Written by:

- Opening Bell

- March 10, 2026

- 5 min read

Oil Shock Eases, Leaving USDJPY Vulnerable to Yen Strength

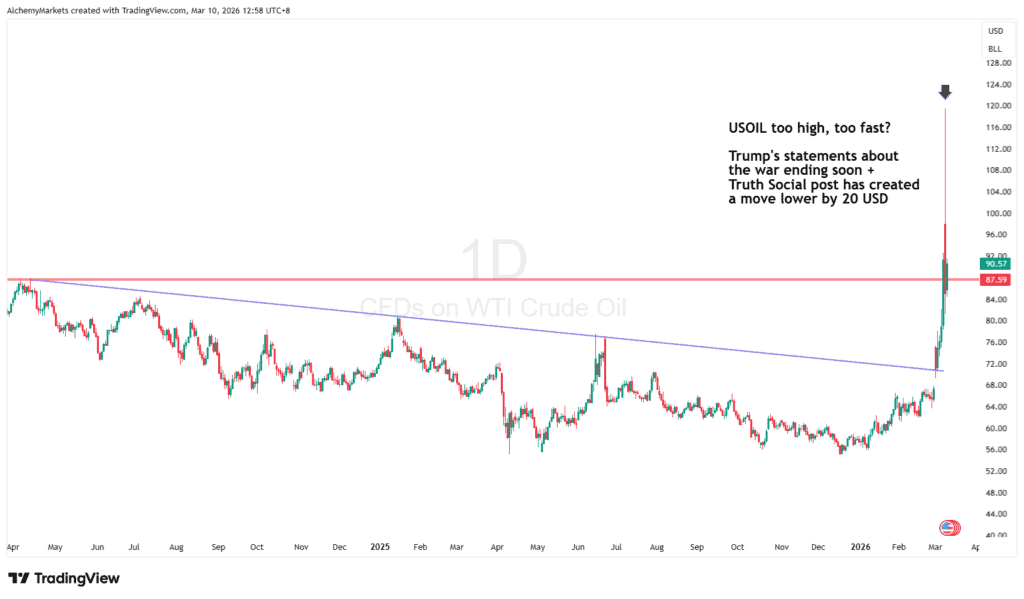

USOIL began the week with extreme volatility, surging toward 120 before reversing sharply as geopolitical headlines shifted. The rally was initially driven by fears that escalating tensions with Iran could disrupt shipping through the Strait of Hormuz, a route responsible for roughly one fifth of global oil flows.

Key highlights:

- Oil moved parabolic to around 120 as markets priced potential supply disruption through the Strait of Hormuz, which carries roughly 20 percent of global oil and LNG flows.

- The rally reversed quickly after President Trump suggested the conflict could end sooner than expected, easing fears of a prolonged supply shock.

- Markets are now highly sensitive to inflation data this week, particularly CPI, as energy prices feed directly into inflation expectations and the interest-rate outlook.

The rally was quickly punctured after comments from President Donald Trump suggested the conflict could end sooner than expected, easing fears of a prolonged supply shock. That shift in narrative triggered a rapid pullback in crude and helped stabilise broader markets.

While President Trump’s comments have helped calm oil markets somewhat, the earlier rally may simply have been too rapid to sustain. At the same time, signals from military officials have been less definitive about the conflict ending, with recent remarks about the possibility of “boots on the ground” highlighting that escalation risks have not fully disappeared.

Despite the reversal, oil remains dramatically higher than it was earlier this year, having risen from roughly 60 dollars in January to near 120 during the recent spike. This highlights how sensitive markets remain to geopolitical risk and energy supply disruptions. With energy prices now feeding directly into inflation expectations, crude has become one of the most important macro variables in the market.

Inflation and Rate Expectations

Oil spikes tend to push inflation expectations higher because energy costs feed directly into transportation, manufacturing, and consumer prices. When crude rises rapidly, markets often begin pricing fewer interest-rate cuts as central banks may need to keep policy tighter for longer.

Current market pricing reflects that caution.

