Written by:

- Opening Bell

- June 24, 2026

- 5 min read

Can Micron Stop the AI Selloff After Korea’s Leverage Flush?

Tuesday’s technology selloff looked dramatic, but the first trigger was not a collapse in AI demand. It was a leverage shock in South Korea. Samsung Electronics and SK Hynix fell more than 12%, pulling the KOSPI down 9.99% and forcing a market-wide trading halt.

The decline then spread into US memory stocks, with Micron and SanDisk losing more than 13%. Today’s question is whether that was a violent reset in crowded positioning or the opening stage of a deeper Nasdaq correction. Micron’s earnings after the US close may provide the answer.

| The selloff began as a leverage flush. Micron now has to prove that the fundamentals still support the price. |

Why Korea’s leverage flush matters

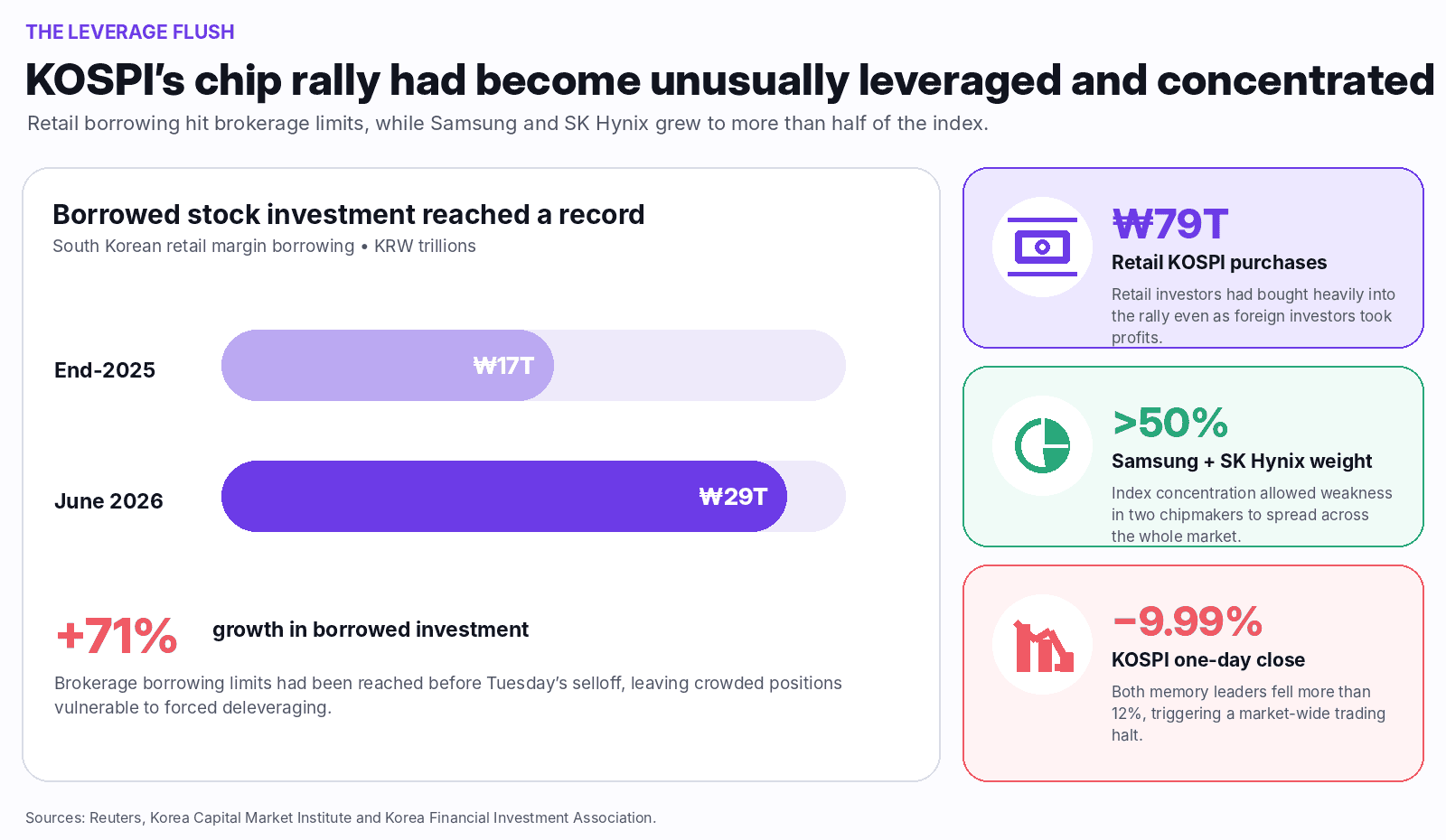

The KOSPI had already become unusually stretched. Retail investors bought ₩79 trillion of KOSPI shares this year, while borrowed stock investment reached a record ₩29 trillion, up 71% from the end of 2025. Local brokerages had reached their lending limits before Tuesday’s fall.

At the same time, Samsung and SK Hynix had grown to more than half of the index’s market value. When regulators warned that leveraged single-stock ETFs were adding fuel to the rally, foreign selling in those two names quickly became a market-wide shock.

That supports the leverage-flush argument. It does not mean the decline was harmless. Korea supplied the trigger, but the semiconductor trade was already crowded, US yields were rising and the Federal Reserve had become more hawkish. The market had very little room for disappointment.

Are markets bearish now?

Not yet. The warning signs have increased, but the larger bullish structures have not fully broken.

