Written by:

- Opening Bell

- July 15, 2026

- 5 min read

DXY: Producer Prices Went Negative and the Core Went Up

The print inside the print

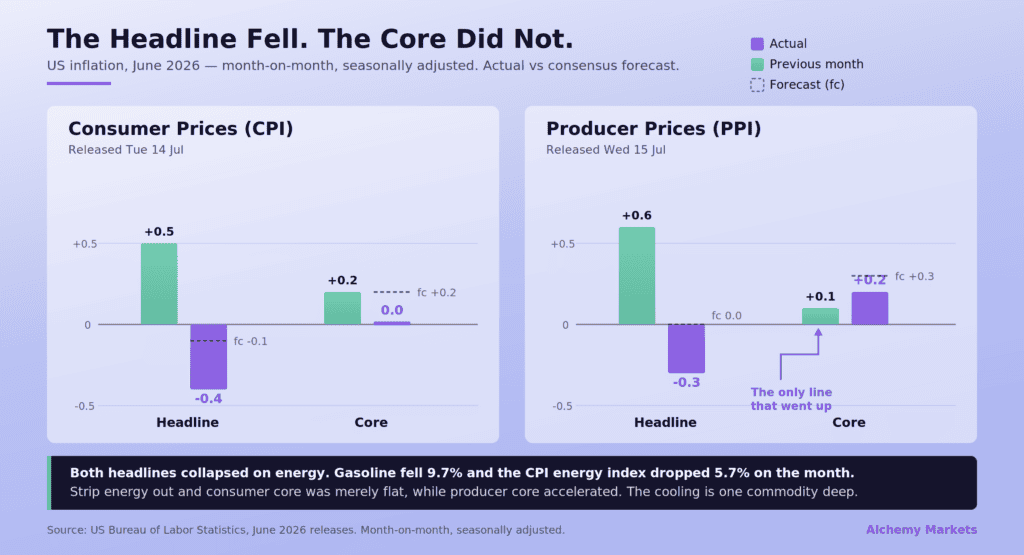

Producer prices fell 0.3% in June against expectations of no change at all, down from a 0.6% rise the month before. That is a negative headline on a series that was running hot as recently as May, and on the surface it is the second soft inflation reading in two days.

Look one line down and the picture changes. Core PPI, which strips out food and energy, rose 0.2%. That missed the 0.3% forecast, so the algorithms read it as soft. But it was 0.1% last month. Core producer inflation did not cool in June. It accelerated.

That single line is the most important number of the week, and almost nobody will lead with it.

Here is why it matters. Yesterday’s CPI was soft everywhere, and the reason was energy. Consumer prices fell 0.4% on the month against a 0.1% expected drop, the largest monthly decline since April 2020, taking the annual rate to 3.5% from 4.2%. Core was flat, easing to 2.6% from 2.9%. But the entire move traced to a 5.7% drop in energy and a 9.7% fall in gasoline, which more than offset increases everywhere else. Shelter still rose. Food still rose.

The obvious question after a print like that is whether the disinflation is real or whether it is one commodity doing all the work. Producer prices sit upstream of consumer prices, which makes today’s report the natural test. If cost pressure were genuinely easing through the chain, core PPI is where you would see it first.

Core PPI went the other way.

So the two reports do not corroborate each other. They repeat each other. Both headlines collapsed for the same reason, and in both cases the underlying measure told a different story than the headline did. Consumer core was flat because of what was excluded from it. Producer core, with the same exclusions, actually firmed.

This is why the dollar refused to break yesterday, and it is why Chair Warsh was so blunt in testimony an hour after CPI landed. His line was that the data does not tell him mission accomplished, that it is one data point, and that he has no interest in cherry-picking it. Goolsbee added that several months of readings like this would be needed before it felt like progress. At the time that looked like a Chair defending a hawkish stance against inconvenient data. This morning it looks like a Chair who had read the composition properly.

And the energy relief that produced both headlines is already reversing. It traces back to the ceasefire and the reopening of the Strait of Hormuz, and that ceasefire has collapsed. Strikes have restarted, the blockade is back on, crude is bid again. The input that made June look benign is unwinding while we speak. July’s prints get built on a rising energy base with a core that was firming before the base even turned.

