Written by:

- Weekly Outlook

- February 21, 2026

- 3 min read

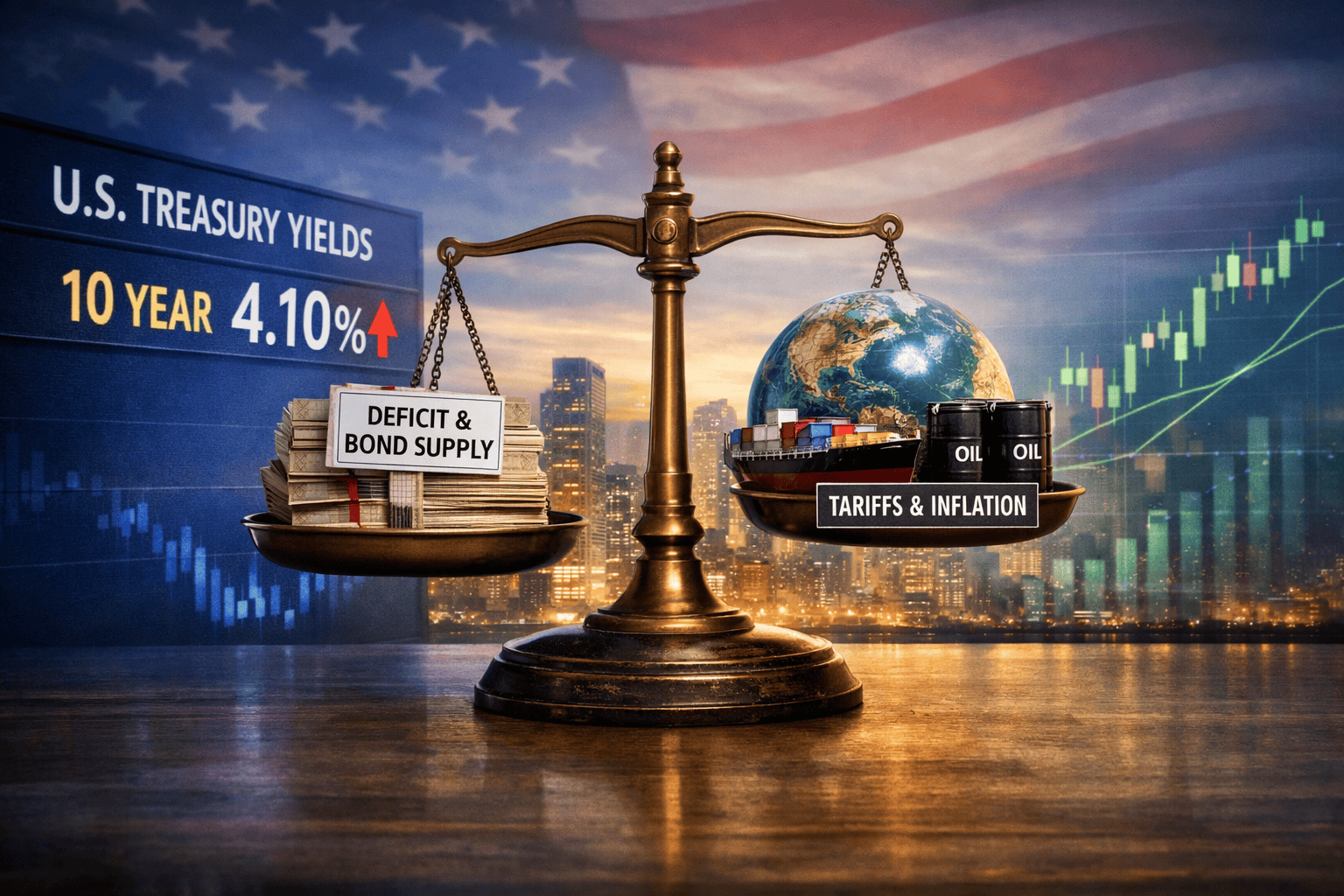

Yields Drifting Higher as Fiscal Risks Re-Emerge

Markets reacted calmly but cautiously to the recent US Supreme Court ruling, with the clearest move seen in US government bonds. The 10-year US Treasury yield has edged back towards 4.10%. It’s not a dramatic shift, but it reflects growing unease about what this means for the fiscal deficit and future bond supply.

Fiscal Risks Back in Focus

The key issue is the US deficit. Tariff revenues have recently helped soften concerns around government borrowing. While the deficit remains high, actual outcomes have been slightly better than the same period last year, largely thanks to tariff income. That has reduced pressure on the US Treasury to issue more long-dated bonds.

If those tariff revenues fade, however, the funding gap widens. That could mean more bond issuance down the line, particularly at the longer end of the curve. More supply typically means higher yields.

The next question is inflation. If tariffs are reintroduced in another form – which remains the base case for many analysts – inflation risks stay elevated. If Congress resists extending tariff powers, inflation pressure could ease, but that would leave a bigger revenue shortfall to fill.

On balance, fiscal risk looks like the dominant force. That suggests further upside pressure on yields, with the 10-year potentially drifting towards 4.25%. We could also see the yield curve steepen again, with the 2-year versus 10-year spread moving back towards 75 basis points.

