Written by:

- Opening Bell

- April 27, 2026

- 8 min read

Five Mag 7 Earnings in 48 Hours Put AI Rally on Trial

What happens when the market races back to record highs before the biggest earnings test of the quarter?

Well, we are about to find out.

The S&P 500 has almost erased the fear from its late-March selloff, with tech and AI-linked names doing most of the heavy lifting. The recovery has been sharp, but it has also made this week much more important.

This week presents key insights into how healthy this rally is. Five of the Magnificent Seven stocks will be releasing their earnings on Wednesday and Thursday, merely within a 48-hour timeframe.

Microsoft, Alphabet, Amazon, and Meta report on Wednesday. Apple follows on Thursday. Together, these stocks carry enough weight to shape the entire market mood.

If they deliver, the breakout looks stronger. If they disappoint, even slightly, traders may start asking whether the market has already priced in too much good news.

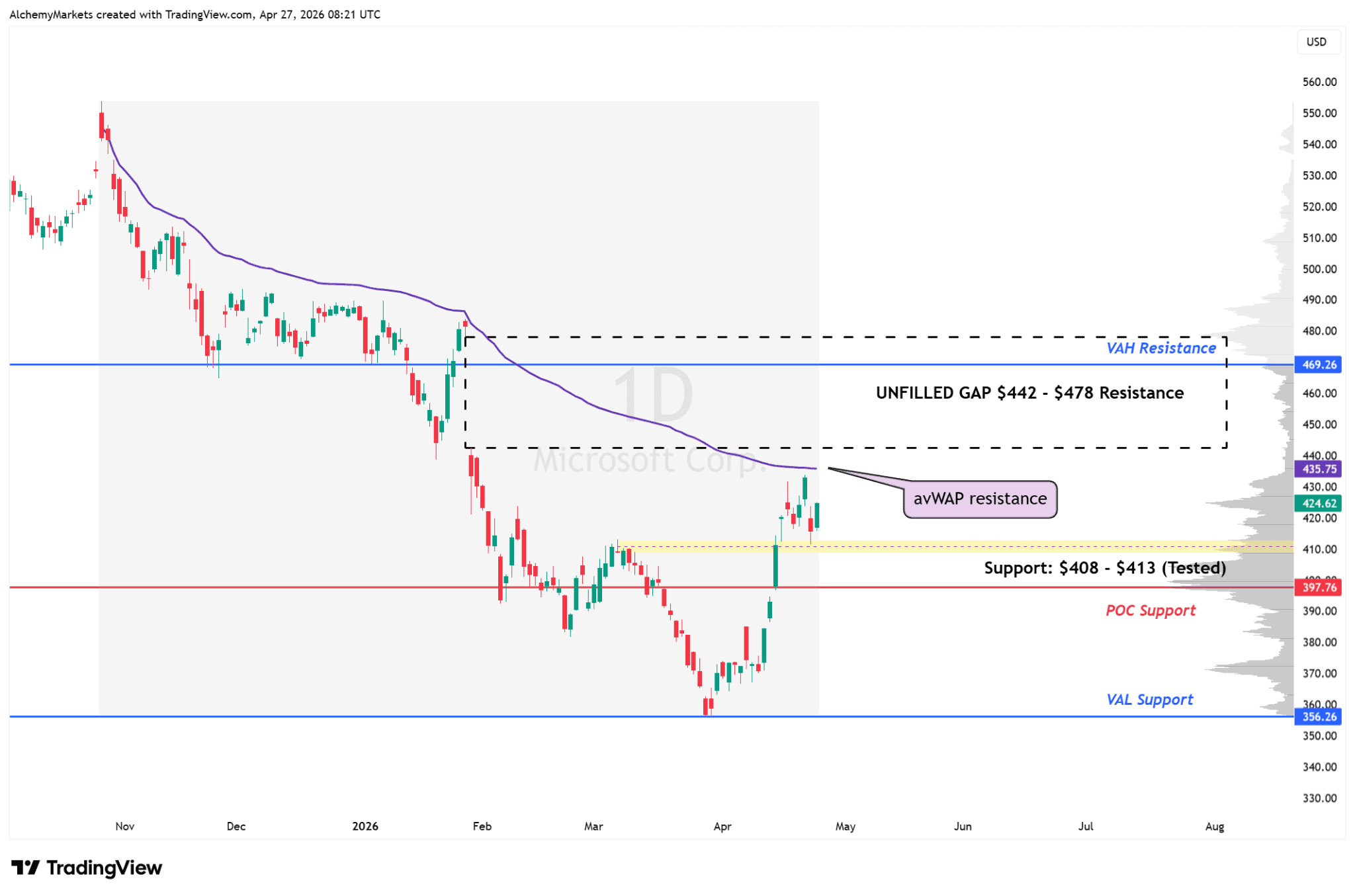

Microsoft: AI demand still needs to show up in Azure

Tools used: The chart levels below use Volume Profile and anchored VWAP tools.

Volume Profile helps show where previous trading activity was concentrated (or wasn’t), while anchored VWAP helps track whether buyers are still defending the move from an important starting point.

Microsoft’s earnings focus is Azure, its cloud computing business.

Azure is where investors look for signs that companies are still spending on AI tools, data storage, computing power, and enterprise software. If Azure growth stays strong, it supports the idea that AI is feeding real business demand, not just pushing stock prices higher.

Microsoft’s recent financials still give the stock a strong base heading into earnings:

- Revenue: $81.27B, up 16.72% year over year

- Gross profit: $55.30B, up 15.60%

- Operating income: $38.27B, up 20.92%

The chart has recovered from its April lows, but it has not fully cleared resistance.

Microsoft is holding above the tested $408–$413 support zone. As long as that area holds, the rebound remains intact. The next test is around $435.75, where anchored VWAP resistance is currently sitting.

A reclaim of $435–$436 would open the door toward the large unfilled gap between $442 and $478. That gap is where the stock previously dropped quickly, so some trapped sellers may use a move back into that area to exit.

Key levels:

- Support: $408–$413

- POC support: $397.76

- avWAP resistance: $435.75

- Unfilled gap resistance: $442–$478

The earnings focus will be Azure growth, AI demand, and whether Microsoft’s infrastructure spending is starting to pressure margins.

