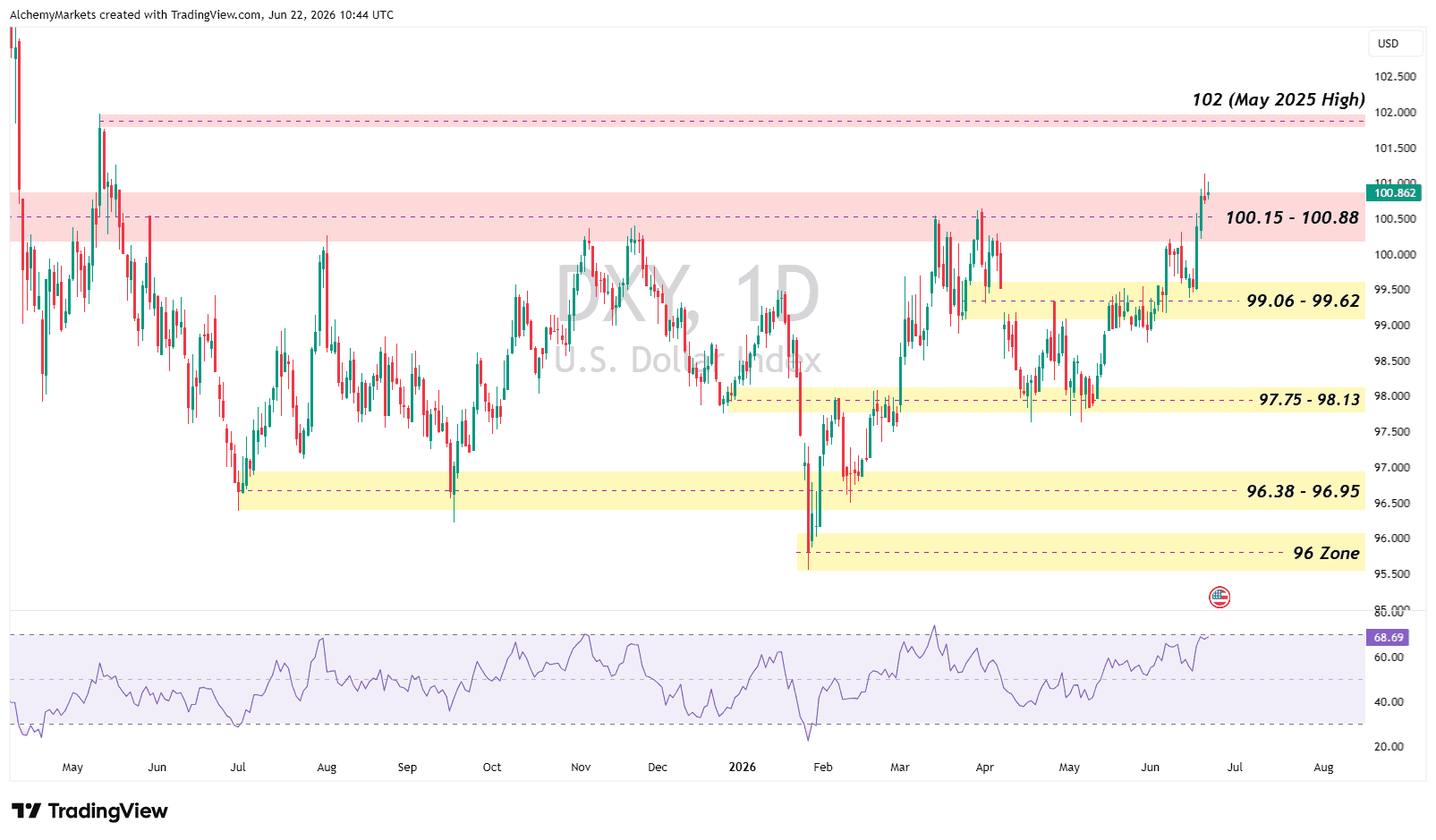

Dollar Strength Reaches a Decision Point

DXY has pushed into and briefly above the 100.15 to 100.88 resistance zone, supported by higher US yields, resilient economic activity and a more hawkish Federal Reserve.

The immediate question is whether DXY can confirm the breakout with a daily close above 100.88.

A confirmed close above that level would strengthen the bullish structure and bring the May 2025 high near 102 back into focus.

However, the dollar is no longer moving through open space.

