Written by:

- Chart of the Day

- September 16, 2025

- 3min read

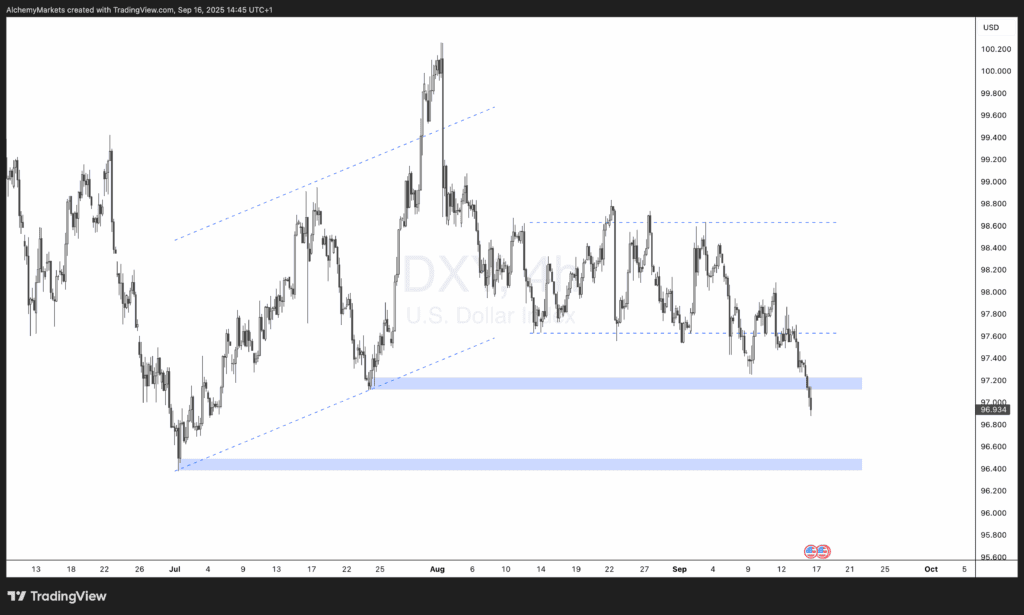

Dollar Index Hits Multi-Month Projection at 97.200, Risks Extend to 96.500

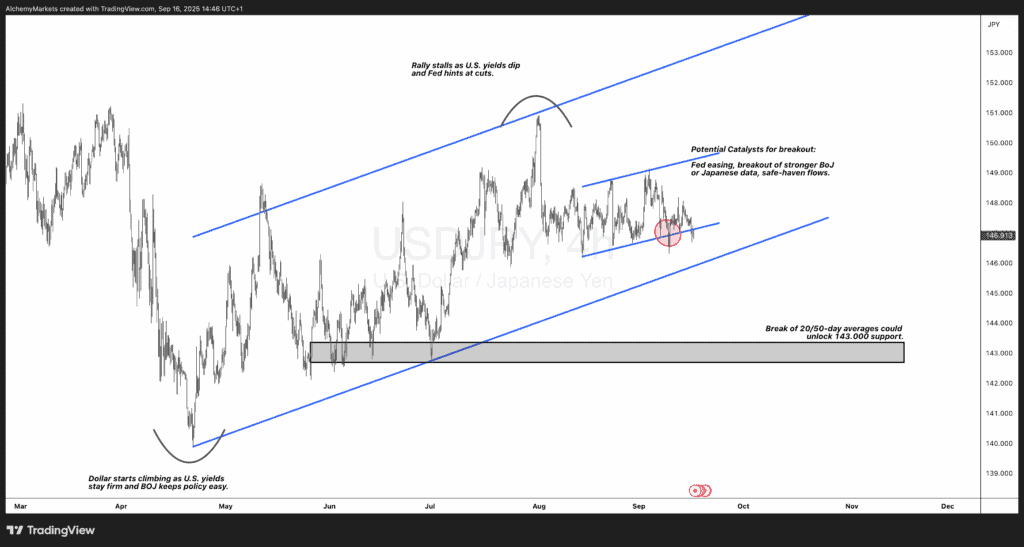

The dollar has started the week on the soft side, slipping into our multi-month projection at 97.200. This has been a well-flagged decision level, and the breach now opens the door to the next support region at 96.500. Part of the softness reflects pre-positioning ahead of tomorrow night’s FOMC meeting, where markets are fully priced for a 25bp Fed rate cut. But the external environment is also working against the greenback.

Global equity markets continue to grind higher on a mix of resilient business optimism and the growing prospect of lower global borrowing costs. Hopes of progress in U.S.–China relations are adding fuel as well, with Presidents Trump and Xi expected to hold direct talks on Friday over the future of TikTok’s U.S. operations. Chinese assets remain well supported, and USD/CNH is edging back toward its lows for the year, underscoring a broader shift away from the dollar.

Carry trade dynamics are another headwind. Over the summer, high-yielding currencies have drawn strong demand, with the Turkish lira a standout. Yesterday’s news that a key political court case has been postponed until late October gave investors additional comfort, driving the lira higher and delivering fresh returns for carry traders. In effect, investors are being rewarded twice—through elevated interest differentials and nominal FX appreciation—at the expense of the dollar.

Elsewhere, even the traditionally resilient USD/JPY has been drifting lower. Political developments in Japan are at play here, with the entry of Shinjiro Koizumi into the LDP leadership race seen as more moderate compared to rivals favoring looser monetary and fiscal policy. While we still expect USD/JPY to gravitate toward 145 over the coming weeks, the near-term path looks choppier, adding further nuance to the dollar’s weakening profile.

Back in the U.S., headline risks have been limited. Fed Governor Lisa Cook’s regained voting rights after a court ruling haven’t moved the needle for markets. The focus remains on U.S. retail sales and import prices due today. Retail control group sales are expected to show a steady 0.4% MoM gain, pointing to a still-resilient consumer backdrop. Meanwhile, import price data will be scrutinized to determine who is ultimately absorbing tariff costs—exporters, corporate margins, or end-consumers. Our bias is that tariffs will, in time, filter through to consumers.

Technical View

The U.S. Dollar Index (DXY) has now completed its multi-month downside projection at 97.200, a level we’ve been monitoring closely as a potential inflection point. The price action shows a decisive break below the recent consolidation range, suggesting that this level may have acted more as a staging ground than a durable base.

With downside momentum accelerating, the focus now shifts towards the next decision level at 96.500, which marks a broader support cluster and could serve as the next area of interest for market participants. A sustained close below 97.200 increases the probability of a deeper pullback into that zone.