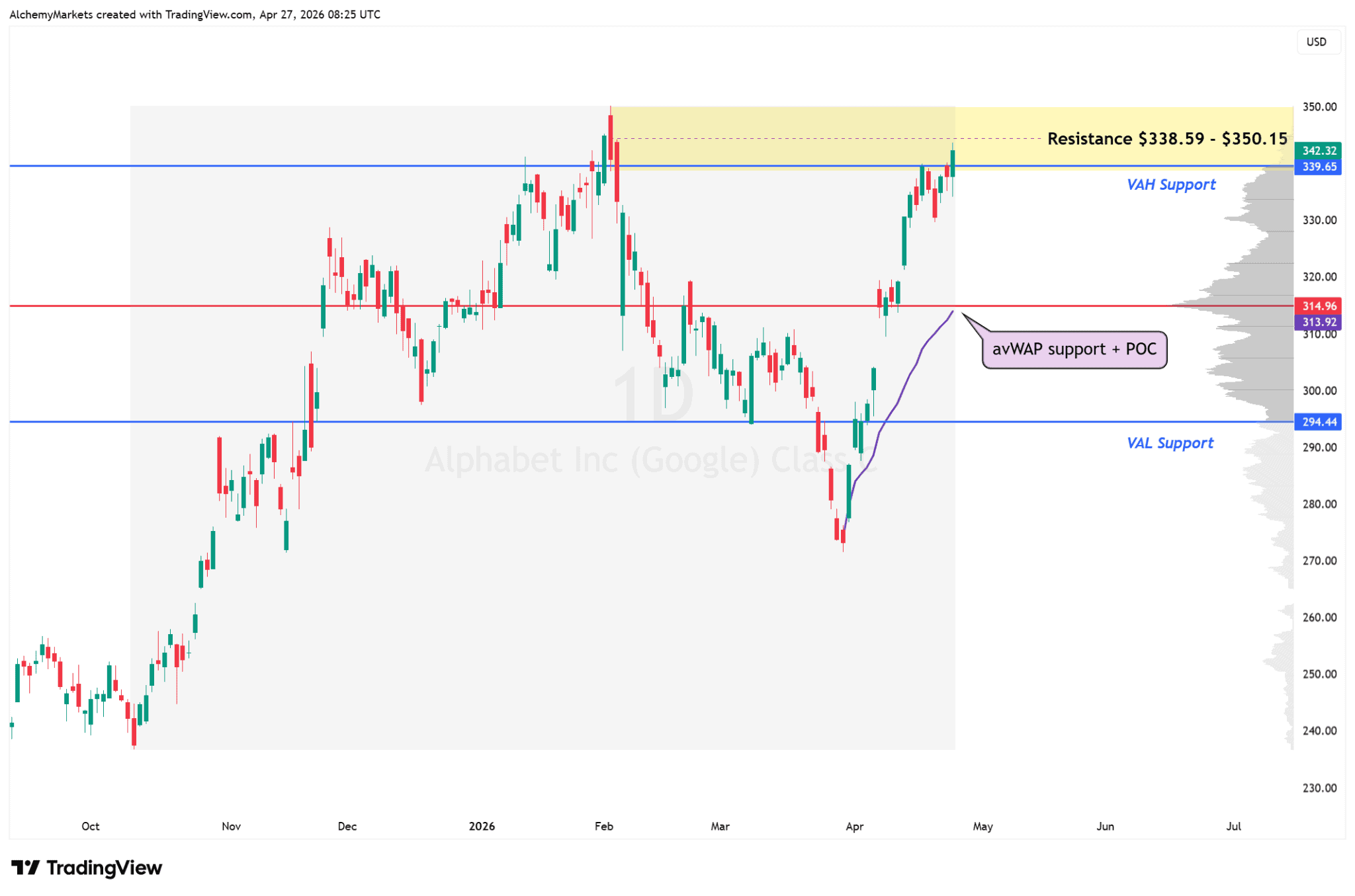

Alphabet: Google needs to prove AI is helping Search, not hurting it

Alphabet’s earnings report will likely come down to Search, Cloud, and AI spending.

Google still makes a large part of its money from Search advertising. Businesses pay to appear in front of users who are already searching for something. That model has been one of the most profitable parts of the internet for years.

AI changes the conversation. If more users start getting answers directly from AI tools, investors may start questioning how much pressure that puts on traditional search ads over time.

Alphabet’s recent numbers still look strong:

- Revenue: $114.00B, up 18.19% year over year

- Gross profit: $68.23B, up 22.20%

- Operating income: $36.10B, up 16.64%

The business is not weak. The market just wants a clearer answer on whether AI protects Google’s search advantage, improves Cloud growth, and stays manageable from a spending perspective.

The chart is sitting in a sensitive area.

Alphabet is testing the $338.59–$350.15 resistance zone, with the value area high near $339.65. A hold above this region would show that buyers are accepting the stock at higher prices again.

A rejection back into the old value area would be the warning sign.

If Alphabet falls back below that area and starts trading inside the previous range again, the breakout attempt loses quality. The next major magnet sits near $314, where anchored VWAP and point-of-control support are closely aligned around $313.92–$314.96.

Key levels:

- Resistance: $338.59–$350.15

- Value area high: $339.65

- avWAP + POC support: $313.92–$314.96

- Lower value area support: $294.44

The cleanest bullish read would be steady Search revenue, strong Google Cloud growth, and AI spending that does not sound like an open-ended cost problem.

