Skriven av:

- Opening Bell

- februari 11, 2026

- 4 min läsning

NFP Today, CPI Friday Will Decide Market Moves

Starting off the day, we finally get the delayed Nonfarm Payrolls print, landing at 13:30 GMT just ahead of the U.S. cash open.

With CPI following on Friday at the same time, markets will be forced to reassess both growth and inflation within 48 hours.

These readings will decide for the market what to expect from the Federal Reserve heading into March; and therefore, set the trading bias and tone until then.

Labour Market Stabilising, Not Accelerating

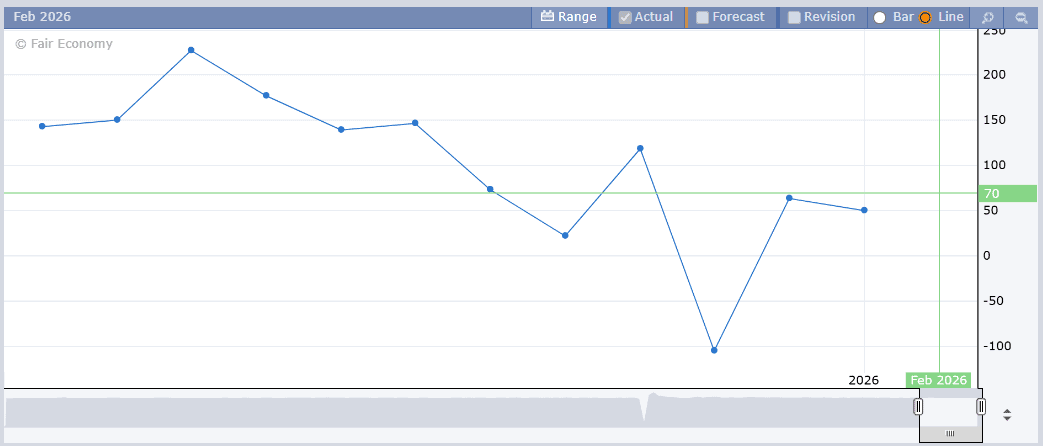

Source: Forex Factory, Green line highlights the NFP Jobs expectation

| Previous NFP Jobs added: 50k Unemployment rate: 4.4% |

| Forecast Jobs added: ~70k Unemployment rate: 4.4% Average hourly earnings: +0.3% m/m |

Consensus suggests a modest pickup in hiring compared to the previous print. That points to stabilisation rather than acceleration. The labour market is not collapsing, but it is not overheating either.

An in-line print near 70k probably sends markets back to technical structure rather than triggering a fresh macro repricing.

Hawkish scenario (USD gains strength):

If payrolls print meaningfully above 80k to 90k, especially alongside firmer wage growth, markets may lean toward a higher-for-longer rate narrative. That scenario likely supports the dollar and puts some pressure on gold, while equities could struggle near resistance.

Dovish scenario (USD weakens):

If payrolls come in below 60k, particularly with softer wages, rate cut expectations may be pulled forward. That tends to support gold and risk assets, provided markets interpret it as cooling rather than cracking.

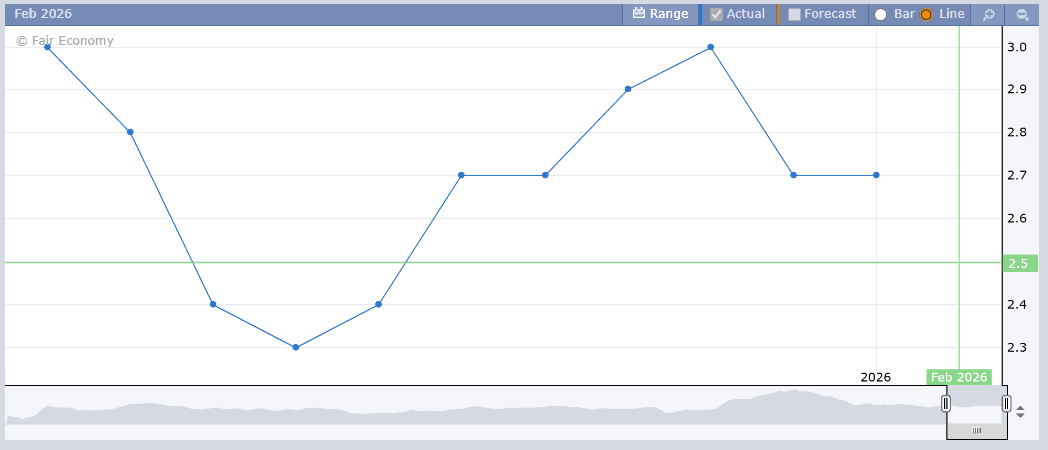

Inflation Still Drifting Lower

Source: ForexFactory, Green line highlights the CPI y/y expectation

| Previous CPI 2.6% YoY |

| Forecast 2.5% YoY |

Inflation has been trending lower, but gradually. The market expects that trend to continue.