DXY is testing established resistance while its daily Relative Strength Index approaches 70. That shows strong momentum, but it also means the move is becoming increasingly stretched.

This is central to the equity outlook.

A rising dollar can:

- Tighten global financial conditions

- Increase the cost of dollar-denominated debt

- Place pressure on emerging markets

- Reduce the reported value of overseas earnings for US companies

- Make US assets more expensive for international investors

But Wall Street may not need the dollar to reverse sharply.

It may only need DXY to stop accelerating.

If the index falls back below 100.88 or begins consolidating around the resistance zone, the additional pressure on equities may remain manageable.

A clean breakout towards 102 would create a more difficult backdrop, particularly if Treasury yields continue rising alongside it.

USD/JPY provides further confirmation of broad dollar demand. The pair is approaching the 161.96 to 162.00 area, with the yen already trading near its weakest level against the dollar in almost four decades.

A sustained break above 162 would place the yen at a fresh multi-decade low and further increase the possibility of Japanese intervention.

Why Higher Yields May Not Stop Stocks Rising

Higher yields can pressure equities, especially technology stocks, but the relationship is not automatic.

Stocks can still rise when yields increase because the economy remains resilient, earnings are growing and recession risk is falling. In that environment, higher yields partly reflect stronger growth rather than an inflation shock.

The two-year Treasury yield is near 4.23%, while the ten-year remains around 4.50%. Markets appear willing to tolerate those levels for now. The risk is that yields rise because inflation is accelerating and investors begin pricing several Fed increases.

Thursday’s PCE report will help show whether the move reflects healthy growth or renewed inflation pressure.

US Indices Remain in Four-Hour Uptrends

The latest price action remains technically constructive, although the US open will show whether the recovery has enough demand behind it to continue.

Both the S&P 500 and Nasdaq declined during Friday’s shortened futures trading before recovering through the Asian session and extending higher during London trading.

S&P 500

The S&P 500 remains in a four-hour uptrend after rebounding from its 4H-200 exponential moving average last Wednesday.

Key levels include:

- Immediate resistance: 7,520 to 7,540

- Next upside area: 7,582 to 7,604

- Initial support: 7,460 to 7,486

- Broader four-hour support: Approximately 7,340 to 7,425 around the 200 EMA

A clean breakout above 7,540 would strengthen the case for another test of the highs.

A rejection would not immediately break the uptrend, provided the index continues holding above its immediate support region.

