Written by:

- Opening Bell

- May 28, 2026

- 4 min read

Oil’s Bluff: Why Brent Won’t Rally on War

There is one story this morning, and it is not the inflation print. It is oil — and more precisely, it is the gap between what the overnight headlines say should be happening to crude and what crude is actually doing.

The narrative screams escalation. US forces struck Iranian targets near the Strait of Hormuz overnight, and Iran’s Revolutionary Guard said it hit a US airbase at around 4:50am local time — the latest exchange in a conflict now roughly three months old, one that has kept a fifth of the world’s seaborne oil hostage to a single chokepoint. On a fresh airbase strike, the reflex trade is simple: buy crude, sell the oil-tax victims, brace for a risk premium spike.

Then you look at the chart, and the chart disagrees.

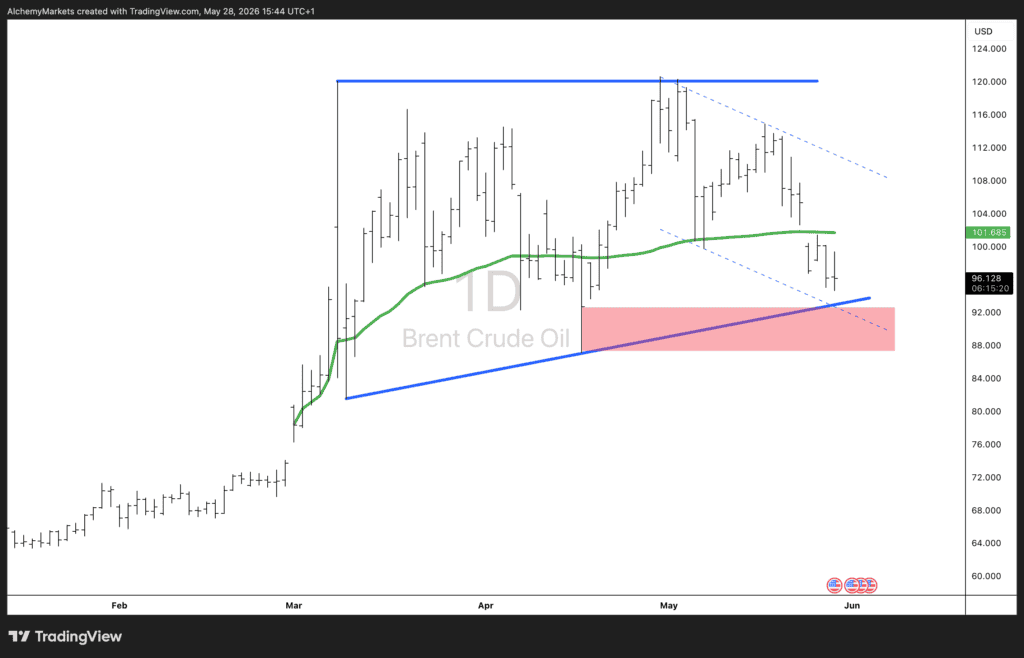

Brent crude: below the war-anchored average, and refusing to rally

The green line is the volume-weighted average price anchored to February 28 — the day the war began. It sits at $101.69. Brent is trading $96.79, below it.

That single relationship is the most important thing on the screen. Every barrel bought, on average, since this conflict started is now underwater — and an overnight escalation headline could not even lift price back to that average, let alone above it. The structure underneath confirms the message: $120 has been rejected twice at the war-spike highs, price is carving a clean series of lower highs inside a descending channel, and it is now pressing into the support cluster where the rising trendline meets the $88–93 demand zone.

This is the textbook “bad news, no rally” tell. When a market cannot rally on news tailor-made to send it higher, the risk premium is being sold, not bought. The fear is bleeding out of crude even as the headlines get louder.