Hawkish Scenario (USD gains strength):

If CPI surprises higher, particularly back toward 2.7% or above, markets will question whether inflation is truly under control. That likely supports yields and the dollar while creating pressure for gold and potentially equities.

Dovish Scenario (USD weakens):

If CPI prints below 2.5%, that reinforces the disinflation narrative and strengthens the case for eventual policy easing. In that environment, yields may soften, the dollar could ease, and both gold and equities may find support.

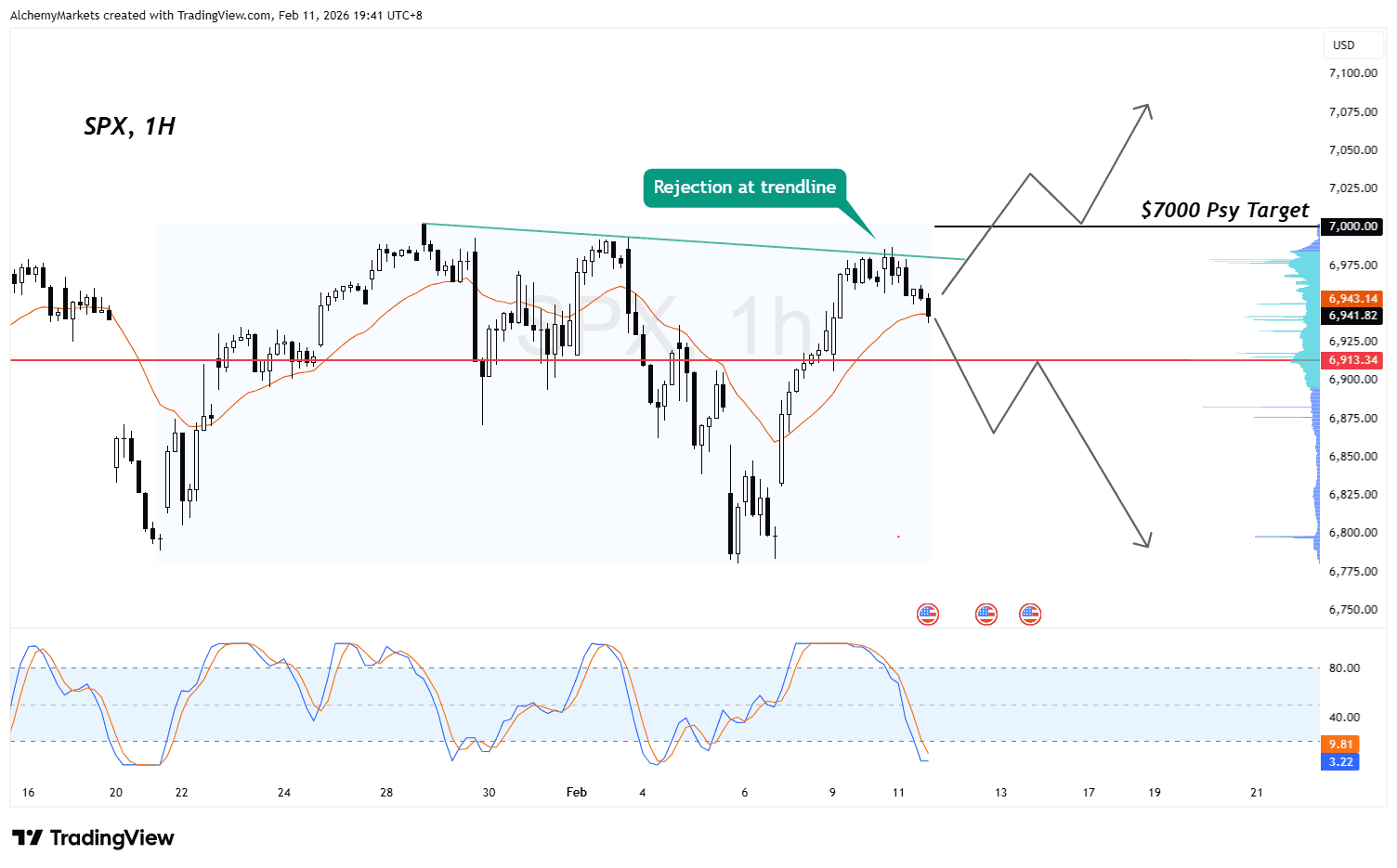

S&P 500 1-Hour Chart Analysis

On the 1H timeframe, the index continues to respect the 20 EMA and is currently compressing after a mild retracement. Stochastic RSI is near oversold territory, suggesting the market is coiling ahead of the data.

If NFP disappoints modestly and CPI follows softer, a push higher from current levels becomes plausible.

If payrolls materially beat expectations, especially above 90k, upside may struggle as markets reassess rate cut timing.

Equities want balance. Not too hot. Not too weak. The sweet spot remains a stable labour market combined with cooling inflation.

