Written by:

- Opening Bell

- June 25, 2026

- 5 min read

Micron prints perfect, and now the chart has to answer

Memory’s biggest name just delivered the cleanest quarter of its life, and the most interesting thing about it is that the stock isn’t sure what to do with it.

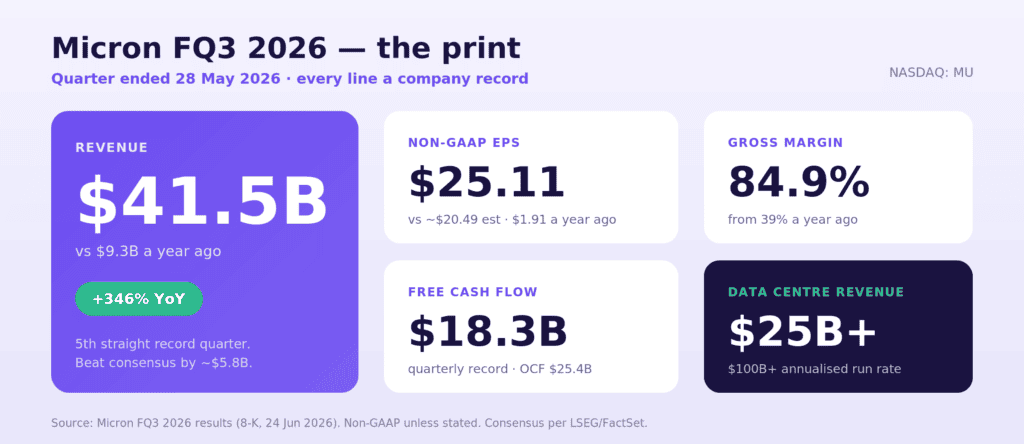

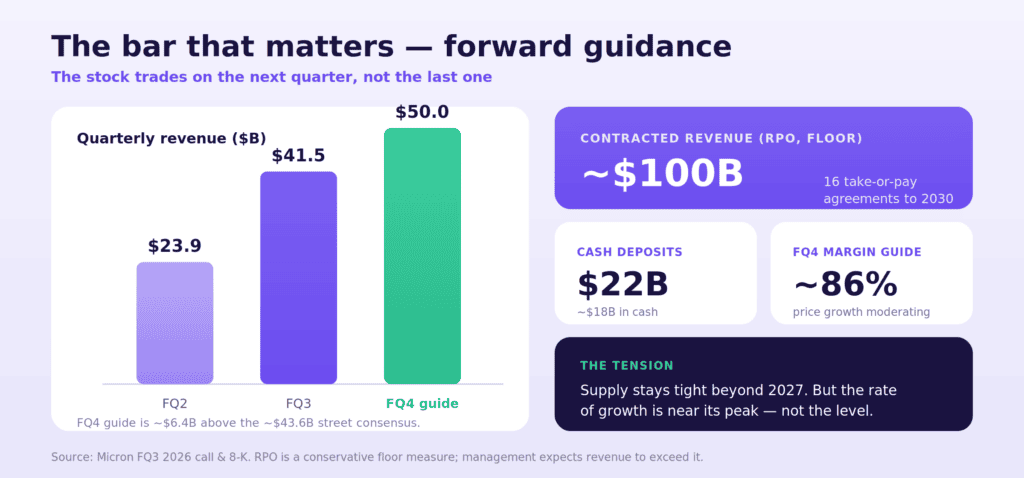

Micron closed out fiscal Q3 with revenue of $41.5 billion, up 346% on the year, a fifth straight record. Gross margin came in at 84.9%, up from 39% the same quarter a year ago. Earnings landed at $25.11 against a Street sitting near $20.49. Then management did the part that actually moves stocks: they guided the next quarter to $50 billion, roughly $6.4 billion north of where analysts were parked. On the fundamentals, there is no soft spot to pick at here. This was about as good as a print gets.

So why is the tape hesitating?