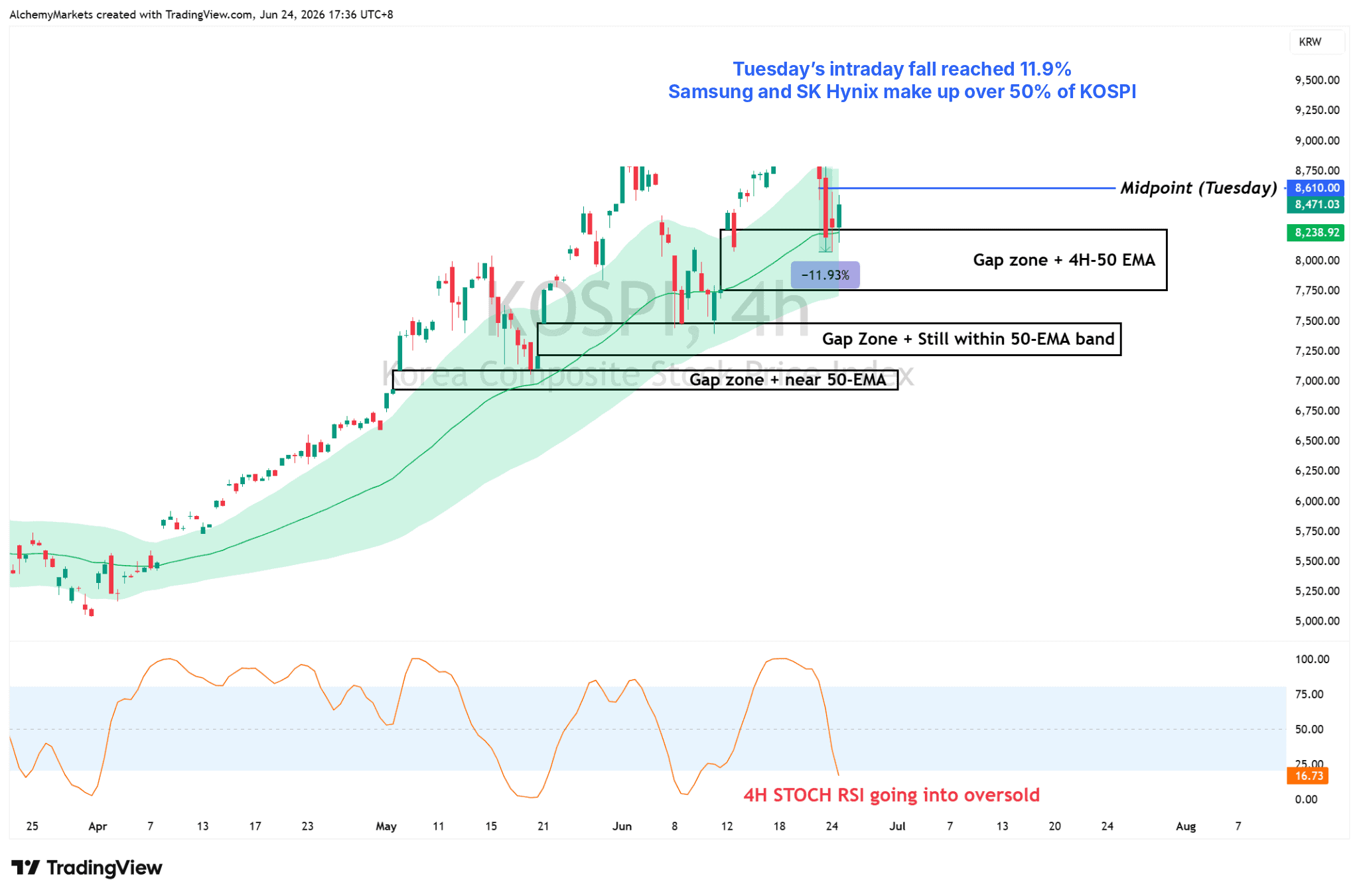

KOSPI is trading from a familiar support area, while its four-hour Stoch RSI has moved into oversold territory. A recovery above Tuesday’s 8,610 midpoint would improve the stabilisation case.