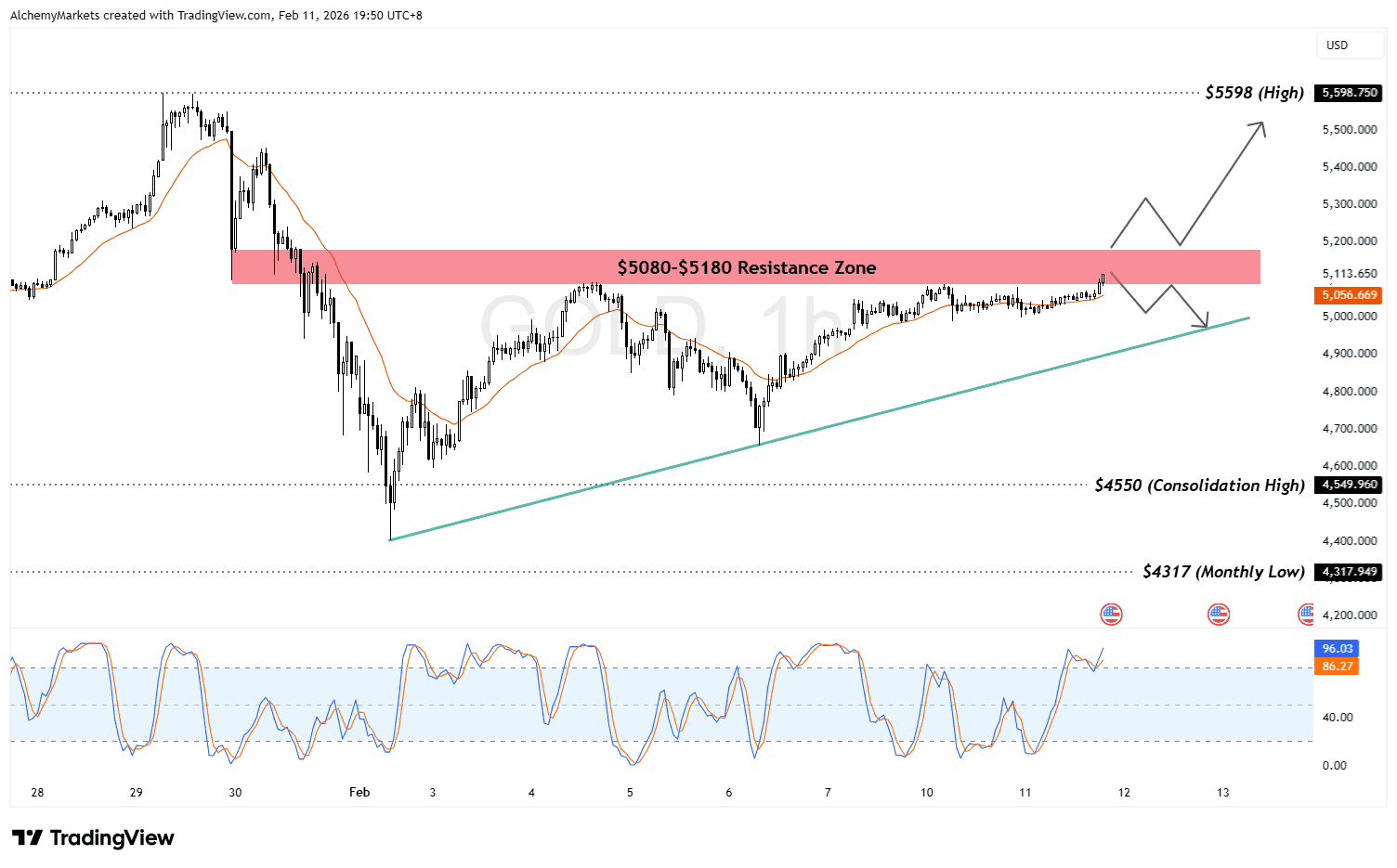

Gold 1H Chart Analysis

Gold continues to respect the 1H 20 EMA and is grinding into resistance between 5080 and 5180.

Momentum indicators suggest elevated reversal risk, but compression does not rule out a breakout attempt if macro conditions align.

A weaker jobs print today would strengthen the case for upside continuation, particularly if CPI on Friday also prints below 2.5%.

A stronger NFP print likely leads to short-term rejection, with the rising trendline near 5000 acting as structural support if price pulls back.

Gold’s direction this week will largely hinge on yields. If yields move lower, gold has room. If yields push higher, resistance may hold.

Bottom Line: Side A vs Side B

Side A says the labour market is stabilising and inflation continues to cool. That keeps the soft-landing narrative intact and supports risk (Equities and gold higher, USD lower).

Side B says inflation remains sticky and growth is resilient enough to delay easing. That favours the dollar and challenges gold and equities.

Both outcomes remain possible — we need to remain patient and observe data this week.

As always, this is not financial advice. We’re simply providing a framework for navigating event risk in a week where both growth and inflation expectations are being tested simultaneously.