Written by:

- Opening Bell

- May 12, 2026

- 4 min read

CPI Day Puts Inflation Back in Focus

Markets head into today’s US CPI release with inflation nerves creeping back into the picture, largely driven by the recent rebound in oil and gasoline prices following renewed Middle East tensions. After several months where inflation appeared to be gradually cooling, traders are now questioning whether today’s report could mark the beginning of another short-term inflation reacceleration.

Still, the broader macro backdrop looks very different from the inflation shock seen during 2021 and 2022. Wage growth has slowed, consumer demand is softer beneath the surface, and several parts of the economy continue to show signs of cooling. That’s important because it suggests today’s inflation risk may be more about energy and shelter distortions rather than a full-blown structural inflation spiral.

In other words, markets are trying to determine whether today’s CPI print represents a temporary inflation scare — or something more persistent that could force the Federal Reserve back into a more aggressive stance.

What Markets Are Watching

The key focus today isn’t just the headline CPI number itself, but how broad inflation pressures appear underneath the surface.

A headline beat driven mainly by gasoline and energy may be viewed differently from a report showing accelerating services and core inflation across the economy.

If CPI comes broadly in line with expectations, markets may interpret the data as manageable rather than alarming. In that scenario, the Fed would likely maintain its current cautious approach instead of turning meaningfully more hawkish. Treasury yields could stabilise, the US dollar may struggle to extend gains aggressively, and equities — particularly AI and growth-related names — may continue leaning on earnings momentum rather than macro fears.

A hotter-than-expected print, however, would likely force markets to further push back Fed rate-cut expectations. That could trigger a sharp move higher in Treasury yields, especially on the front end of the curve, while strengthening the US dollar as traders reprice a more hawkish Fed path. Gold and other rate-sensitive assets could come under pressure, while higher yields may weigh on growth stocks in the short term.

On the flip side, a softer CPI report could reopen the door to a more dovish Fed outlook. Treasury yields would likely move lower, the dollar could weaken, and risk appetite may improve across equities as markets revive hopes for future rate cuts.

Markets Still Leaning Toward “Temporary” Inflation

For now, markets still appear to be treating this as a temporary inflation scare rather than the beginning of another major inflation cycle.

That distinction matters.

While energy prices can create short-term volatility in headline inflation, investors will want to see whether pricing pressure is becoming more embedded across the broader economy. If core inflation remains relatively contained beneath the energy noise, markets may remain comfortable with the idea that the Fed can eventually ease policy later this year.

Today’s report could therefore become less about whether inflation ticks slightly higher — and more about whether inflation breadth begins expanding again.

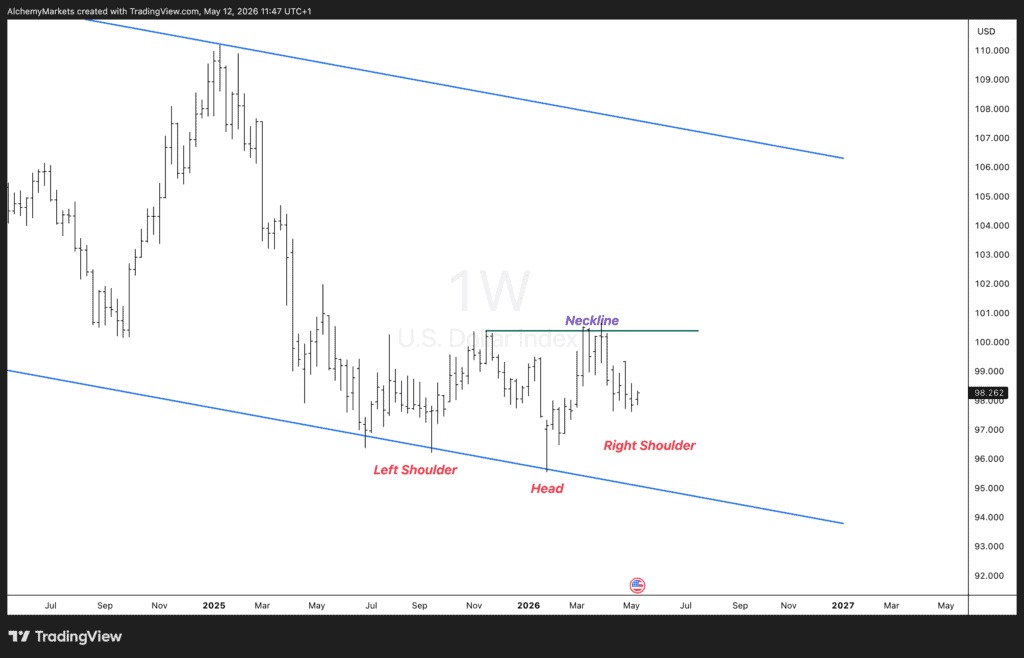

Technical Analysis: Dollar Index Watching Key Breakout Zone

From a technical perspective, the US Dollar Index is sitting at an important inflection point.

The weekly chart continues to show a potential inverse head and shoulders formation developing within the broader descending channel. The neckline sits near the 100.50–101.00 region, which remains the key breakout area traders are watching closely.

If today’s CPI data comes in hotter than expected, that could provide the catalyst for a bullish breakout in the dollar. A stronger inflation print would likely drive Treasury yields higher and reinforce expectations that the Fed keeps rates elevated for longer — a combination that could trigger the inverse head and shoulders pattern and open the door toward a larger recovery move in the DXY.

However, if CPI lands broadly in line with expectations, the dollar may struggle to generate enough momentum for a breakout. In that case, the market may continue trading sideways as investors wait for clearer direction on inflation and Fed policy over the coming months.

For now, today’s CPI report looks set to determine whether the dollar finally breaks higher — or remains stuck consolidating within its broader range.