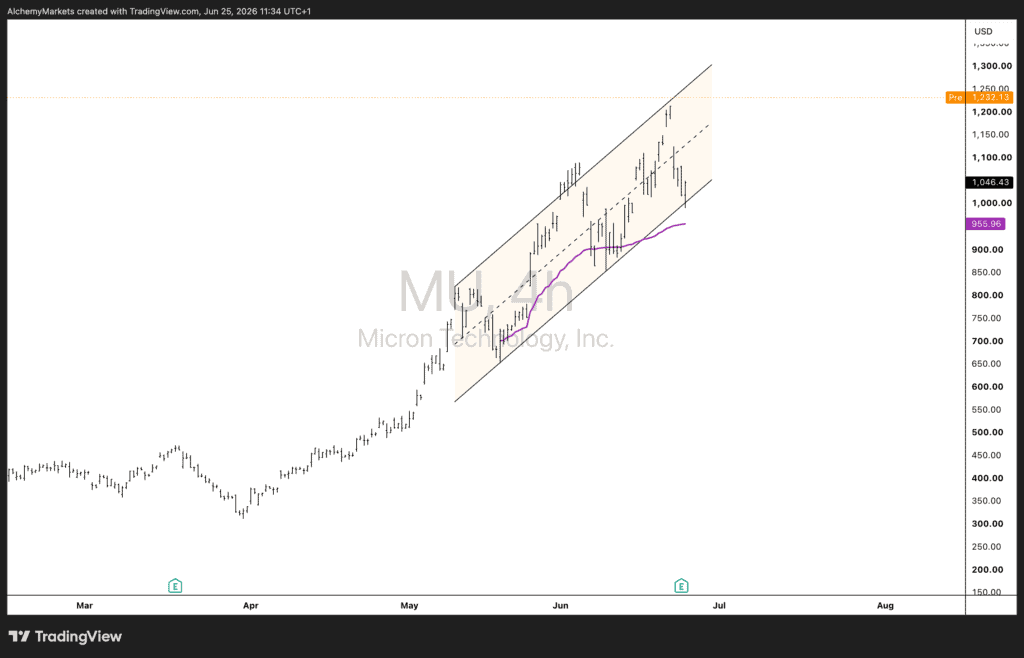

Because a stock that has run more than 700% in a year doesn’t trade on what just happened. It trades on what happens next, and on whether the best news the company had to give is already in the price. Micron spent the session before the report getting dragged 14% lower in a memory-sector selloff that had nothing to do with Micron and everything to do with nerves around AI spending and a wobble in South Korean chip names. The report landed into that anxiety. After hours, the stock spiked back toward its prior high near $1,213, and this morning it’s gapping up again, marked around the $1,218 area before the bell. The cash session, though, has been hanging in the lower half of its recent range. That gap between where the stock wants to open and where it has actually been willing to sit is the whole story today.

What’s underneath the number

The genuinely new thing in this report isn’t the revenue line, it’s the business model behind it. Micron has now signed sixteen long-term, take-or-pay customer agreements running out to 2030. Customers cannot cancel, and they pay for the volume whether they lift it or not. That’s roughly $100 billion of contracted revenue at floor prices, backed by $22 billion in deposits and financial commitments. Management was blunt that even at the floor, margins would sit above any peak the company has printed in a prior cycle.

For a business that has spent its entire public life swinging through brutal boom-bust memory cycles, that’s a structural change worth paying attention to. The floor under the company is higher and firmer than it has ever been. Supply stays tight beyond 2027 because new fabs won’t produce meaningful volume until 2028, so the pricing power isn’t going anywhere soon.

The honest caveat sits right next to it. Costs are rising as those fabs get built, and management flagged that the pace of price increases is moderating from here. Going from 39% to 85% gross margin was the easy leg. The level of earnings looks durable; the rate of growth is probably at or near its peak right now. None of that is bearish. It just means the part of the story that sends a stock vertical may be largely behind it, even as the business stays strong.

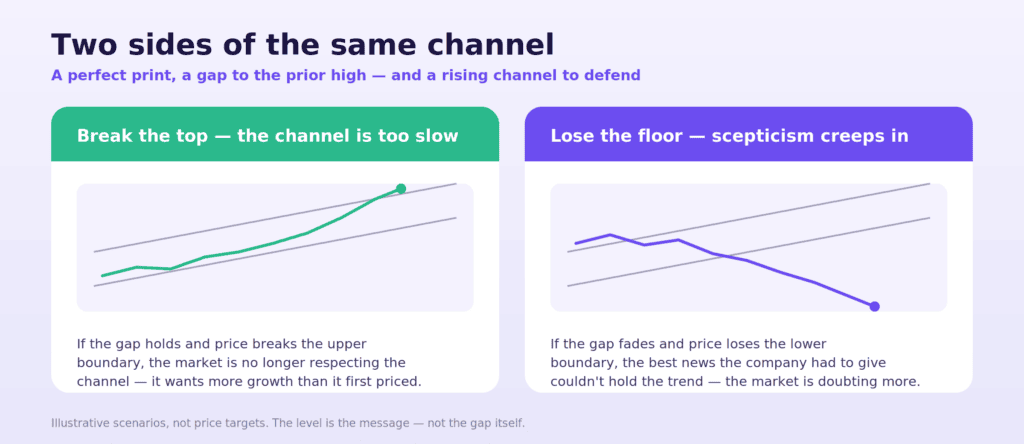

The chart: one channel, two messages

Pull up the 4-hour and the structure is clean. Micron has been climbing inside a rising channel since the April lows, the moving average riding the lower boundary near 956, price working between that floor and the upper rail. The cash session has it sitting around 1,046, in the middle-to-lower half of the channel. The pre-market, though, is marked up near 1,227, pressing toward the upper boundary and just under the prior high. That gap between where the stock closed and where it wants to open is the setup, and it cuts both ways.

The bullish read. If the gap holds and price pushes through the upper boundary, the message is that the market has decided the channel is too slow. The rising trend that has governed this stock since spring would no longer be containing it. That’s the tape effectively saying the contracted-revenue, supply-tight story is worth more growth than it had originally been pricing in, and that even a perfect print wasn’t fully reflected yet. A break of the top rail on this kind of news is the market re-rating its own expectations higher.

The bearish read. If the gap fades and price slips back to test, then lose, the lower boundary, that’s a very different signal. It would mean the best quarter in the company’s history, with the strongest guide it has ever issued, couldn’t keep the stock inside its own uptrend. When unambiguously great news can’t hold the trend, it tends to mark the moment the last buyer has stepped in. The people who chased the gap are immediately offside, and the channel that was support becomes the thing that breaks. That’s scepticism showing up in price even while the fundamentals look spotless.

The level is the message, not the gap. A green open on a blowout is neither bullish nor bearish on its own. What matters is whether price can defend the channel it has respected for two months, or whether it gives it back. Watch the boundaries, not the headline.

The takeaway

The earnings settled the fundamental question and opened a cleaner one. Micron’s results were excellent and its forward visibility is the best it has ever been. But the tape is now adjudicating something the income statement can’t: whether the market still expects acceleration, or whether it’s quietly deciding that perfect was the peak. The channel will tell you which, and it should tell you soon.