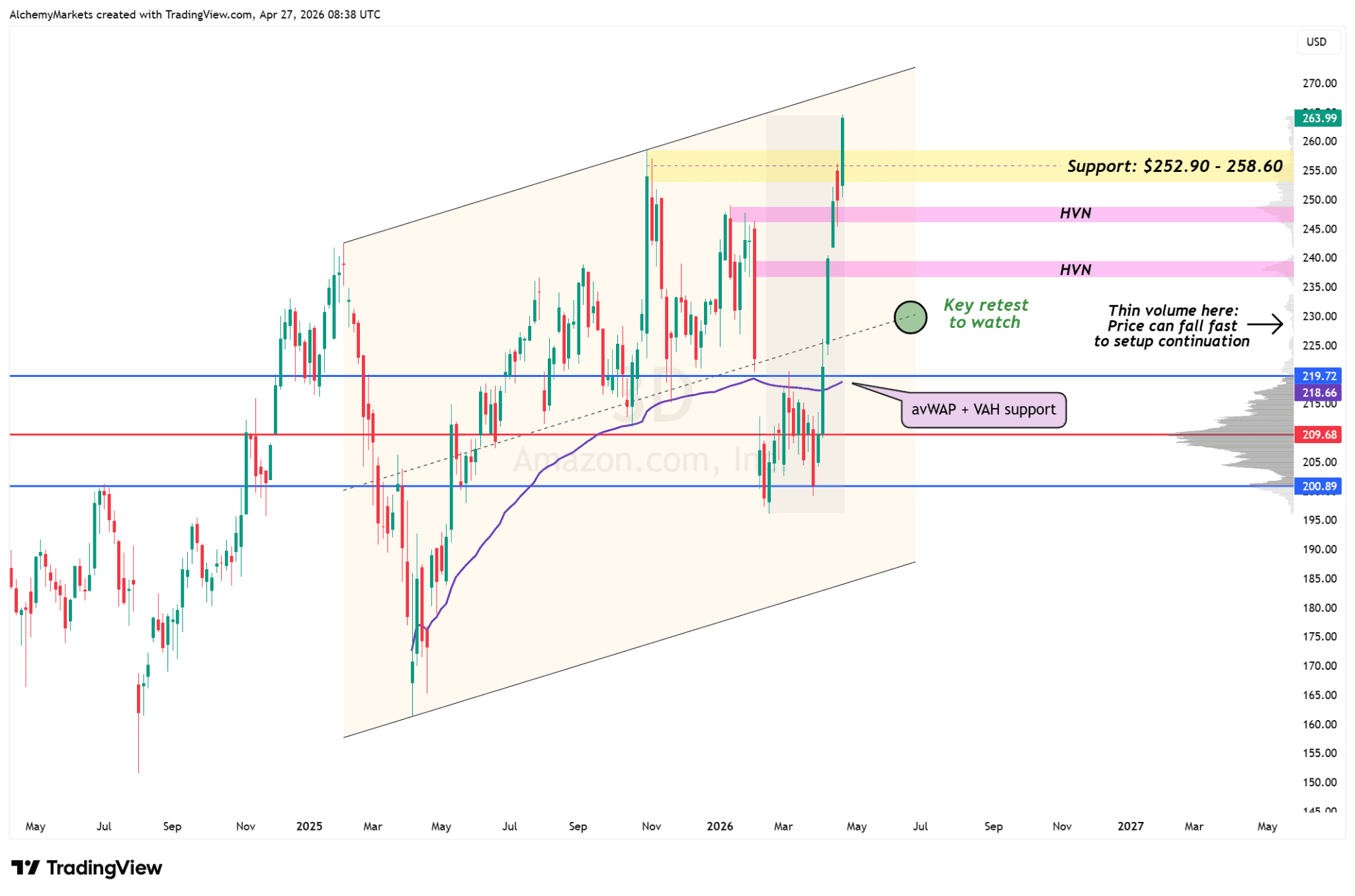

Amazon: AWS has to justify the breakout

Amazon’s earnings report will likely revolve around AWS, its cloud computing business.

