Written by:

- Opening Bell

- March 19, 2026

- 5 min read

Post-FOMC Recap: Oil and Rate Uncertainties Rock the Markets

The March FOMC just concluded, with the Federal Reserve maintaining a cautious tone. While policy was left unchanged, the messaging did little to support expectations of near-term easing.

Instead, the focus returned to inflation risks, particularly those linked to energy, pushing expectations for rate cuts further out.

This reflects a shift from earlier expectations of steady disinflation, as renewed US–Iran tensions and higher oil prices reintroduce upside risks.

Key Focus Points

- Fed holds rates in March, as expected

- Inflation risks remain to the upside

- Oil flagged as a key inflation uncertainty

- Rate cut expectations pushed further out

- Small probability of hikes reappears

- Yields rebound after initial dip

- Equities and gold under pressure

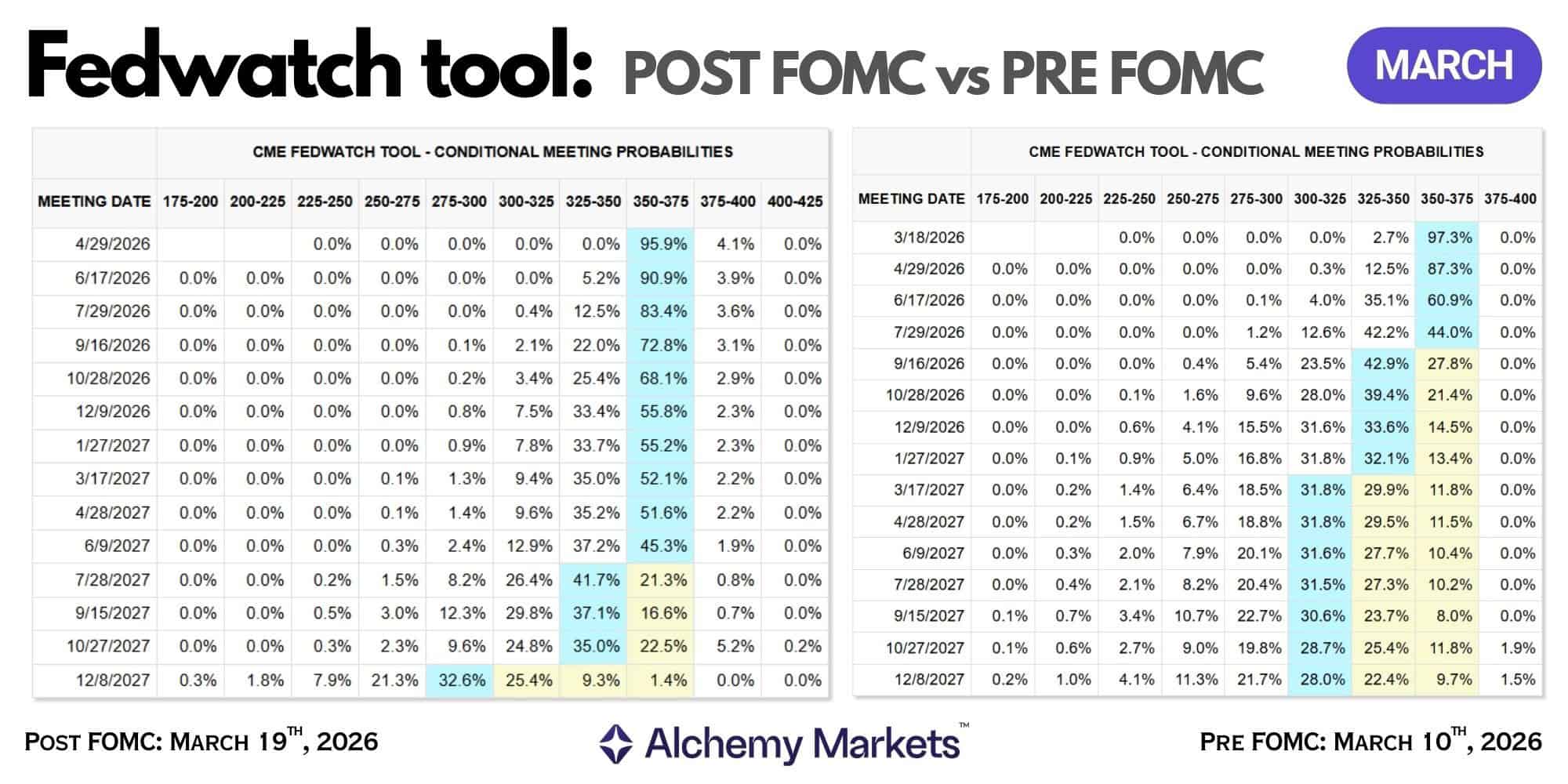

Rate Expectations Repriced: Post FOMC vs Pre FOMC

Expectations for rate cuts have been pushed further out following the March FOMC, marking a clear shift from earlier projections of easing as soon as June. Markets are now pricing a slower path, with cuts delayed toward September at the earliest, and increasing likelihood of just one cut, or potentially no cuts, by year-end.

Observe how expectations have shifted from pre-FOMC to post-FOMC pricing:

- Rate cuts expected to hold for longer, and rate hikes expectations are being introduced to the mix

Other economic metrics also support this tonal shift on rate cuts. Officials now see total PCE inflation at 2.7% this year and 2.2% next year, while the implied policy path points to rates easing only toward 3.4% by year-end and 3.1% the following year.

This reflects a higher-for-longer stance, where policy remains restrictive unless inflation shows sustained improvement. Compared to the previous week, markets have reduced the probability of multiple cuts and are even assigning a small chance of further tightening.

Powell Confirms a Data-Dependent, Higher-for-Longer Bias

Powell’s remarks during the conference help explain the shift in rate expectations, with repeated emphasis on uncertainty and upside inflation risks, particularly linked to energy markets.

Powell said — “The implications of developments in the Middle East for the U.S. economy are uncertain.”

He also acknowledged the near-term impact of higher energy prices:

“Higher energy prices will push overall inflation… it is too soon to know the scope and duration.”

When asked about the broader economic effects, the response remained non-committal:

“We don’t know… the effects could be smaller or much bigger.”

At the same time, inflation risks were not dismissed:

“Risks to inflation are to the upside.”

And importantly, there was no signal of urgency to ease: “We will wait and see.”

Taken together, these remarks reinforce a Fed that is no longer confident in a smooth disinflation path, but are forced to stay in ‘Wait-and-see’ mode.

Policy remains reactive, with any move toward easing dependent on incoming inflation data rather than a defined timeline. Bottom line, there is no near-term policy support for risk assets unless inflation shows clear and sustained improvement.