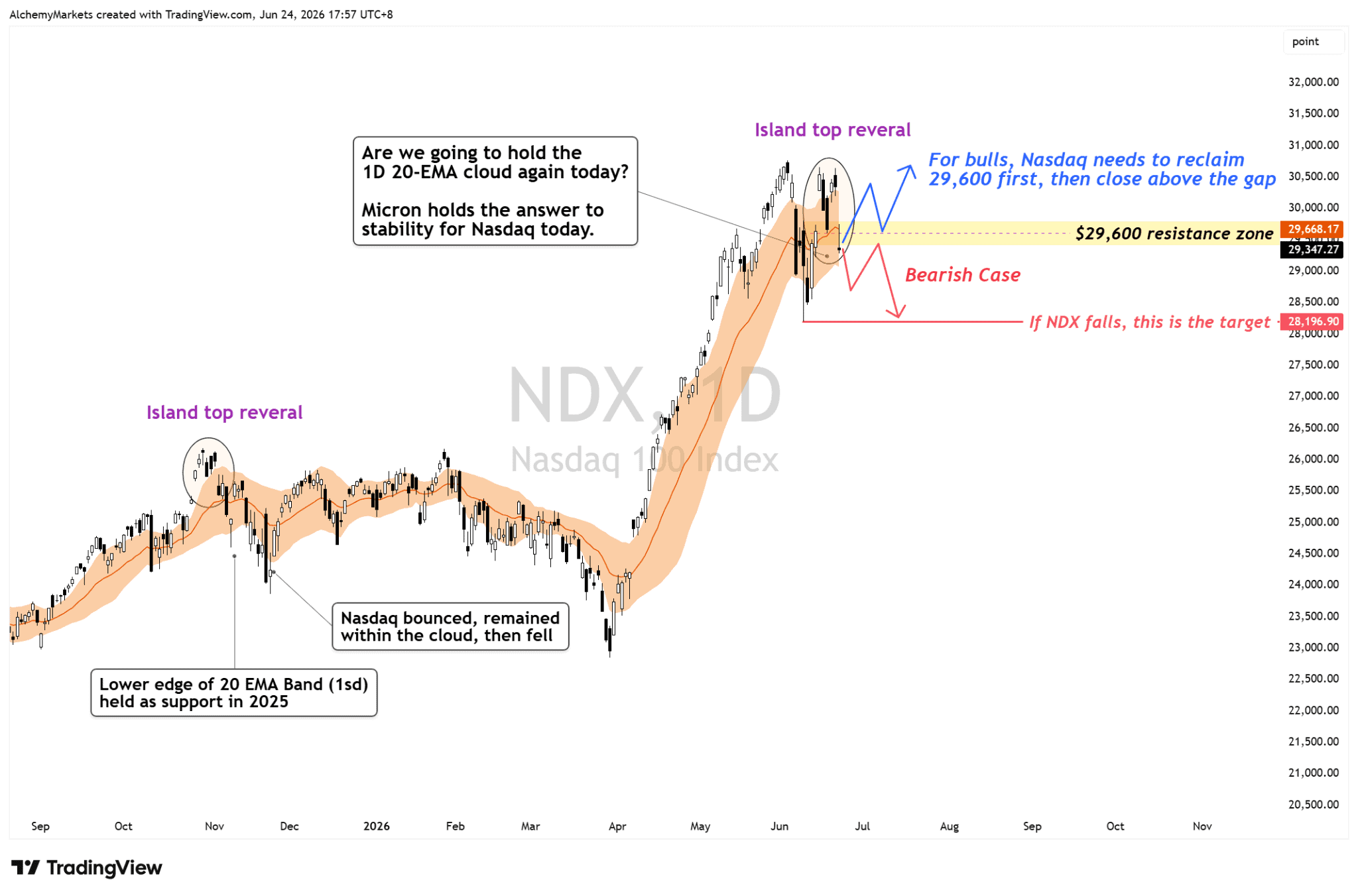

Nasdaq is more delicate. The index has formed a potential island-top reversal near record highs, but the pattern still needs confirmation. Bulls need to reclaim 29,600 and close the overhead gap. A decisive close below the daily 20-EMA cloud would expose the next marked support near 28,196.