None of which means the dollar cannot fall. July hike odds genuinely came down this week, and that repricing is real. But the case for a sustained leg lower rested on the idea that the cooling was broad, and this morning’s core reading is the first hard evidence that it is not.

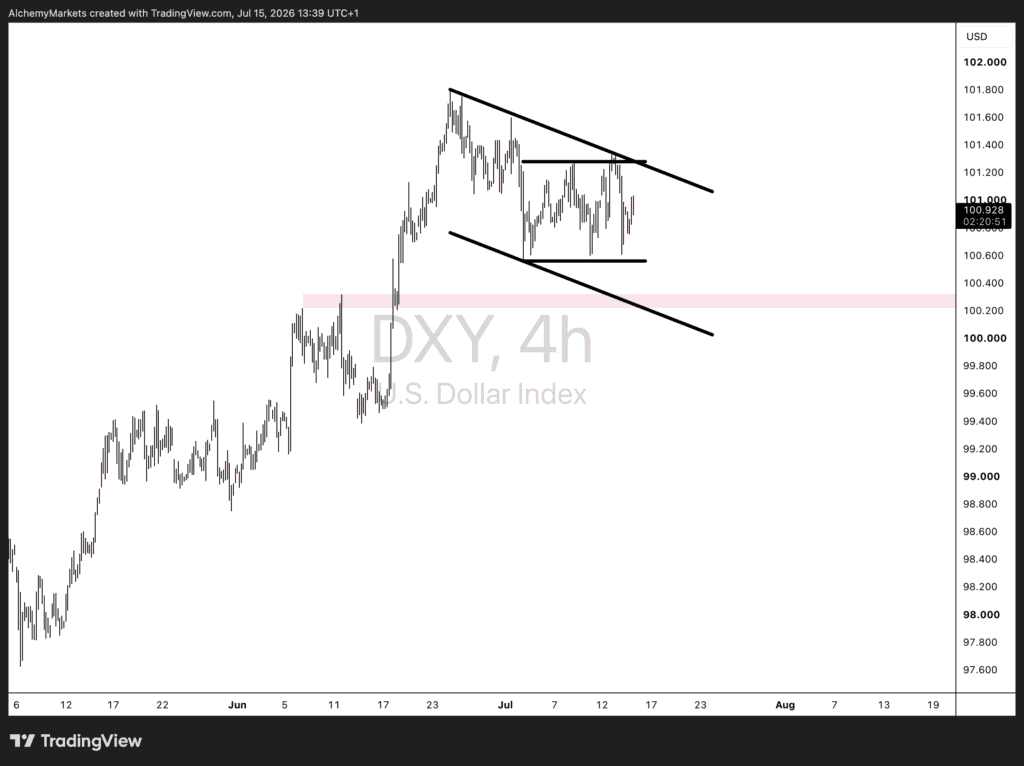

Dollar Index – 4 hour

DXY is inside a descending channel and running out of room to be undecided.

The structure begins with the early-July expansion, which took price vertically out of the 99.50 region up to just under 101.90 on the Iran escalation and Waller’s comments about a hike being on the table. Since that high, price has rolled over into a clean descending channel, with the upper boundary catching every rally attempt since.

Inside the channel sits a tighter range, roughly 101.30 on the ceiling and 100.60 on the floor. Price is at 100.988, near the middle of the box, and that box has now held two weeks of trade. Note the character. The advance was vertical and clean. The correction has been choppy and overlapping, taking three times as long to retrace a third of the distance. That relationship reads as correction rather than reversal, which is why downside needs a specific trigger rather than a narrative.

The 100.60 floor is that trigger. Price tested it on the CPI wick yesterday and it held on a closing basis, which is where the defence has shown itself. A four-hour close beneath it, not a wick, turns the shelf from support into resistance and opens the path toward 100.30. That level is worth more than a round number because two structures meet there. The lower boundary of the descending channel converges with a horizontal zone that price respected on the way up in mid-June, and confluence of that kind is what tends to stop a move rather than let it run.

Above, the channel’s upper boundary and the 101.30 ceiling have now compressed almost on top of each other, the tightest resistance has been all month. Price failed there on the twelfth. A sustained break through that confluence is what would invalidate the corrective read entirely.

Two soft headlines, a firming core, and a market sitting mid-channel. The edges decide this, and they are closer than they were on Monday.