Written by:

- Weekly Outlook

- July 11, 2026

- 3 min read

The Deadline Nobody’s Watching

Everyone in this market is staring at the same three letters this week. CPI. That’s fair, it’s the headline event, but there’s a quieter clock ticking in the background that matters just as much for a currency pair like USD/CAD.

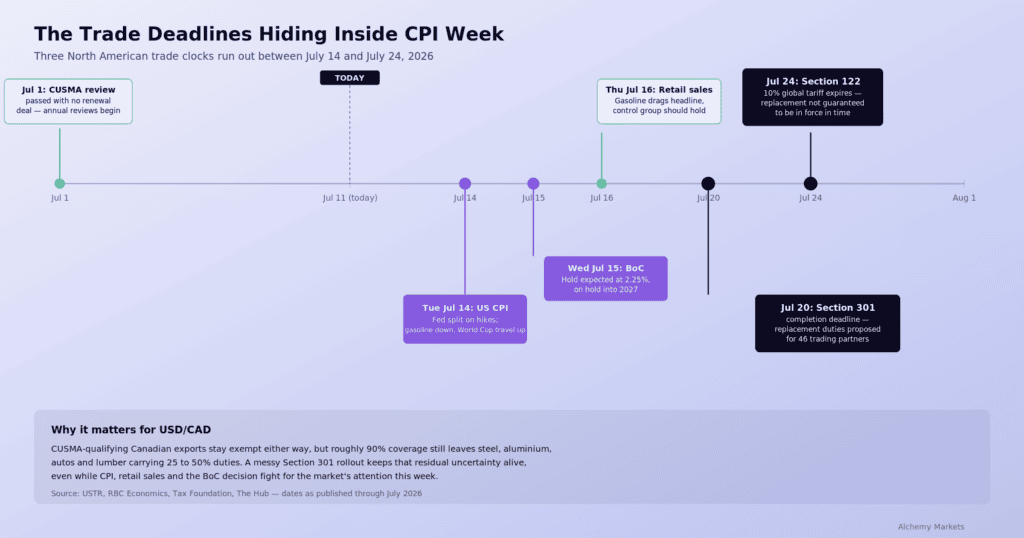

Ten days from now, on July 24, the temporary 10% tariff the US placed on most global imports is due to expire. Before that, on July 20, Washington is supposed to finish deciding what replaces it. Neither date has anything to do with interest rates. Both could still move the dollar.

Canada already got a preview of how this plays out. Its trade deal with the US came up for review on July 1 and nothing was renewed. Not cancelled, not extended, just left hanging in an annual review process that now runs for a decade. The market barely blinked, because roughly 90% of Canadian exports still cross the border tariff-free under the existing rules of origin. But steel, aluminium, autos and lumber are carrying duties of 25 to 50%, and that carve-out is precisely the kind of detail a rushed Section 301 rollout could reopen. Nothing has to go wrong for this to matter. It just has to stay unresolved while the market is busy pricing something else.

That’s the setup heading into a week that already has plenty on the calendar without it.

The Economic Calendar

United States

- Inflation (Tuesday): Should ease some of the market’s concern about the Fed hiking this year. Policymakers were split down the middle in their June projections on whether a hike is likely, but a sharp fall in gasoline prices points to a softer month-on-month CPI print. Core inflation may get a small lift from World Cup-related price hikes in hotels, travel and hospitality, but that looks temporary. From autumn onward, slowing housing rents, weaker wage growth and a fading tariff impulse should keep the disinflation story intact, and our base case is the Fed holds rates for the next 12 months.

- Retail sales (Thursday): Held back by lower gasoline prices, which mechanically depress the headline sales figure, but the control group should hold up fine. Consumer confidence should also see some recovery given the relief that cheaper fuel brings to household spending power.

Canada

- Rate decision (Wednesday): The Bank of Canada looks set to hold at 2.25%. Mixed jobs numbers, subdued business surveys, ongoing trade uncertainty and fairly benign inflation pressures all point the same way. We expect the BoC on hold well into 2027.

USD/CAD Technical Picture

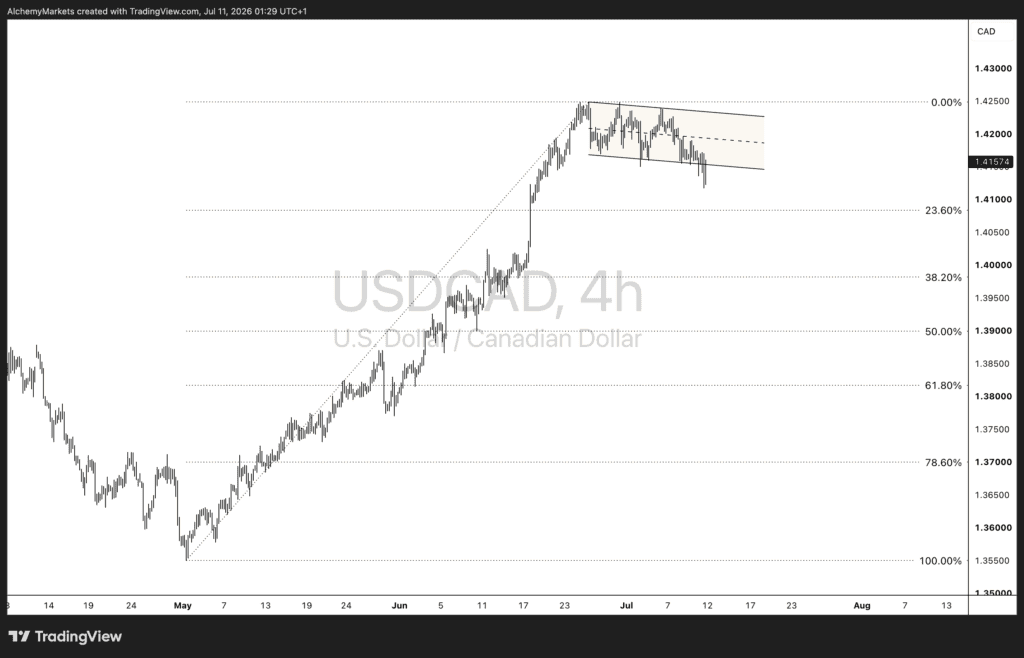

Since the May rally took USD/CAD from the low-1.35s to a high near 1.4250, price has spent the last few weeks doing something more interesting than a straight reversal. It’s consolidating inside a well-defined bull flag, orderly and compact rather than the messy churn you’d expect if the rally were simply exhausted.

That compactness matters. A tight, controlled pullback after a strong impulse move is typically corrective, not the start of a new trend, and this one has stayed inside its channel with no violent breaks either side.

Even so, we think there’s more room to give here. A retracement of at least 38.2% of the May rally would bring price down toward the 1.3990 to 1.4000 area, and given how the pair has been grinding lower within the flag rather than snapping back, that level looks like a reasonable target before buyers reassert control.