AWS is one of the main reasons investors treat Amazon as an AI infrastructure stock. Companies building AI products need computing power, storage, and cloud services. AWS provides that infrastructure, which makes it a direct read on whether enterprise AI demand is still expanding.

Amazon’s recent financials show a strong base heading into earnings:

- Revenue: $213.39B, up 13.63% year over year

- Gross profit: $103.43B, up 16.34%

- Operating income: $26.23B, up 22.71%

The chart is one of the cleaner ones in the group.

Amazon has pushed above the $252.90–$258.60 zone. That area now becomes the first support area to monitor. Holding above it keeps the breakout in decent shape.

A move back below $252.90–$258.60 would make the breakout less convincing. From there, price could look toward high-volume areas near $247 and $238. A deeper failure opens the thinner volume pocket around $219–$220, where price may move faster because there has been less previous trading activity.

Key levels:

- Current support: $252.90–$258.60

- High-volume areas: around $247 and $238

- avWAP + VAH support: around $219–$220

- POC support: $209.68

The earnings focus will be AWS growth and AI infrastructure demand. A strong AWS update would support the breakout. A softer report could make the recent move look stretched.

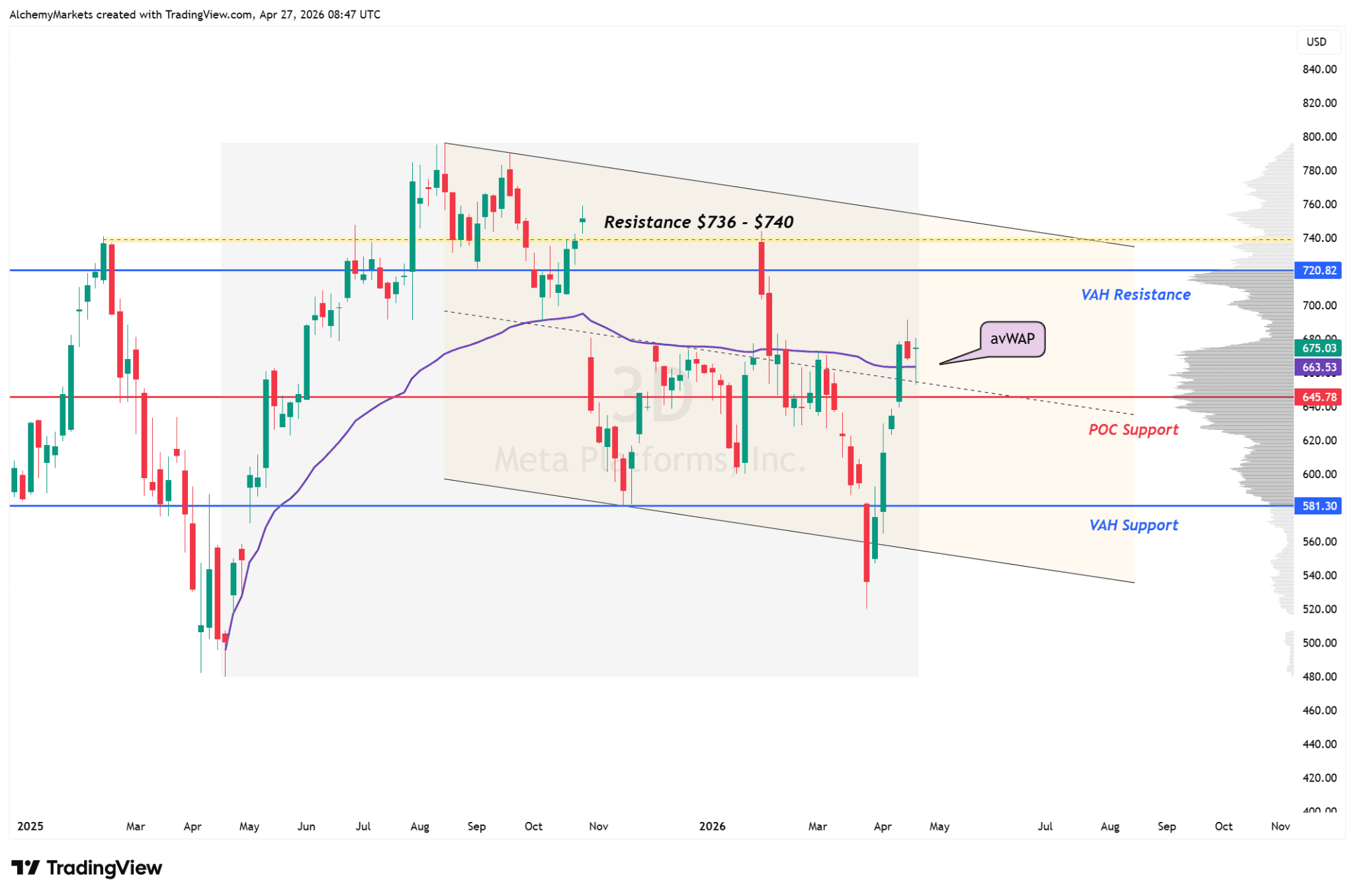

Meta: AI spending needs to strengthen the ad business

Meta’s earnings report is mainly about advertising and AI spending.

