Written by:

- Weekly Outlook

- April 17, 2026

- 5 min read

Rising Inflation to Drive FX: Policy Divergence Points to a Softer Dollar

With inflation expected to rise more sharply over the next three to six months, global currency markets are entering a more policy-driven phase. The key differentiator will be which central banks are willing to keep real interest rates—that is, rates adjusted for inflation—firmly in restrictive territory.

In this environment, currencies linked to more hawkish central banks are likely to find support. We are already seeing early signs of this shift. The European Central Bank is now expected to deliver another rate hike as soon as June, while further policy tightening remains on the table in Australia and Norway. These central banks appear increasingly focused on preventing a renewed inflation cycle, even at the cost of slower growth.

By contrast, the Federal Reserve looks less likely to re-engage in an aggressive tightening cycle. While inflation risks remain elevated in the US, the balance between growth and price pressures appears more delicate. As a result, the Fed is expected to remain cautious rather than overtly hawkish.

This divergence in policy outlooks is critical. If other central banks continue tightening while the Fed holds back, interest rate differentials will begin to move against the US dollar. Over time, this should lead to a softer dollar, particularly against currencies where real yields are being actively supported.

In short, the next phase for FX markets will be less about absolute inflation levels and more about policy response credibility—specifically, which central banks are willing to act decisively to contain inflation, and which are not.

United States

It’s a quieter week for economic data, so markets will mainly focus on talks between the US and Iran. If the two sides reach a deal and tensions ease—especially around the important oil route called the Strait of Hormuz—it would likely calm markets.

But if talks fail, things could go the other way. Investors may get nervous, stock markets could fall, and the US dollar might rise. That’s because oil prices could stay high, pushing up inflation and making it harder for the Federal Reserve to cut interest rates anytime soon.

The Federal Reserve is in its “quiet period” before its next meeting on April 29, meaning officials won’t be speaking publicly. However, there’s still attention on Kevin Warsh, who is being considered as the next Fed Chair. His confirmation hearing is on April 21.

Warsh used to be seen as someone who prefers higher interest rates, but since he’s been nominated by Donald Trump—who wants lower rates—people will be watching closely to see what he says. He’s likely to suggest that lower rates could make sense eventually, but only if the economy supports it.

He also believes that technology and AI investment could help the US economy grow faster without causing inflation, which is a view some Fed members agree with.

However, his approval may not be straightforward. There are political disagreements that could delay the process.

As for economic data, the key report this week is March retail sales (how much consumers are spending). Sales may look stronger partly because of higher petrol prices and better car sales.

But the more important figure strips out things like cars and fuel. This “core” measure is expected to show only a small increase. If that happens, it would suggest that consumer spending is still weak, especially as people feel financially squeezed and less confident.

United Kingdom

This week, the focus is on jobs, wages, and inflation.

- Jobs and wages (Tuesday):Wage growth in the private sector is expected to slow down. This is because the job market is weakening slightly, which reduces pressure on employers to raise pay.This supports the argument that the Bank of England doesn’t need to raise interest rates further.

- Inflation (Wednesday):Inflation is expected to rise slightly, mainly due to higher petrol and heating oil prices linked to tensions involving Iran.The overall inflation rate could reach around 3.3%.

However, the full impact on household energy bills won’t be seen until July, when price caps are updated.

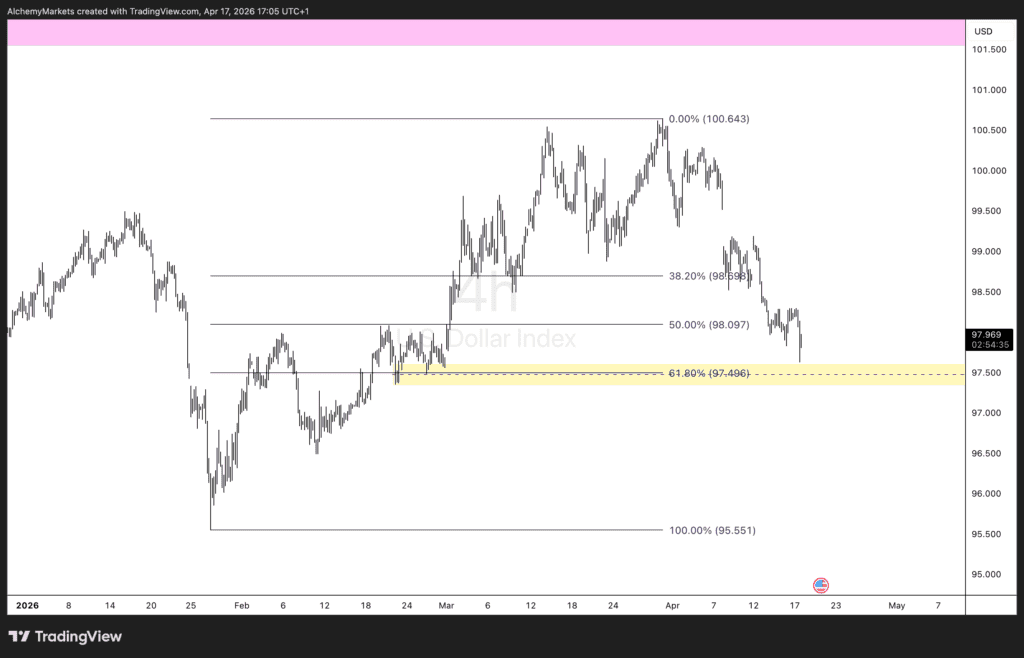

Technical Analysis – DXY (US Dollar Index)

From a technical perspective, the DXY is currently trading around the 61.8% Fibonacci retracement level, a zone widely viewed as a key inflection point in trending markets. This level, often referred to as the “golden ratio,” tends to act as strong support during corrective phases.

The recent price action suggests that the dollar has been moving within a broader bearish impulse structure, with lower highs and a gradual loss of upside momentum following its peak near the 100.60 area. The pullback into the 61.8% retracement—around the 97.50 region—places the index at a technically significant support zone.

Holding this level could trigger a short-term corrective bounce, effectively unwinding part of the bearish move. In this scenario, a move back toward the 50% retracement or even the 38.2% level would not be surprising, particularly if macro catalysts (such as rate expectations or geopolitical developments) provide support.

However, the broader structure still leans bearish. A decisive break below the 61.8% level would likely confirm continuation of the downside impulse, opening the door toward the 100% retracement area near 95.50.

In summary, the DXY is at a critical juncture:

- Support holding → corrective rebound within a bearish trend

- Support breaking → continuation of downside momentum

This aligns closely with the macro view of a potentially softer dollar, but near-term price action may first see a technical correction before any sustained decline resumes.

Bottom Line

- Global tensions (especially US–Iran) are the biggest market driver this week.

- US consumers still look financially stretched despite higher spending figures.

- In the UK, wage growth is cooling and inflation is ticking up slightly.