Scritto da:

- Opening Bell

- Aprile 30, 2026

- 6 min di lettura

Jerome Powell’s Final FOMC Speech: Hawkish, and More Political

“Thank you very much, everyone, and I won’t see you next time,” Jerome Powell said, smiling as he waved to reporters at the end of his final post-FOMC press conference as Fed Chair.

The meeting concluded with a warm, wholesome quip from a central banker not exactly known for theatrical exits, and a room full of warm smiles and laughter.

For many traders, yesterday’s Fed meeting felt like a farewell message to a Fed Chair who has shaped the market’s thinking for years. It also signalled that a change is coming, whether that change proves major or mostly symbolic still remains to be seen.

Powell had some choice words this time around, and he sounded unusually political by central-bank standards.

Perhaps because this was his final Fed meeting as Chair, he appeared more willing to leave a stronger message behind. Not just about inflation or interest rates, but about what he believes the Federal Reserve needs to protect after he steps away from the Chair role.

Powell made clear that while he will remain on the Board, he does not intend to become a “shadow chair” once Kevin Warsh takes over. He also stressed that rate decisions should remain separate from political pressure, even if elected leaders naturally prefer lower interest rates. That was the sentimental part of the meeting, but it was also the market-relevant part.

Warsh did not speak, but his presence was felt through the handover. Powell’s comments suggested he wants the transition to look orderly, rather than like a second power centre forming inside the Fed.

In simple terms, Powell’s message was this:

- Rates were left unchanged, with the Fed still viewing current policy as appropriate.

- Inflation remains the priority, with Powell repeating the goal of bringing inflation back toward 2%.

- Oil is becoming harder to ignore, especially as Middle East risks keep energy prices in focus.

- The labour market is cooling, but not breaking, giving the Fed room to wait rather than rush into cuts.

- Fed independence was the emotional centre of the meeting, with Powell stressing that policy should not bend to political pressure.

- Warsh did not speak, but the transition to his leadership is now part of the market conversation.

Powell did not give markets a clean green light for aggressive rate cuts. He also did not sound ready to restart tightening.

Instead, the Fed remains stuck in the middle (neutral). Inflation is still above target, oil is adding uncertainty, growth is holding up, and the labour market is soft enough to watch but not weak enough to force action.

For forex markets, that keeps the focus on yields and the US dollar.