The company makes most of its money from ads across Facebook, Instagram, WhatsApp, and its wider app ecosystem. AI already helps that business through ad targeting, content recommendations, and user engagement.

That gives Meta a fairly direct AI story. Better AI can help users stay engaged for longer and help advertisers reach the right people more efficiently.

Meta’s recent financials remain strong:

- Revenue: $59.89B, up 23.78% year over year

- Gross profit: $48.99B, up 23.85%

- Operating income: $24.75B, up 5.48%

The slower operating income growth is the line to watch. Meta is spending heavily on AI infrastructure, so investors will want a clearer link between that spending and future revenue growth. Reality Labs also remains part of the cost story, which keeps pressure on management to explain the payoff.

The chart has recovered well.

Meta has reclaimed the $645.78 point-of-control area and moved back above anchored VWAP around $663.53. Buyers have taken the stock back above an important average-price reference, which improves the recovery setup.

The next test is overhead resistance. The first major level is around $720.82, followed by the larger $736–$740 zone. Until Meta clears that area, the stock still looks like a strong recovery inside a wider range rather than a clean breakout.

Key levels:

- POC support: $645.78

- avWAP area: $663.53

- VAH resistance: $720.82

- Major resistance: $736–$740

- Lower support: $581.30

The best earnings reaction would likely come from strong ad growth with a convincing explanation for AI spending. A clearer link between AI investment, ad performance, engagement, and future revenue would support the bullish case.