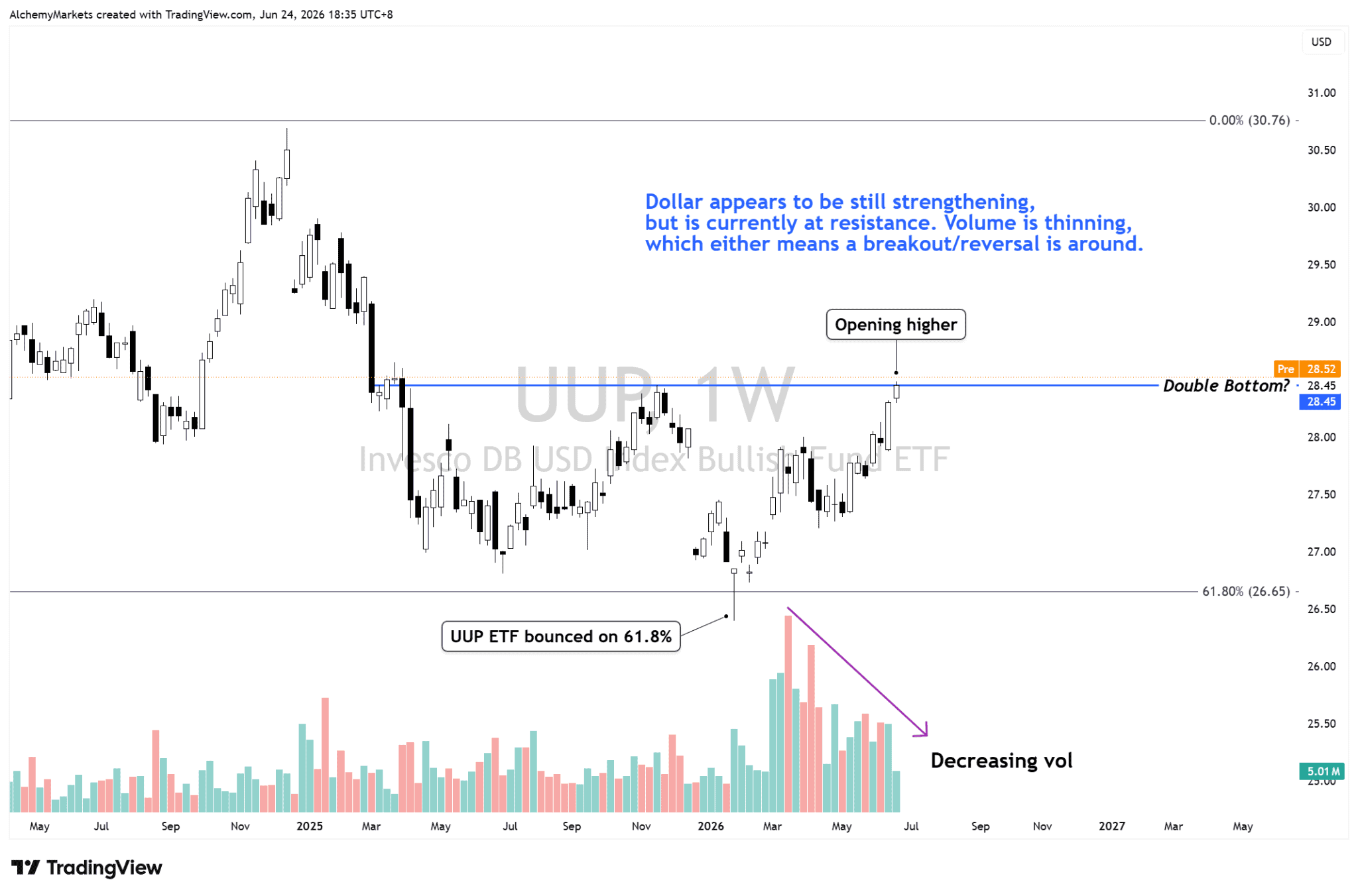

Dollar remains the macro confirmation

The dollar remains another pressure point for technology shares. DXY does not provide a clean centralised volume series, so UUP, a bullish dollar ETF is useful as a tradable proxy for participation in the dollar move. It is not an exact copy of DXY, but its exchange-traded volume helps show whether fresh demand is entering.

UUP has rebounded from the 61.8% retracement near $26.65 and is testing the $28.45 neckline of a possible weekly double bottom. Price is firm, but volume has thinned into resistance. A weekly breakout with expanding volume would strengthen the dollar case and increase pressure on rate-sensitive growth shares. A rejection would remove one of Nasdaq’s immediate headwinds.