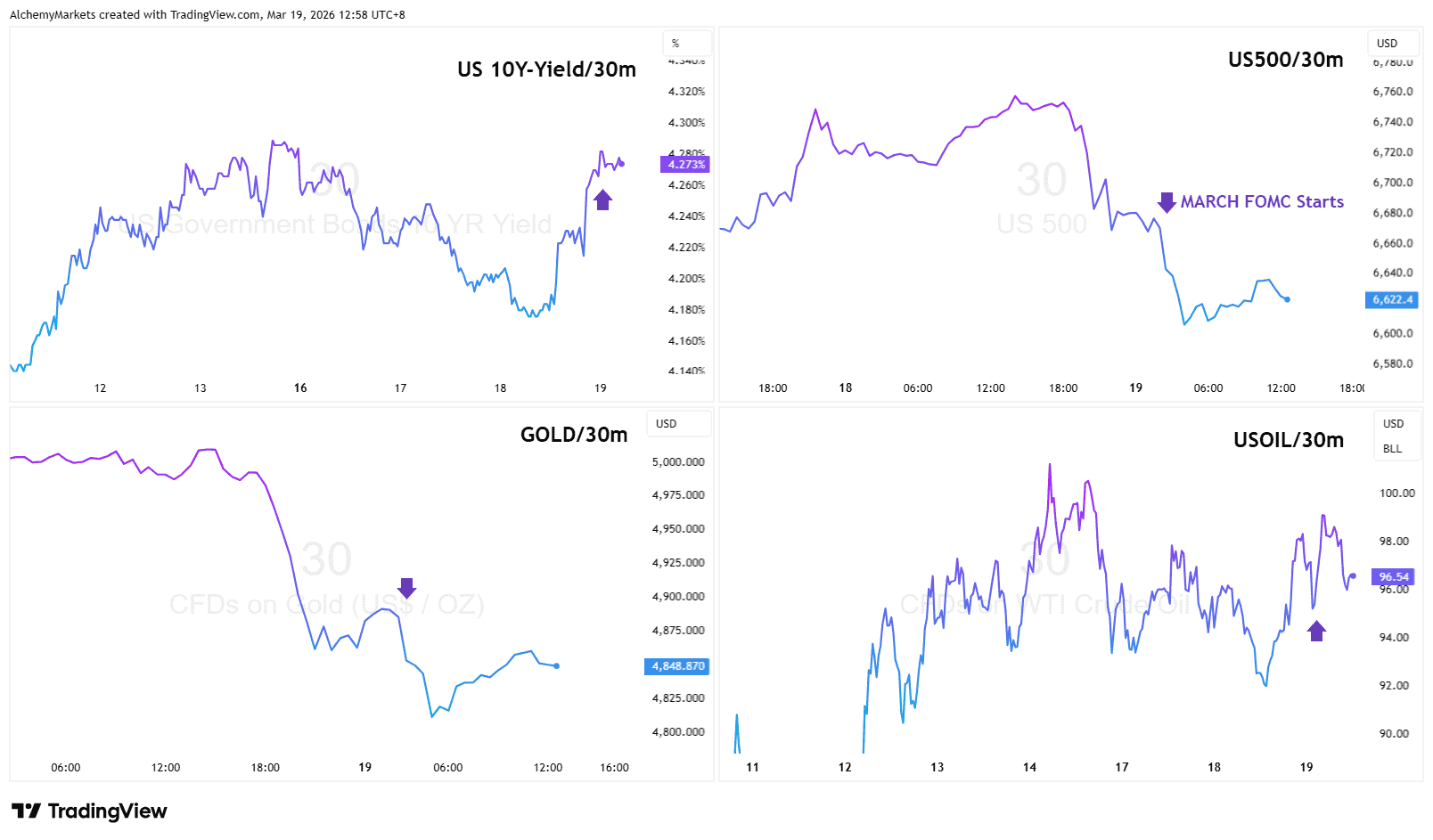

How Markets Have Reacted: Yields Rise, Equities and Gold Weaken

The immediate reaction following the FOMC has been a move higher in Treasury yields, with direct spillover effects across asset classes.

The US 10-year yield initially dipped before finding support and moving higher

This indicates a repricing of the expected rate path rather than a one-off reaction. Markets are adjusting to the likelihood that policy remains restrictive for longer.

Equities have weakened as higher yields tighten financial conditions.

The move lower in the US500 reflects repricing pressure rather than forced liquidation.

Gold has also declined, failing to benefit from uncertainty.

This reflects the dominance of rising real yields over safe-haven demand in the current environment.

Oil remains elevated, sustaining pressure on the inflation outlook and reinforcing the Fed’s cautious stance.

Taken together, this is a cross-asset adjustment to a more restrictive and uncertain policy outlook, not a broad risk-off event. At this stage, markets are adjusting to a shift in policy expectations rather than trending in a single direction.