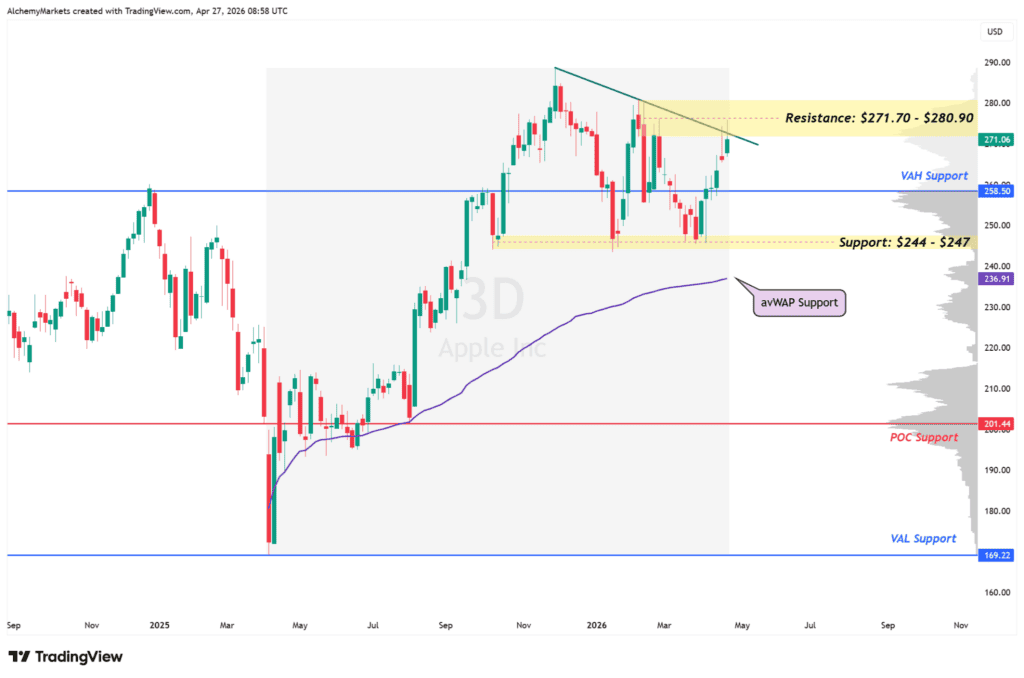

Apple: The odd one out in an AI-heavy week

Apple’s earnings report has a different feel from the other four.

Microsoft, Alphabet, Amazon, and Meta all have clearer AI links through cloud, advertising, software, or infrastructure. Apple’s AI story is less direct. Investors are still waiting to see whether Apple can turn AI into a stronger reason for users to upgrade iPhones, use more services, or stay deeper inside the Apple ecosystem.

Apple’s financials remain very strong:

- Revenue: $143.76B, up 15.65% year over year

- Gross profit: $69.23B, up 18.80%

- Operating income: $50.85B, up 18.72%

The stock is not dealing with a weak-business problem. It is dealing with a market-positioning problem. In a week dominated by AI infrastructure and cloud demand, Apple needs to show that it still belongs in the same leadership conversation.

The chart is pressing into an important decision zone.

Apple is testing resistance around $271.70–$280.90, while also pushing into a descending trendline from its prior high. A clean break above that region would make the recovery look much healthier.

If Apple fails there, the first level to watch is around $258.50. Below that, the broader support band sits around $244–$247, with anchored VWAP lower down near $236.91.

Key levels:

- Resistance: $271.70–$280.90

- VAH support: $258.50

- Support: $244–$247

- avWAP support: $236.91

- POC support: $201.44

The earnings focus will be iPhone demand, Services growth, China sales, and any update that makes Apple’s AI roadmap feel more practical. A strong quarter can support the stock, but a vague AI update may leave Apple looking like the slower-moving name in a very AI-heavy week.

Bottom line

The market has rallied first. Now earnings need to catch up.

Five Mag 7 stocks report within roughly 48 hours, and each one carries a different part of the AI story:

- Microsoft needs Azure to prove AI demand is still feeding cloud growth.

- Alphabet needs to show that AI is strengthening Search and Cloud, not creating new margin pressure.

- Amazon needs AWS to justify its breakout.

- Meta needs to connect its AI spending back to the ad business.

- Apple needs to show it still belongs in a market being led by AI-linked names.

The trend is still strong, but the setup is no longer quiet.

If these companies deliver strong numbers and confident guidance, the S&P 500 breakout gets stronger support. If the results are fine but the outlook sounds expensive, crowded, or too dependent on future AI returns, traders may start asking whether the rally moved too far before the proof arrived.