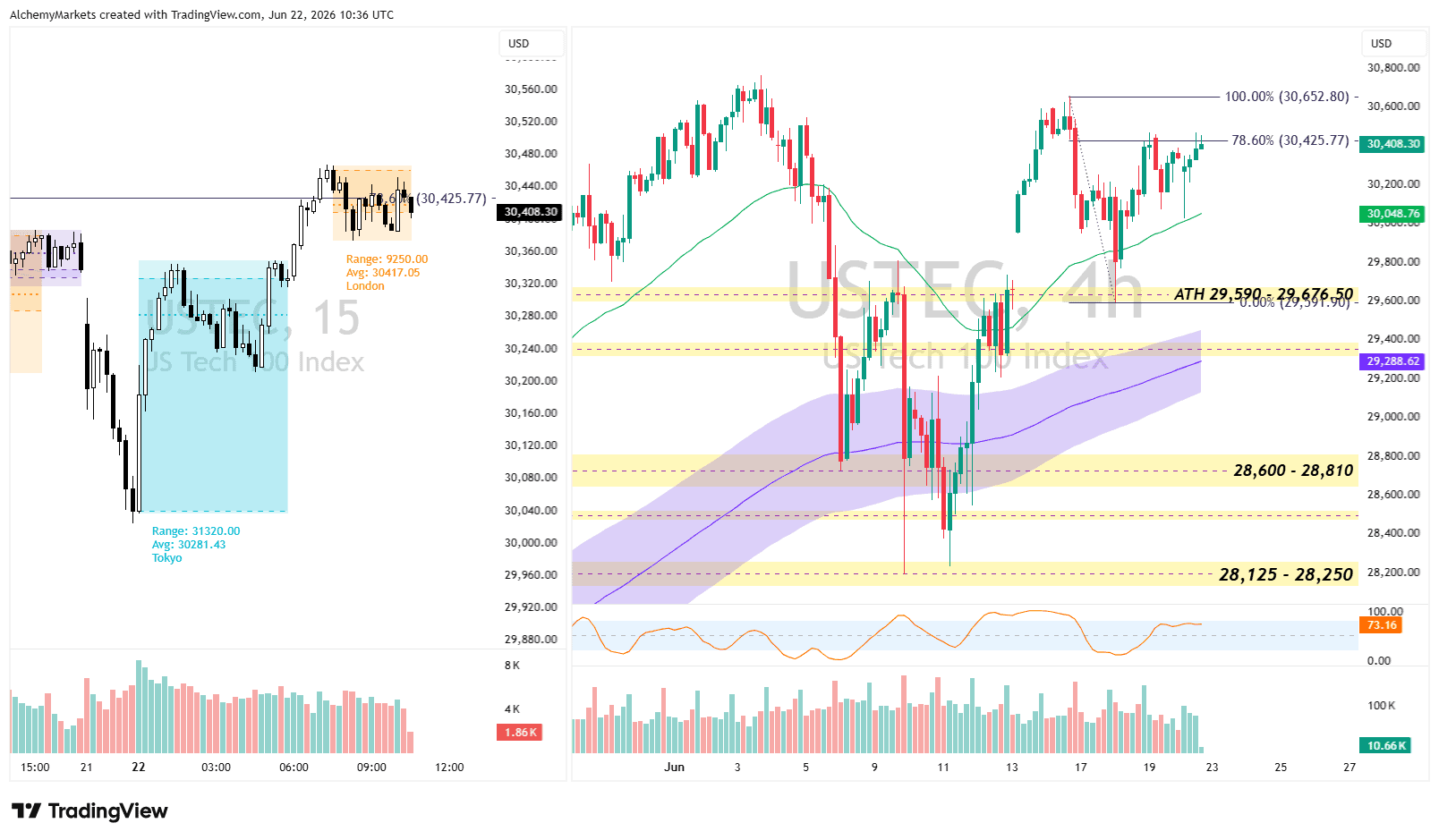

Nasdaq

The Nasdaq remains technically stronger. It rebounded from its 4H-50 EMA, and previous all time highs at 29,590, rather than requiring another test of the 200 EMA. Price has since recovered towards the 78.6% Fibonacci retracement near 30,426.

The main levels are:

- Immediate resistance: 30,426

- Previous high: Approximately 30,653

- Four-hour 50 EMA support: Approximately 30,049

A break above 30,426 could reopen the previous high.

A rejection would not immediately invalidate the uptrend while price remains above the four-hour 50 EMA.

Both US indices are therefore entering the session from constructive trends, but directly beneath resistance.

Earnings Become the Next Market Test

This week’s earnings will test whether the rally is still supported by strong demand and corporate growth.

- FedEx, Tuesday: Delivery volumes, business demand and margins will provide an early signal on the health of the US economy and global trade.

- Trip.com, Wednesday: Results will offer a read on Asian travel demand, international bookings and whether the weak yen is still supporting tourism into Japan.

- Micron, Wednesday: The main event for markets this week.

Micron matters because semiconductor and memory stocks have been carrying a large part of the rally. Its shares have climbed almost 300% this year, leaving very little room for disappointment.

Investors will focus on:

- High-bandwidth memory demand

- DRAM and NAND pricing

- Data-centre revenue

- Gross-margin guidance

- Capital spending and future supply

Strong results and guidance would support the AI and semiconductor rally. A disappointment could pressure Micron and spill into the wider Nasdaq, particularly with valuations already stretched.

Bottom Line

Wall Street is entering the week with a stronger dollar, higher Treasury yields and unresolved geopolitical risk. However, CFD markets are holding up well for now, with the S&P 500 and Nasdaq still trading within four-hour uptrends.

The main question is whether DXY stalls near resistance or continues towards 102. Equities may remain resilient if the dollar and yields stop accelerating, but a stronger breakout would place more pressure on technology shares and wider risk appetite.

This Week’s Timeline

- Monday: The US open tests whether the current CFD recovery can hold beneath resistance.

- Tuesday: FedEx earnings provide an early read on business activity, consumer demand and global trade.

- Wednesday: Micron becomes the main earnings test for the AI and semiconductor rally. Trip.com also reports.

- Thursday: PCE inflation tests whether rising yields reflect resilient growth or renewed inflation pressure.

- Throughout the week: Iran negotiations and Strait of Hormuz headlines remain the main geopolitical risk.

For now, the trend remains constructive. Micron and PCE will determine whether that resilience develops into another breakout or begins to crack under a stronger dollar and increasingly demanding expectations.