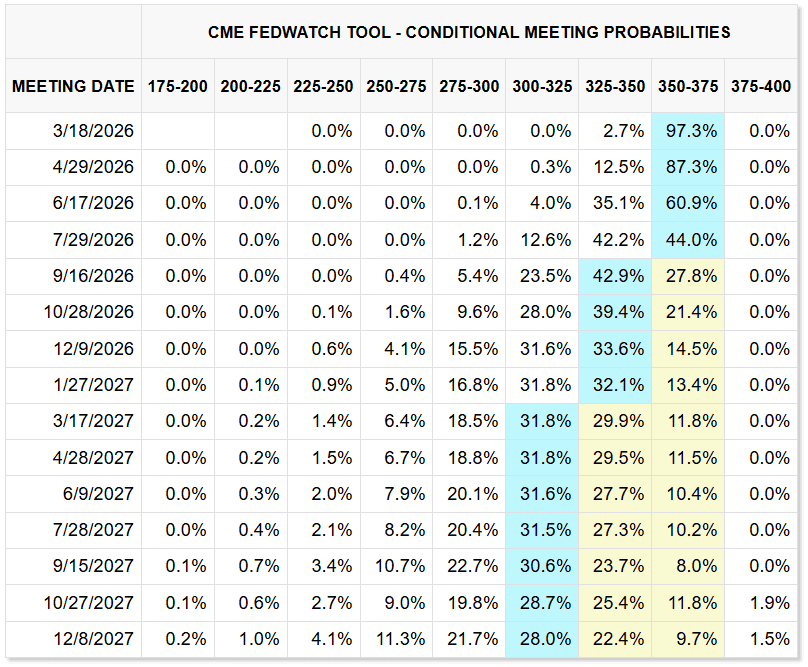

According to the CME FedWatch tool, the March FOMC meeting is expected to result in a rate hold with roughly a 97% probability. The probability of holding rates remains dominant through the April and June meetings as well.

By July, expectations become more divided. Futures pricing shows markets split of around 43% between a rate hold and the first potential cut, indicating growing uncertainty about the timing of policy easing.

Earlier this year, markets had expected the Fed to begin cutting rates sooner, with multiple cuts priced into the first half of 2026. However, resilient economic data and persistent inflation pressures have gradually pushed those expectations further out.

Strong labour market data earlier this year reinforced this caution, as continued job growth can support wage pressures and delay the Federal Reserve’s ability to ease policy.

The recent spike in oil briefly reinforced those inflation concerns, as higher energy prices can feed into headline CPI and complicate the path toward policy easing. However, the sharp pullback in crude removes some of that immediate pressure.

The next major test for this narrative will arrive with upcoming US inflation data later this week.

USDJPY and Yen Dynamics

The yen remains highly sensitive to changes in global yields and inflation expectations. When oil prices rise sharply, inflation fears tend to push global bond yields higher.

Higher yields often support the US dollar and weaken the yen, particularly as investors favour carry trades that borrow cheaply in yen to invest in higher-yielding assets abroad. In addition, crude is priced globally in US dollars, meaning a surge in energy prices can increase demand for USD as importers purchase dollars to buy oil.