Micron has two jobs tonight

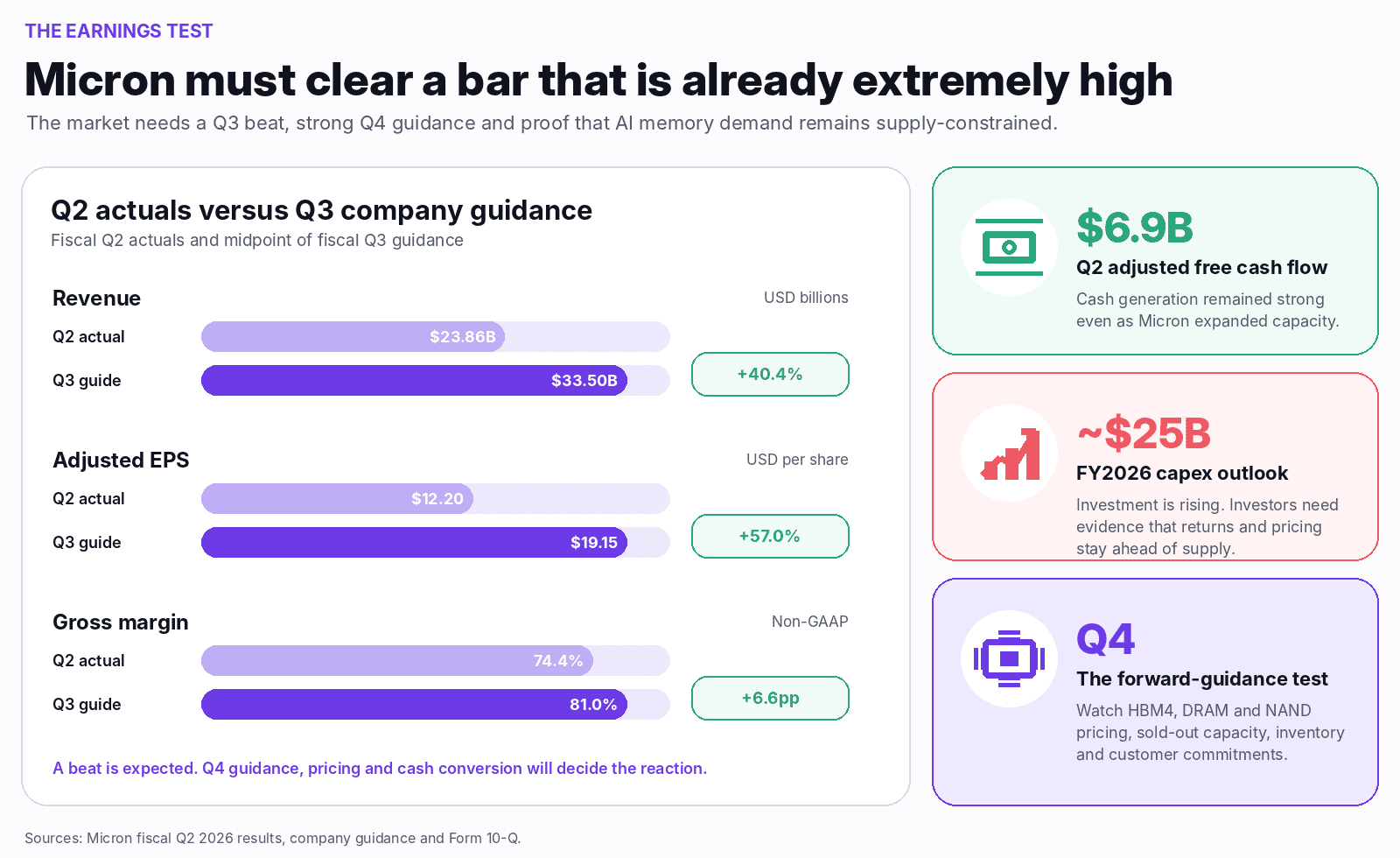

First, Micron must clear a financial bar that is already extremely high. Fiscal Q2 revenue reached $23.86 billion, adjusted EPS was $12.20 and non-GAAP gross margin reached 74.4%. For fiscal Q3, management guided to $33.5 billion of revenue, $19.15 of adjusted EPS and an 81% gross margin at the midpoint.

Second, management must show that the next quarter can remain strong. A headline beat is expected. The larger market reaction will depend on Q4 guidance, HBM4 and data-centre demand, DRAM and NAND pricing, sold-out capacity, inventory and customer commitments.

The cash-flow test beneath the headline numbers

Micron’s previous quarter showed why the quality of the beat matters. Revenue reached $23.86 billion, operating cash flow climbed to $11.9 billion, capital expenditure was $5.0 billion and adjusted free cash flow reached $6.9 billion. Inventory remained broadly stable at $8.27 billion, even as revenue accelerated sharply.

Investors therefore need the new report to show that cash generation is keeping pace with investment. Rising capital expenditure is not automatically bearish when demand is constrained, but a large inventory build, weaker free cash flow or commentary pointing to future oversupply would challenge the idea that this cycle is structurally different.