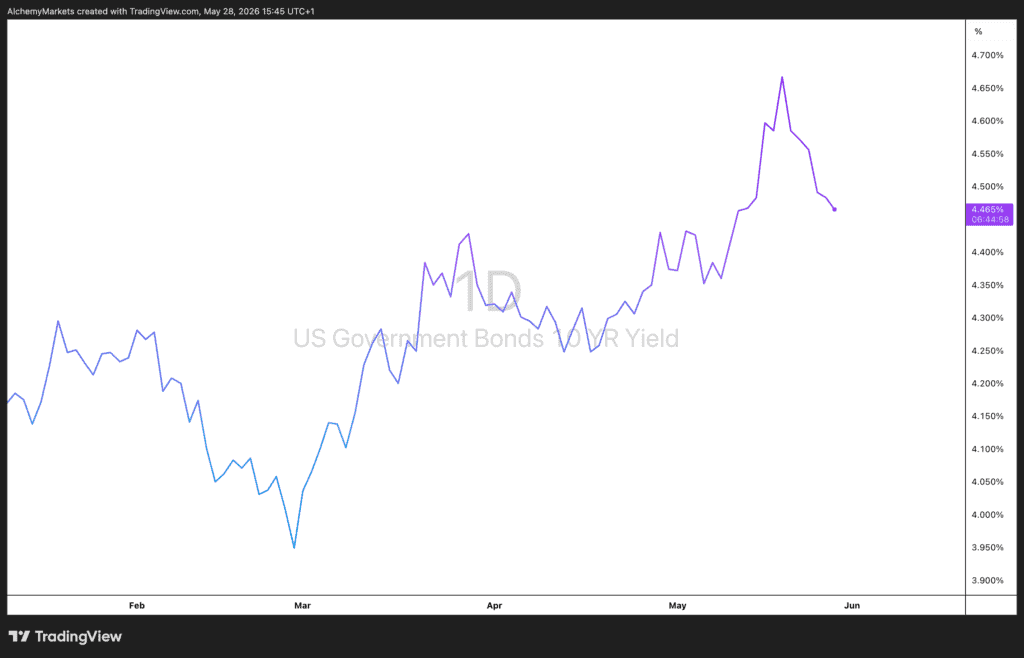

The 10-year yield: the bond market votes the same way

The second chart says the same thing in a different language. The 10-year yield spiked to roughly 4.66% in mid-May — the high-water mark of the market’s stagflation fear, the moment it most worried about an energy-driven inflation shock running into a hawkish new Fed chair. It has since backed off to 4.46%, quietly handing back about 20 basis points of that premium.

That is not a market bracing for a rate hike. That is a market exhaling.

The data fits the price action — for once

This morning’s releases line up cleanly behind the charts rather than against them. Core PCE rose just 0.2% on the month, undershooting the 0.3% estimate — the soft underlying read the doves needed. Headline PCE did hit 3.8% year over year, the highest since May 2023, but that is an energy story sitting on top of a cooling core, not evidence of broad reacceleration. And first-quarter GDP was revised down to 1.6% from the initial 2.0%, reinforcing the growth-is-cooling side of the ledger.

Soft core, softer growth, a hot-but-energy-driven headline — and two markets, crude and Treasuries, both choosing to look through the energy spike toward the benign read. The price action and the data are pointing the same direction this morning, which does not happen every day.

The frame for the open

The de-escalation, the-Fed-can-look-through read is winning at the margin. But it is one headline away from flipping, which is exactly why this is a levels trade, not a news trade. The lines that matter:

- Brent reclaims $101.69 (the war AVWAP). The risk premium is re-expanding, escalation is being priced, and the oil-tax victims — airlines, consumer discretionary — become live shorts while energy longs start to work. Until that line breaks, the chart is gating you out of the escalation trade.

- Brent breaks the $88–93 support cluster. The deal premium wins, oil-tax relief flows through, and the book inverts toward risk-on.

- Right now, Brent is mid-structure, below the AVWAP, inside the channel — leaning lower, not committed. No trade here. Wait for a line to break.

- On the 10-year, mirror it: a push back toward 4.66% says the inflation-and-hike scare is back on; holding below keeps the soft-landing read intact.

This is a binary-headline catalyst — negotiations and military action, not a scheduled data release. Clean chain, poor tradability. Do not front-run the wire. Let Brent’s relationship to the war-anchored average be the confirmation, and right now that relationship is telling you, plainly, that the market does not believe the escalation.

Into the close

The afternoon brings EIA crude inventories — a genuine oil-vol input given everything above — and Costco reports after the bell. That print is the more durable signal: a clean read on how a consumer facing 3.8% headline inflation and an energy squeeze is actually behaving. Worth more of your attention than the next Hormuz headline.