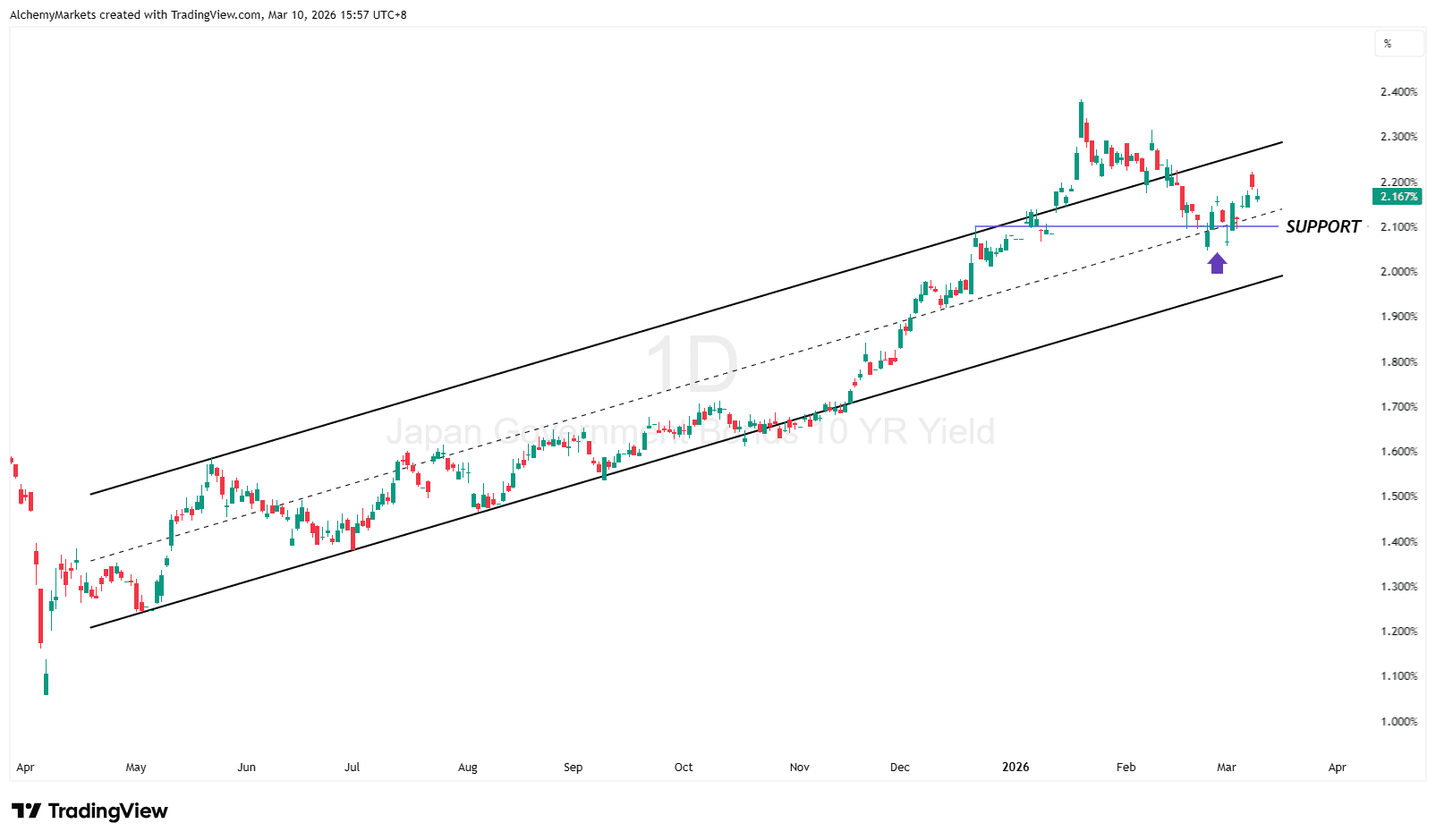

However, the recent pullback in crude may ease some of that inflation pressure. At the same time, Japanese government bond yields have been rising across the curve, which can support the yen by narrowing the yield gap with other developed markets and reducing the attractiveness of carry trades.

JP10Y Chart (Daily Timeframe)

