Written by:

- Opening Bell

- March 11, 2026

- 5 min read

CPI in Line; EUR/USD Eyes Inverse H&S Break

U.S. inflation cooled modestly in the latest CPI report, reinforcing the view that price pressures are gradually moving closer to the Federal Reserve’s target.

Headline Consumer Price Index rose 0.3% month-over-month and 2.4% year-over-year, broadly matching expectations. Core CPI, which excludes food and energy, increased 0.2% on the month and 2.5% on the year, slightly softer on the monthly reading.

The data suggests the disinflation trend remains intact. Inflation has not fully returned to the Fed’s 2% objective, but the trajectory continues to move in that direction.

Importantly, the report reflects inflation conditions before the recent geopolitical oil shock, meaning potential energy-driven inflation risks may appear in future prints if oil prices remain elevated.

For now, however, the overall message from the data is straightforward: inflation pressures continue to ease gradually.

What Drove the CPI Print

Energy prices were the main contributor to the rise in headline inflation.

Higher fuel costs helped push the monthly headline reading to 0.3%, though the increase was largely expected given recent moves in energy markets.

Core inflation, which policymakers watch more closely, remained contained.

Several components helped keep the core reading relatively subdued:

- Goods inflation continued to cool

- Used vehicle prices declined

- Supply chain pressures remain largely normalized

The most persistent component remains shelter inflation, which continues to run above pre-pandemic levels. However, the pace of shelter price increases is gradually moderating, consistent with softer housing market conditions.

Overall, the composition of the report suggests that underlying inflation pressures continue to ease, even if progress remains gradual.

Implications for the Federal Reserve

For the Federal Reserve, the report does little to change the broader policy outlook.

With headline inflation at 2.4% and core at 2.5%, price growth is now approaching levels broadly consistent with the Fed’s target.

However, policymakers are likely to remain cautious. The central bank has repeatedly emphasized the need for sustained evidence of disinflation before shifting policy.

The Fed will continue to watch two areas closely:

- Core services inflation

- Labour market conditions

If inflation continues to trend lower and the labour market gradually cools, the Fed could begin moving toward policy easing later this year.

For now, the data supports the view that inflation is moving in the right direction, even if the final stretch toward the 2% target may take time.

Market Implications

Cooling inflation generally supports financial markets by easing pressure on interest rates.

Lower inflation tends to translate into:

- Lower real yields

- Easier financial conditions

- Improved risk sentiment

That combination typically supports equities and other risk assets.

The main uncertainty remains energy prices. The current CPI report largely captures inflation conditions before the recent rise in oil prices, leaving open the possibility that future prints could see temporary energy-driven increases.

For now, markets appear to view any oil-driven inflation spike as potentially temporary rather than structural.

Forward Inflation Expectations

Markets tend to focus less on past inflation data and more on where inflation is heading.

The key question for investors is whether inflation will continue moving toward the Fed’s 2% target.

If confidence in the disinflation trend strengthens, expectations for future policy easing could increase, which typically supports risk assets and eases financial conditions.

In that sense, the macro debate has shifted from whether inflation has peaked to how quickly it will normalize.

FX Focus – EUR/USD

Foreign exchange markets are particularly sensitive to shifts in inflation expectations and interest rate outlooks.

If inflation continues to moderate and the Fed moves closer to easing policy, U.S. real yields could stabilize or decline, which would typically weigh on the dollar.

A softer dollar environment could provide support for currencies such as the euro, particularly if interest rate differentials begin to narrow.

Technical Setup – EUR/USD

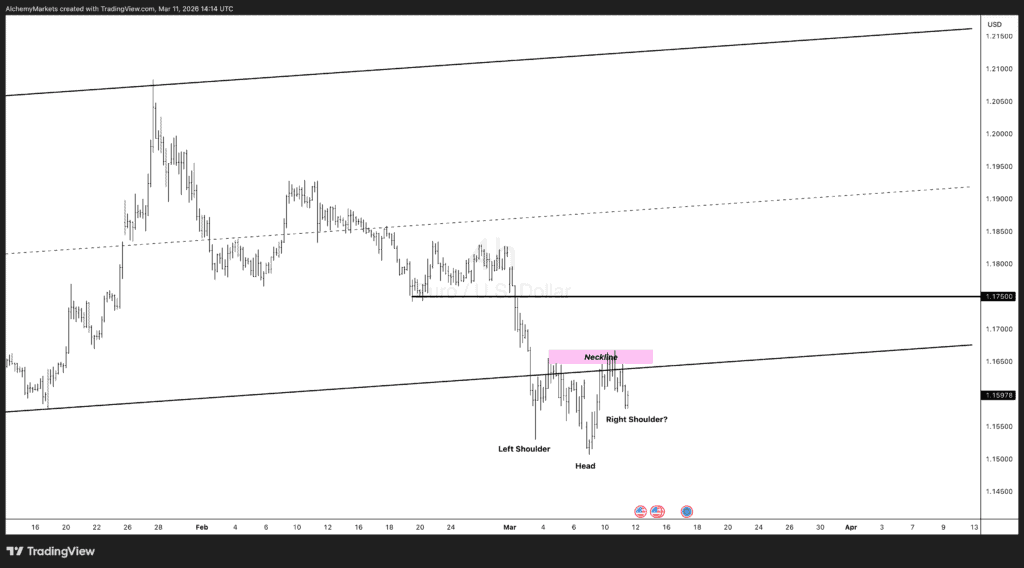

From a technical perspective, EUR/USD appears to be forming an inverse head-and-shoulders pattern, a classic bullish reversal structure.

The left shoulder formed in early March, followed by the head near the recent lows around 1.150. Price action now appears to be forming the right shoulder.

The key level to watch is the neckline near 1.165.

A break above this level would confirm the pattern and could signal a broader shift in momentum.

If that breakout occurs, the next upside level traders are watching sits near 1.175, which marks the next key resistance zone.

Such a move could align with U.S. dollar weakness if markets grow more confident that inflation remains under control and the Fed is moving closer to eventual policy easing.

Bottom Line

The latest CPI report reinforces the broader disinflation narrative.

Inflation continues to trend lower, with both headline and core readings now approaching levels consistent with the Federal Reserve’s target. While policymakers are likely to remain cautious, the data keeps the door open for policy easing later this year if the trend continues.

For markets, the focus remains on forward inflation expectations and the path of interest rates.

If disinflation holds and rate expectations begin to shift, the dollar could weaken, opening the door for EUR/USD to move toward 1.175, particularly if the inverse head-and-shoulders breakout above 1.165 confirms.