Yields Are Doing the Talking

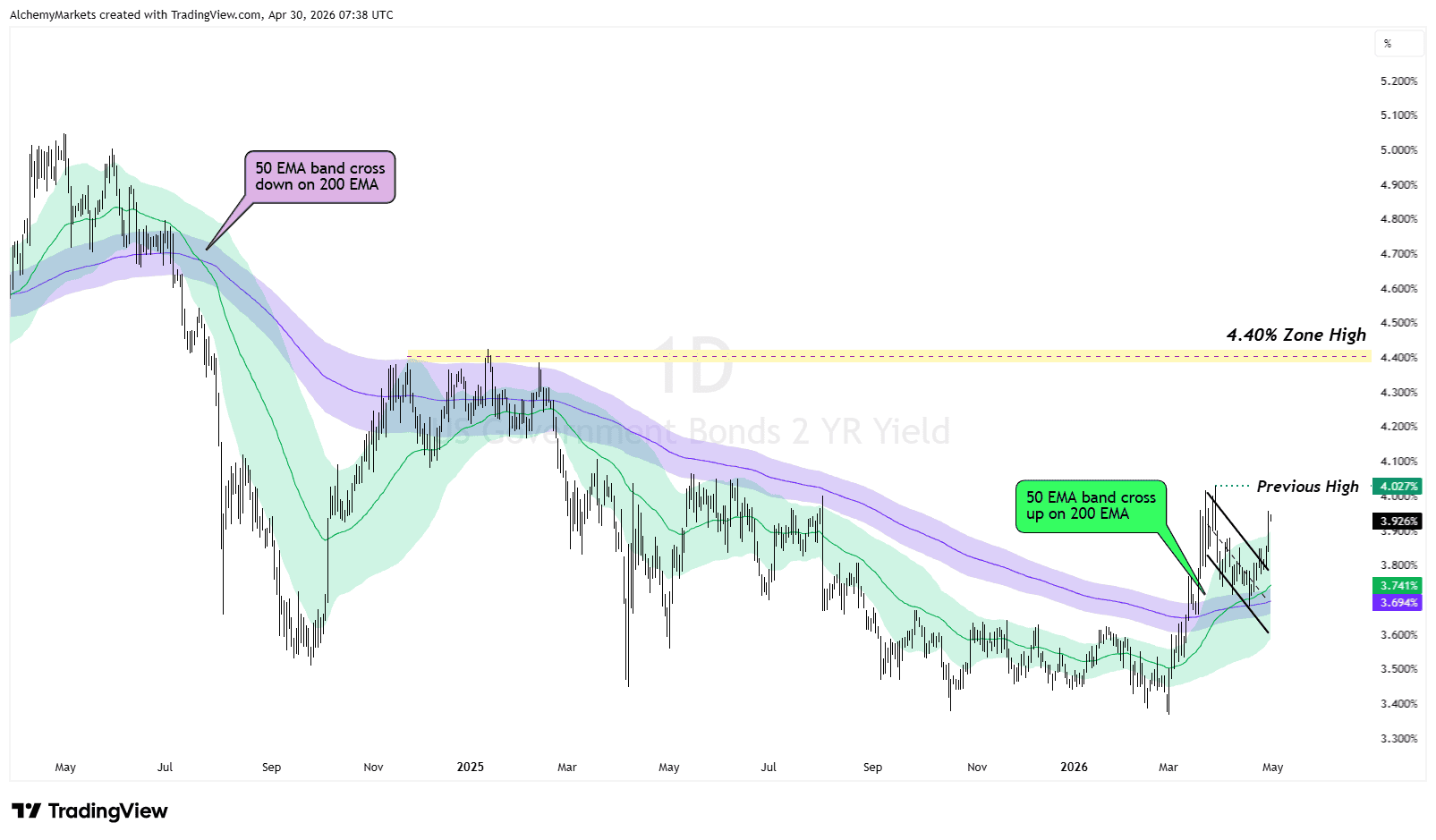

The bond market reacted less like it heard a dovish Fed, and more like it heard a Fed that still needs time. In response, the 2-year yield has broken out of a bull flag pattern, and is continuing towards 4.027%, its previous high.

Traders are starting to price a Fed that may stay restrictive for longer, even if Powell avoided sounding outright hawkish. It suggests markets are questioning whether rate cuts are really as close as previously expected.