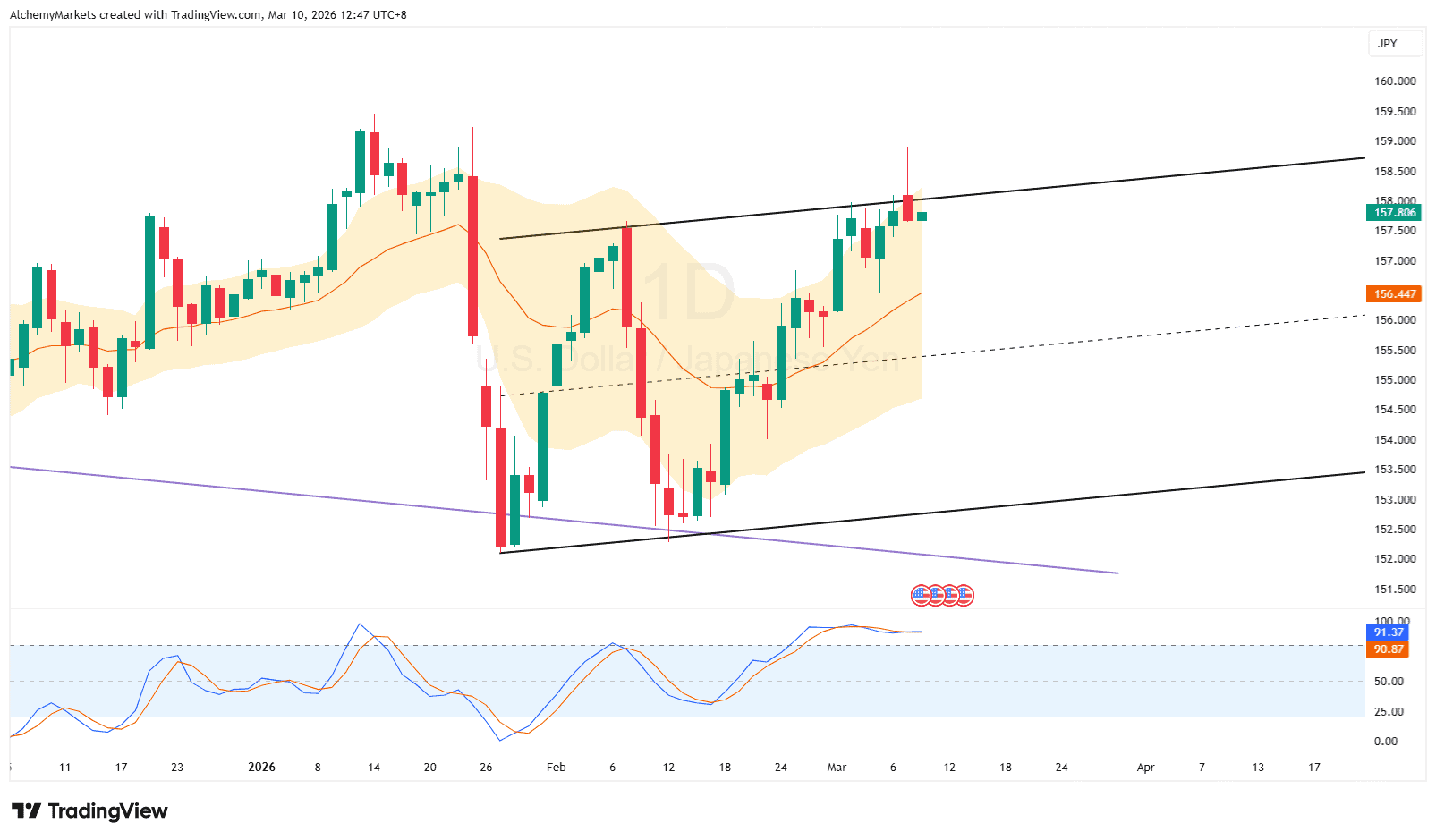

USDJPY Chart (Daily Timeframe)

Against that backdrop, USDJPY is showing signs of technical exhaustion.

The pair recently rejected the upper boundary of a rising parallel channel on the daily timeframe, printing a roughly 0.80% bearish candle. The rejection also occurred near the upper volatility bands of both the daily EMA-20 and EMA-50 (1 standard deviation), suggesting price may have become stretched relative to its short-term trend.

If the rejection develops further, it could signal strengthening yen conditions and a move back toward equilibrium levels.

Key technical levels to monitor include:

- Mean reversion toward the daily EMA-20 near ¥156.477

- The mid-range level around ¥156

- The lower boundary of the broader range near ¥153.5

Oil Remains the Market’s Main Catalyst

For now, the energy market remains the central driver of the broader macro narrative.

A sustained move higher in oil would likely revive inflation fears and support the US dollar, while continued consolidation or downside in crude could allow the yen to strengthen as markets reassess interest-rate expectations and global yield differentials.

In the near term, markets are likely to continue trading the oil–inflation–yield chain, leaving USDJPY particularly sensitive to shifts in energy prices and expectations surrounding US monetary policy.