Micron’s chart still favours the bulls, but damage is visible

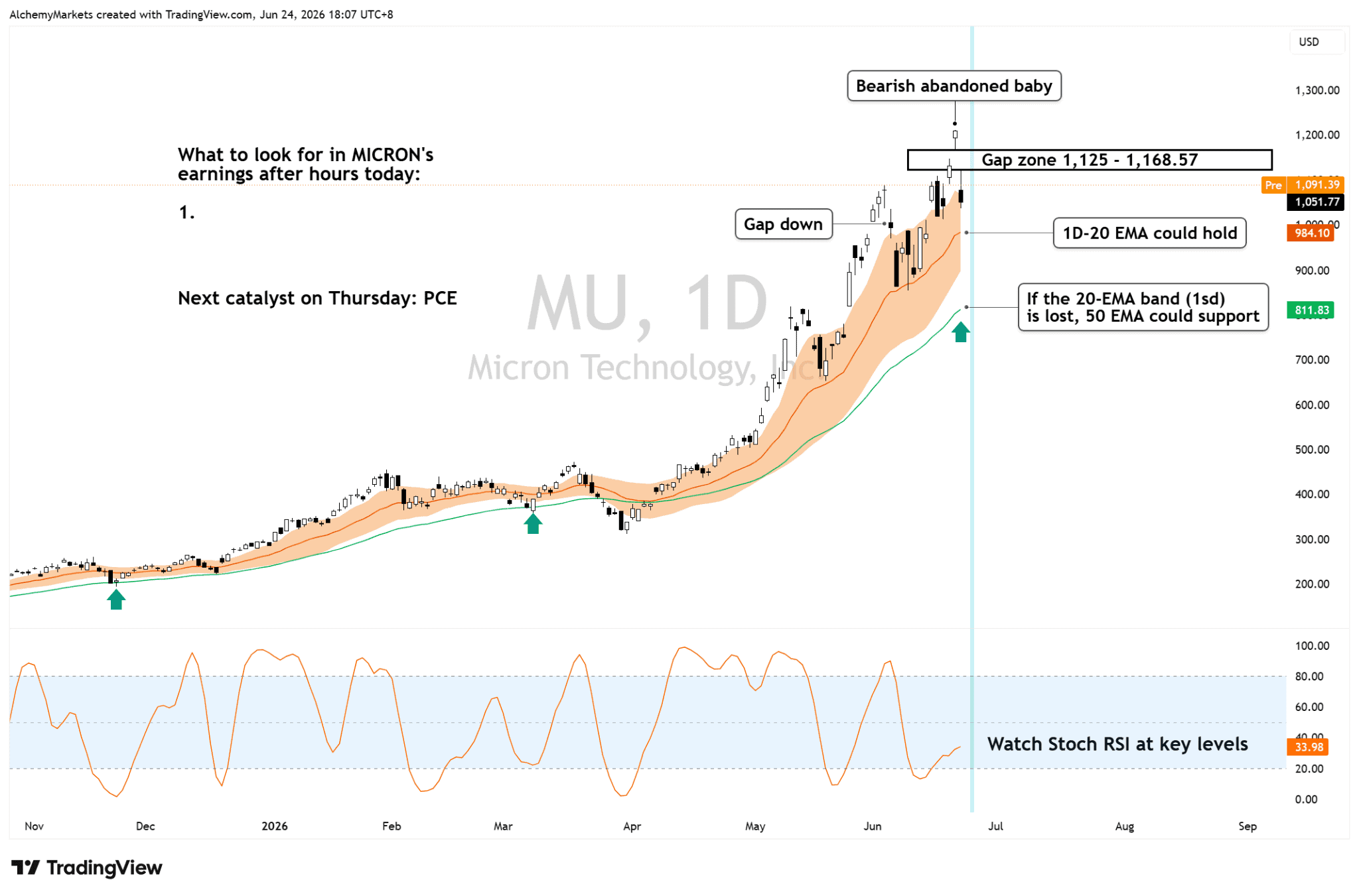

Micron still holds a broader sequence of higher highs and higher lows. The larger uptrend has therefore not reversed. However, the short-term structure has weakened after a bearish abandoned-baby-style formation and a large gap down from the record high.

The daily 20-EMA cloud near $984 is the first important support. If earnings produce a constructive reaction, bulls then need to attack the $1,125 to $1,168.57 gap zone. Stoch RSI is recovering from oversold conditions, but it has not yet confirmed a bullish momentum reversal.

If the 20-EMA band fails, the rising 50-EMA near $812 becomes the next major trend support. That would be a much deeper correction, but it would not automatically end the longer-term uptrend.

PCE can still complicate the relief trade

Micron can repair the AI earnings narrative, but it cannot remove the macro risk. The Federal Reserve’s preferred PCE inflation measure arrives on Thursday. A stronger reading could lift yields and reinforce expectations for tighter policy, placing renewed pressure on long-duration technology shares.

The strongest bullish combination would be a Micron beat and raise, followed by softer inflation and lower yields. The most dangerous combination would be cautious Micron guidance followed by hotter PCE. In that scenario, a fundamental disappointment could restart the leverage unwind across semiconductors.

Bottom line

Markets are not confirmed bearish yet. Tuesday’s move looked more like panic selling and forced deleveraging than proof that AI demand has collapsed. However, the burden of proof has shifted back to buyers.

Micron must now confirm both sides of the story. The numbers need to show that the memory cycle remains strong, while the price reaction needs to help Nasdaq reclaim trend support. A beat and raise would support the leverage-flush explanation. Cautious guidance or another sell-the-news reaction would suggest that crowded positioning has become the larger problem.