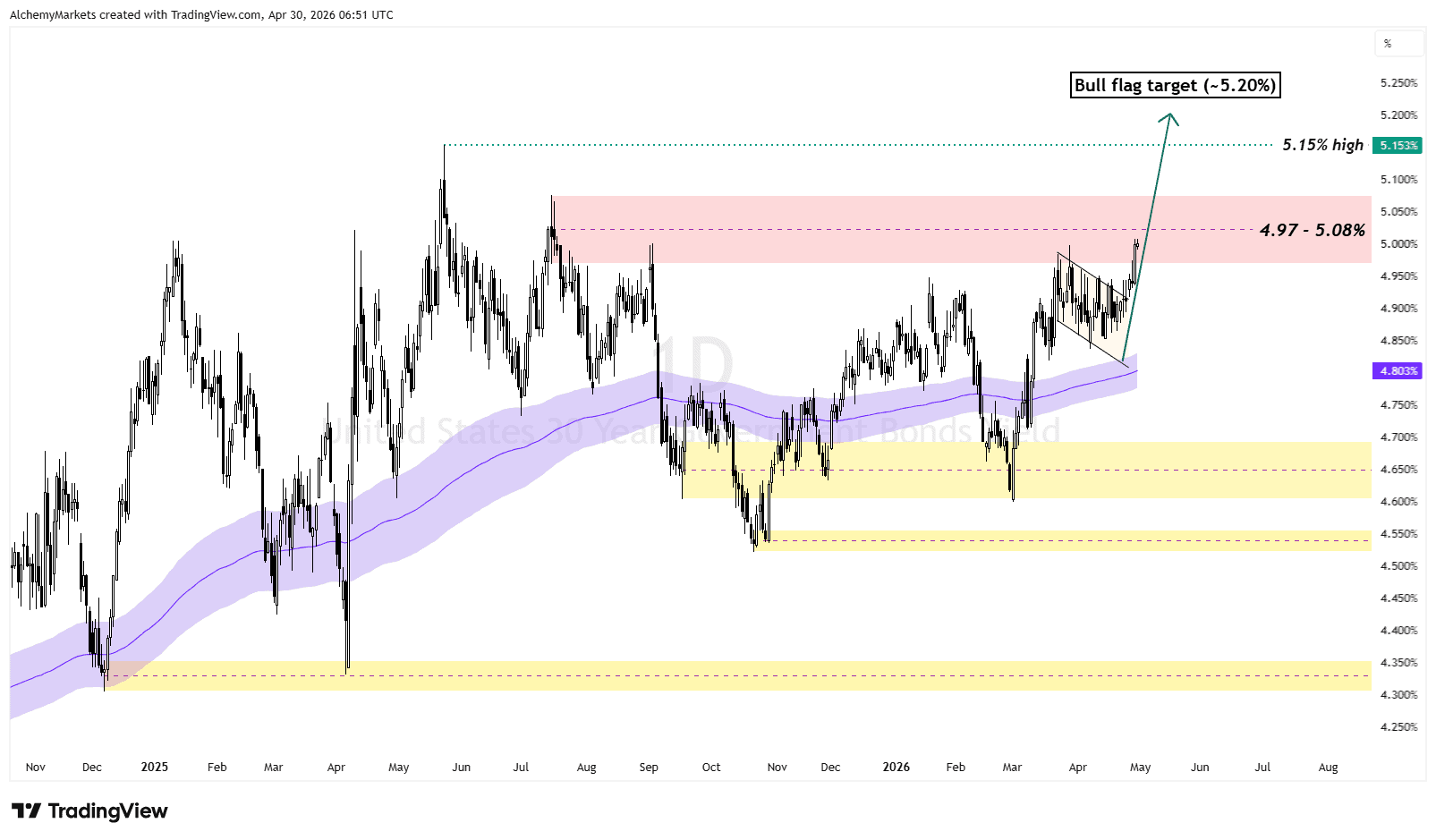

Following a bull flag breakout, the 30-year yield is also pressing into the 4.97% – 5.08% zone, which is where the inflation and fiscal-risk story becomes harder to ignore. If that area breaks, the chart still carries continuation risk toward the 5.15%–5.20% region.

Unlike the 2-year, the 30-year is not just reacting to Powell. It is also reacting to oil, inflation risk, debt supply, and whether investors still want long-term US bonds at these yields.

So even if Powell tried to sound balanced, the bond market heard enough to question the cut story.