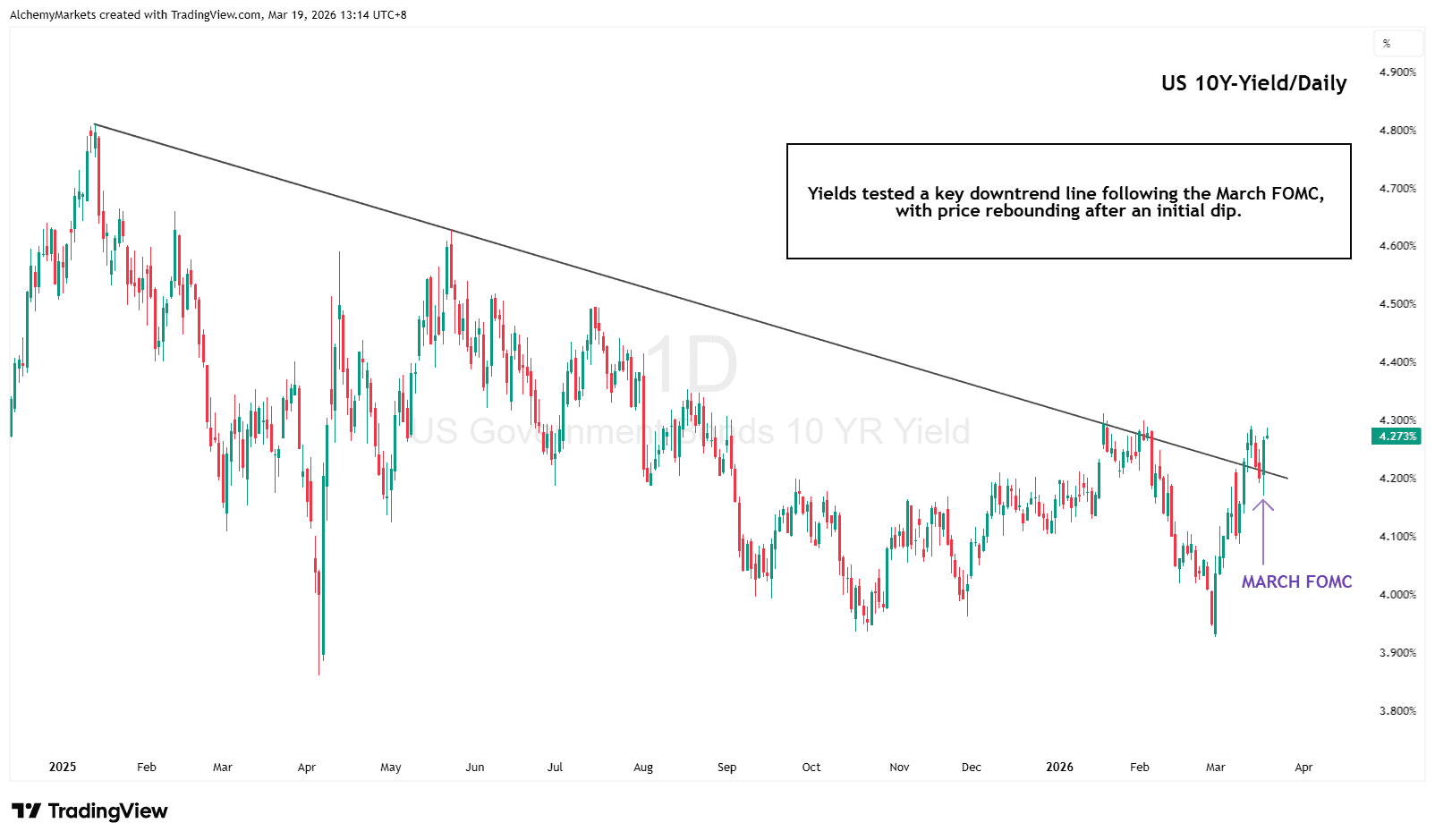

Yields Are the Transmission Mechanism

The US 10-year yield remains the key transmission channel for policy expectations.

Following the FOMC, yields briefly declined before finding support along the broader trendline structure and reversing higher. This behaviour reflects a reassessment of inflation persistence.

Oil acts as the source of inflation pressure, while yields transmit that pressure into financial conditions. Higher yields tighten liquidity, weigh on equities, and reduce the relative appeal of non-yielding assets such as gold.