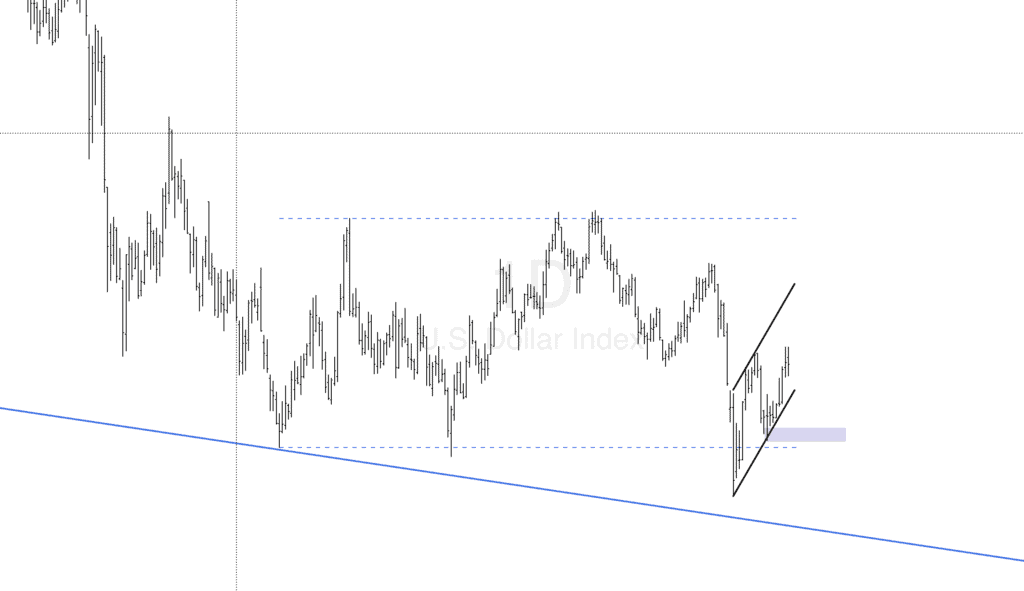

FX: Softer Dollar, but Risks Remain

The US dollar is slightly weaker on the news. Pro-cyclical currencies – those that benefit from global growth – are leading gains. Scandinavian currencies and the Australian dollar are outperforming, reflecting a modest “risk-on” tone.

However, uncertainty remains high. The legal process could drag on for months. Meanwhile, the Canadian dollar and Mexican peso may underperform given that USMCA trade renegotiations are due in July.

There is also a separate geopolitical risk to watch: Iran. Any escalation that pushes oil prices $10–20 per barrel higher would likely strengthen the dollar again, particularly given the US advantage as a major energy producer. That would quickly challenge the current pro-growth narrative.

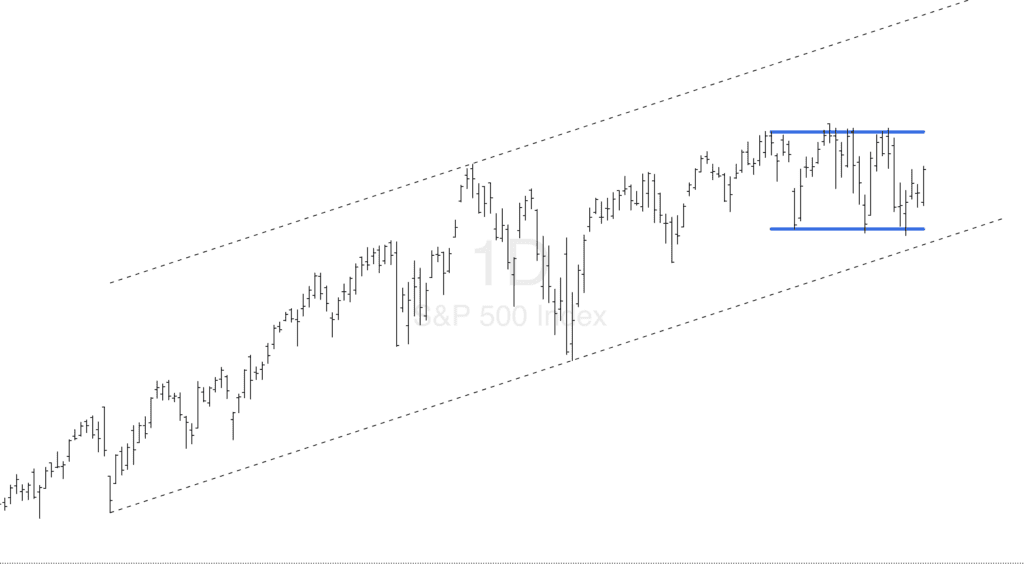

Equities: Rotation Theme Still Intact

Equity markets have so far welcomed the prospect of reduced tariff pressure on corporate margins. US futures are up roughly 0.7%, while Germany’s DAX futures are also firmer.

There are signs that international investors are already rotating away from US equities. Recent European Central Bank data showed strong foreign buying of eurozone equities late last year. As long as energy prices remain stable, that rotation into non-US markets could continue.

The key risk to this theme would be a spike in oil prices or a renewed tariff escalation.

Data Watch: Limited Catalysts

This week’s US calendar is relatively light. The main focus will be:

Producer Price Inflation (Friday) – Markets continue to price two Federal Reserve rate cuts in 2025 despite relatively hawkish January meeting minutes. A surprise here could shift that view.

Consumer Confidence (Tuesday) – Sentiment remains under pressure due to tariff worries and a cooling labour market. However, higher-income households continue to support spending, keeping the “K-shaped” recovery dynamic intact.

Bottom Line

For now, markets are balancing modest optimism in equities against renewed fiscal concerns in bonds. Yields are drifting higher, the dollar is soft but fragile, and global equities are benefiting from hopes of tariff relief.

That balance could shift quickly. Fiscal sustainability, inflation trends, and geopolitical risk – particularly around energy – will set the tone for the weeks ahead.