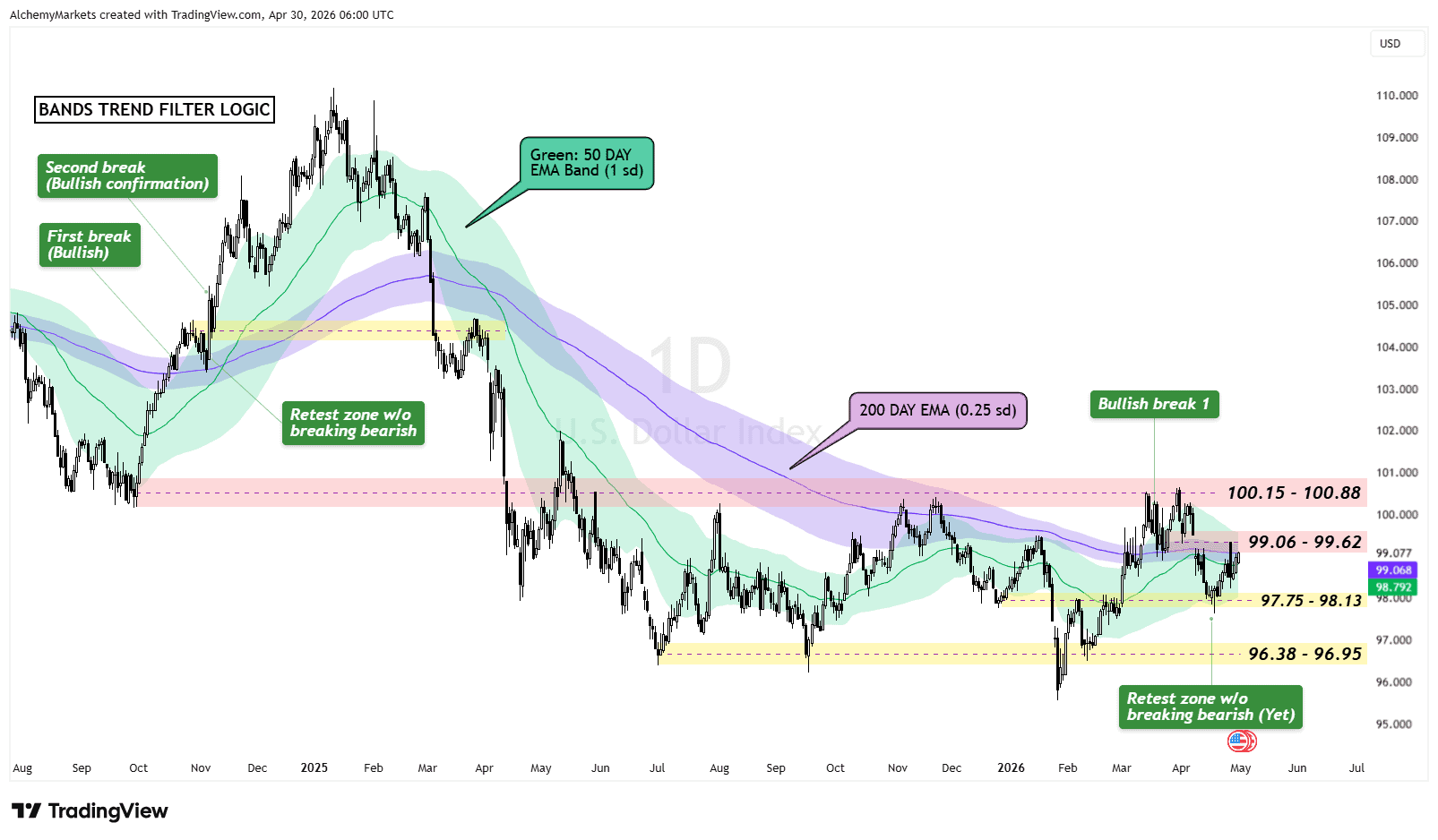

DXY: The Dollar Is Trying to Stabilise

The US Dollar Index has held the 97.75 – 98.13 support zone and is now pushing back into the 99.06 – 99.62 resistance. This is where dollar buyers need to prove the move is more than a relief bounce.

A test of 99.06 – 99.62 is only the first checkpoint, for a stronger signal of a bullish dollar, a break of the zone 100.15 – 100.88 is required. A break there would suggest the dollar is starting to rebuild trend strength, not just retracing.

If DXY fails around 99.06–99.62, the move still looks corrective. A drop back below 97.75–98.13 would keep the wider bearish structure intact.

| DXY zone | Market meaning |

| 97.75–98.13 | Key support. Holding this keeps the rebound alive. |

| 99.06–99.62 | Current retest zone. First major test for dollar buyers. |

| 100.15–100.88 | Bigger confirmation area for a stronger recovery. |

| Below 97.75 | Rebound likely fails, keeping the wider downtrend active. |

Oil Keeps the Fed Cautious

Oil is the problem that stops the Fed from sounding comfortably dovish.

If oil keeps climbing, traders will worry that inflation pressure spreads back into transport, food, and production costs. That makes the Fed’s path toward 2% inflation less clean.

The awkward part is that higher oil can pressure growth and inflation at the same time.

If energy prices rise while growth remains resilient, the Fed has less reason to cut quickly. But if oil starts hurting consumers and businesses, the economy could weaken while inflation stays uncomfortable.

That is the kind of backdrop that keeps currencies sensitive to every move in yields.

Labour Is Softer, But Not Weak Enough

The labour market is not strong enough to make the Fed confident, but it is not weak enough to force a cut either.

Powell noted that unemployment has been broadly stable, while job gains have remained low. That points to a labour market that is cooling, but not breaking.

For markets, this keeps the Fed in wait-and-see mode.

There is no clean labour-market excuse for an aggressive dovish pivot yet. Until that changes, yields and inflation data can keep doing most of the work for the dollar.

What This Means for Other Forex Markets

| Pair | Market read |

| EUR/USD | Vulnerable if US yields keep rising, though ECB inflation concerns may slow euro downside. |

| GBP/USD | Caught between sticky UK inflation and softer growth. A yield-supported dollar could pressure cable. |

| USD/JPY | Higher US yields support upside, but yen weakness keeps BOJ or intervention risk in the background. |

| USD/CAD | Mixed. USD strength supports upside, but higher oil can support CAD and cap the move. |

| AUD/USD | AUD may hold if the RBA stays cautious, but it remains exposed if higher yields hit risk sentiment. |

| NZD/USD | Similar to AUD, but usually more fragile. It needs central-bank support and stable risk appetite. |

| USD/CHF | Mostly dollar-yield driven for now, unless risk-off demand pulls flows back into CHF. |

Bottom Line

Powell’s final Fed meeting was not just about holding rates.

It was a farewell moment, a defence of Fed independence, and a reminder that the inflation fight is not finished. Warsh did not speak, but the market is already preparing for what the next Fed era could look like.

For the dollar, the next signal comes from yields.

If the 2-year yield keeps pushing higher and DXY clears 99.06 – 99.62, the dollar can continue its recovery toward 100.15 – 100.88. If DXY fails at resistance and falls back below 97.75 – 98.13, the rebound likely remains another retest inside the broader downtrend.