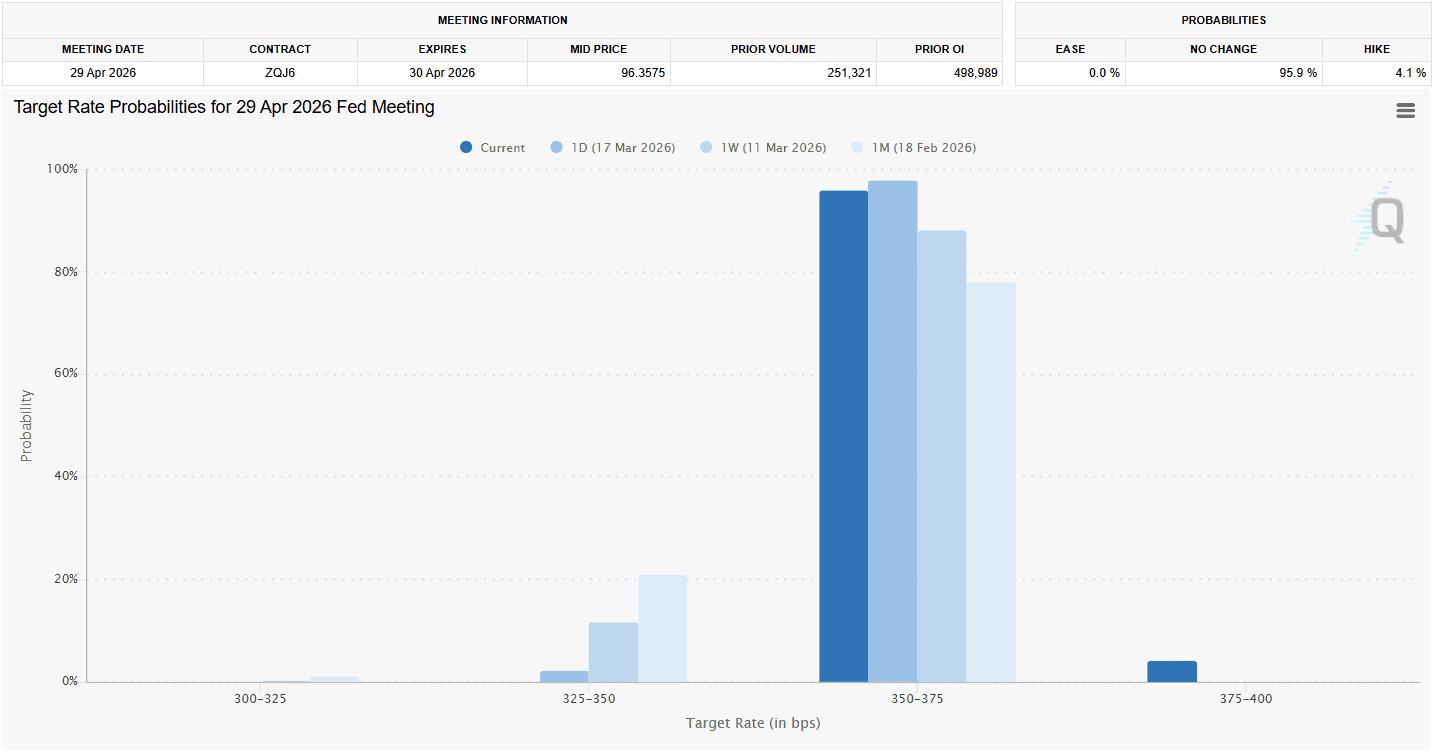

Rate Expectations: Post-FOMC vs Pre-FOMC

Changes in rate expectations are visible in current pricing.

For April:

- ~95.9% probability of no change

- ~4.1% probability of a hike

The reappearance of hike probabilities, while small, indicates reduced confidence in a smooth disinflation process.

The expected rate path has shifted higher and further out. Markets now anticipate a gradual easing cycle, with rates moving toward the mid-3% range into year-end, compared to earlier expectations of a faster decline.

This reduces the scope for policy-driven support in risk assets, as a rapid easing cycle is no longer priced.

What Matters Now

Markets are adjusting to a shift in policy expectations, not reacting to a liquidity shock. While pockets of stress are beginning to emerge in areas such as private credit, this has not yet translated into a broader liquidity event and remains a developing theme.

The key driver remains as the US yields.

- Rising yields → Continued pressure on equities and gold

- Stabilising yields → Potential consolidation, not immediate recovery

Oil remains the key catalyst.

- Elevated oil prices → Inflation risk persists → cuts delayed

- Oil pullback → Easing narrative can return

This keeps markets in a conditional state, where direction is determined by how inflation and yields evolve from here.

Bottom line: Until yields stabilise and inflation shows sustained improvement, risk assets are unlikely to regain durable upside.