Written by:

- Opening Bell

- March 9, 2026

- 4 min read

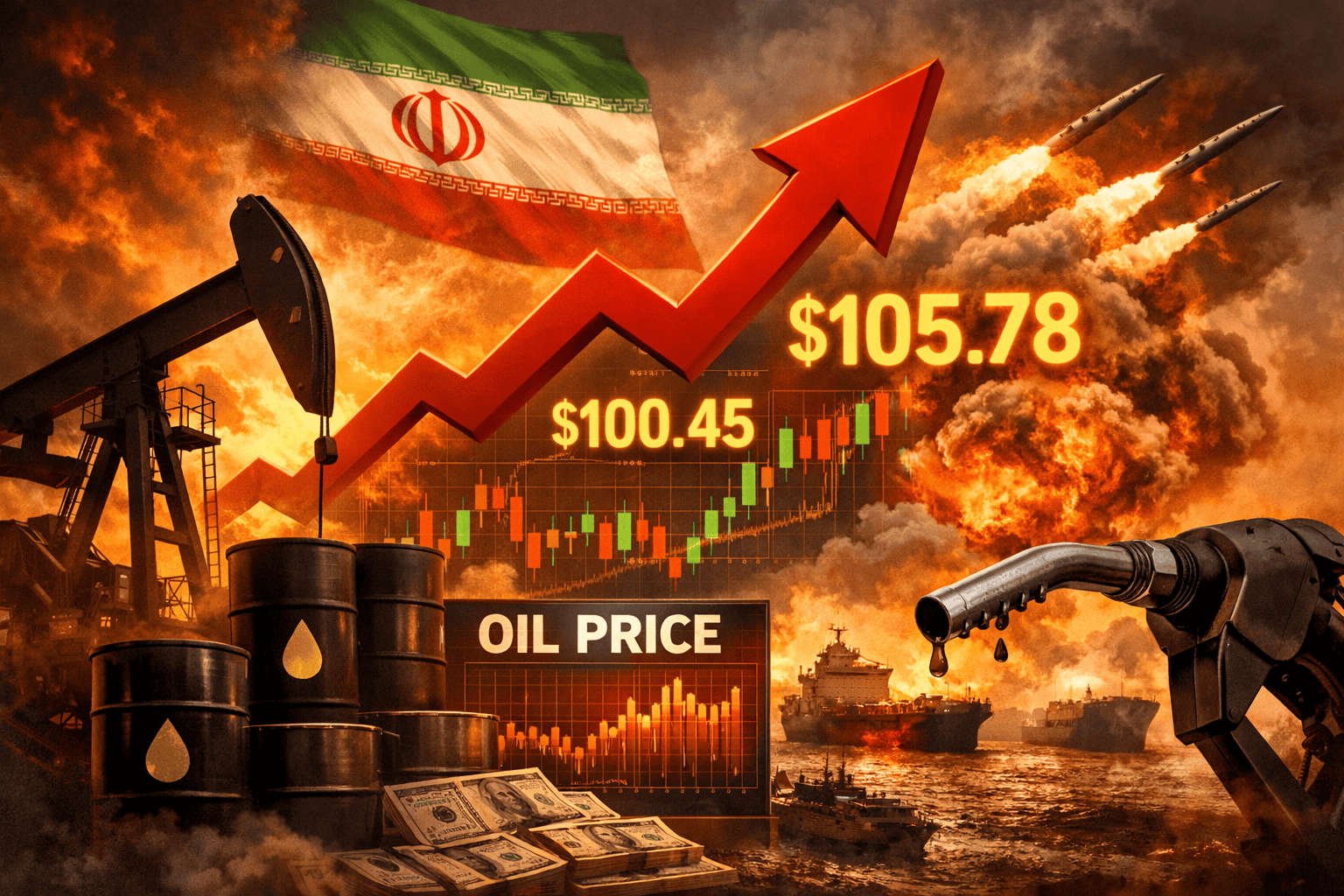

Oil Rally Gains Momentum as Supply Risks Build

Oil prices surged above $100 per barrel this morning as markets begin to price in a longer and more serious supply disruption in the Middle East. With tensions escalating and several Gulf producers already cutting output, traders are increasingly concerned that the global oil market could face tighter supply for longer than initially expected.

Below is a breakdown of the key macro drivers and the technical picture supporting the move.

1. Macro Drivers: Supply Disruptions Push Oil Higher

Oil markets reacted strongly after a weekend that brought no signs of de-escalation in the Middle East conflict. Instead, developments suggest the situation may be deteriorating further, raising the risk of a prolonged disruption to global oil supplies.

Several major producers in the Persian Gulf have already begun reducing output due to storage constraints and logistical challenges.

- Iraq has reportedly cut production by roughly 1.5 million barrels per day.

- Kuwait has reduced output by around 300,000 barrels per day.

These cuts are occurring while flows through the Strait of Hormuz — a key artery for global oil shipments — remain disrupted. As long as crude cannot move freely through the strait, the market will continue pricing in tighter supply conditions.

Even if the situation stabilizes quickly, bringing production back online takes time, meaning supply disruptions could linger.

For now, governments appear reluctant to intervene.

The International Energy Agency (IEA) has said there are no immediate plans for a coordinated release of strategic oil reserves, while the European Union has also indicated that tapping government stockpiles is not yet necessary. However, if prices continue rising and supply tightens further, pressure for emergency releases will likely increase.

Interestingly, speculative positioning has been relatively cautious. Data shows money managers reduced their net long positions in Brent last week, suggesting many traders were hesitant to take on risk ahead of the geopolitical escalation. Open interest has also fallen to its lowest level since December, highlighting the uncertainty across energy markets.

At the same time, disruptions to crude supply could also tighten refined product markets. Refineries — particularly in Asia, which relies heavily on Persian Gulf crude — may have to reduce operating rates, potentially supporting refined product margins and fuel prices in the coming weeks.

2. Technical Picture: Oil Appears to Have Bottomed at $55

While geopolitical tensions are driving the immediate move, technical signals suggest oil may have already established a longer-term bottom.

The chart shows that crude spent much of the past year building a base between roughly $55 and $80 per barrel. The $55 level repeatedly acted as strong support, suggesting the market may have completed a long consolidation phase after the earlier downtrend.

More recently, prices have broken above the upper range around $75–$80, signaling a potential shift in momentum.

From a technical perspective, this breakout supports the macro narrative of tightening supply.

The next major level to watch sits much higher — around $120 to $130 per barrel, which represents a major historical resistance zone.

However, markets rarely move in straight lines. After the sharp rally toward $100, a short-term correction or consolidation would be normal. Such a pullback could help the market digest recent gains before attempting another move higher.

The key question now is whether the combination of geopolitical risk and tightening supply will be strong enough to push oil through that $120–$130 resistance zone.

If supply disruptions persist and prices hold above the recent breakout levels, the path toward those higher levels becomes increasingly plausible.

For now, the market’s message is clear: oil appears to have already bottomed — and the next phase of the cycle may be underway.