Written by:

- Opening Bell

- April 23, 2026

- 5 min read

Europe Slides Into Stagflation Risk as DAX Nears Critical 23,000–23,250 Inflection Zone

European markets are opening on a more fragile footing today as the latest PMI data challenges the prevailing soft-landing narrative and introduces a more complex macro picture — one where growth is slowing, but inflation refuses to cooperate.

The April flash print showed the Eurozone composite PMI slipping into contraction at 48.6, marking the first sub-50 reading in over a year. That alone would be enough to raise eyebrows — but the real signal lies beneath the surface.

This isn’t just a slowdown. It’s a shift in the structure of growth.

The Signal Beneath the Headline

What stands out most is the composition of the decline.

Services — the engine that has carried Europe’s post-pandemic recovery — weakened sharply, falling to a multi-year low. That’s a key warning sign. When services roll over, it typically reflects softness in the consumer, not just external demand.

At the same time, manufacturing surprised slightly to the upside. But this isn’t clean strength. It looks increasingly like inventory-driven activity, likely tied to supply chain uncertainty and geopolitical risk rather than genuine demand recovery.

In simple terms, what we’re seeing is distortion — not durability.

The Bigger Problem: Growth Down, Inflation Up

If this were just a growth slowdown, markets could lean on central bank support. But the complication — and the real risk — is inflation.

Input costs surged again in the latest data, driven by energy and ongoing supply disruptions. More importantly, companies are still passing those costs through. Output prices are now rising at the fastest pace in over three years.

That combination creates a classic stagflationary setup:

- Demand is weakening

- Costs are rising

- Pricing pressure persists

This is precisely the environment central banks struggle with.

The European Central Bank now faces a difficult trade-off:

- Cutting rates risks reigniting inflation

- Holding or tightening policy risks amplifying the slowdown

The most likely outcome, at least near term, is policy staying restrictive by necessity, not choice.

What the Market Actually Cares About

Markets are less concerned with the PMI level itself and more with what it means for expectations.

Up until now, positioning has leaned toward:

- Gradual stabilisation

- Mild recovery into the second half of the year

This data challenges that narrative.

We’re now looking at a more asymmetric risk profile:

- Growth is slowing faster than expected

- Inflation is proving stickier than expected

That combination increases the likelihood of earnings downgrades without policy support — a difficult backdrop for risk assets.

Equities — Pressure Building Under the Surface

For European equities, this is not an ideal setup — especially for cyclicals.

The environment is shaping into a margin squeeze scenario:

- Demand softens (particularly in services)

- Input costs remain elevated

- Pricing power becomes more difficult to sustain over time

Even before volumes deteriorate meaningfully, profitability comes under pressure.

Near term, indices may appear resilient — but the underlying conditions are weakening.

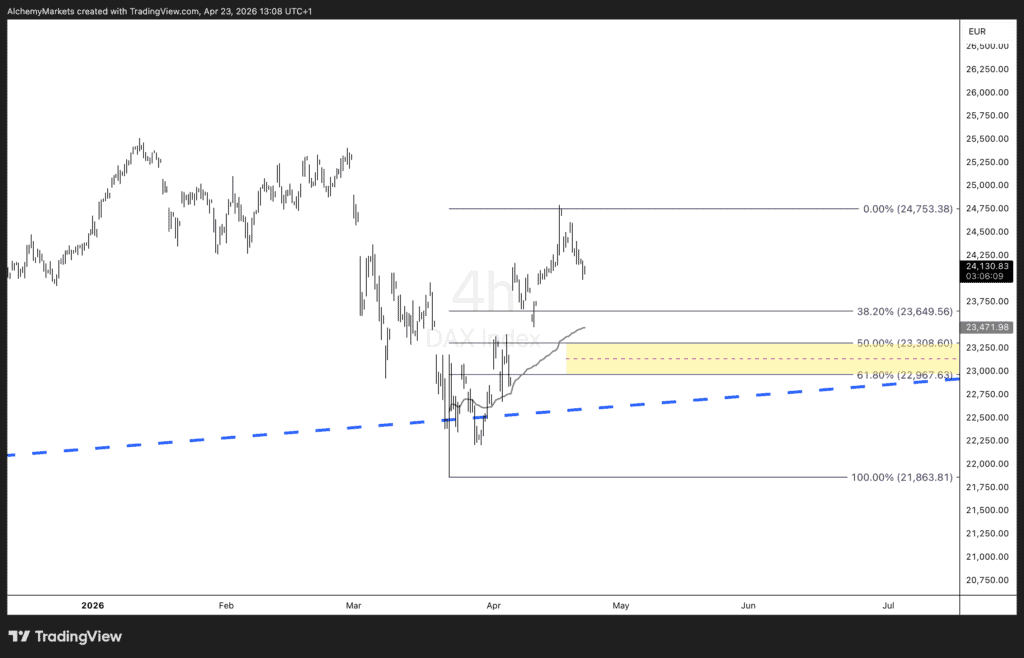

Technical Focus — DAX Approaching Key Inflection Zone

From a tactical perspective, the DAX is approaching a critical area that could define near-term direction.

The index is likely to gravitate toward the 50%–61.8% Fibonacci retracement zone, which comes in between 23,000 and 23,250.

This zone matters for several reasons:

- It represents a natural retracement level after the prior move higher

- It aligns closely with the anchored VWAP from the March 20th lows

- It is a region where positioning tends to shift from momentum-driven buying to more selective participation

In practical terms, this creates a potential near-term magnet for price, but also a decision point.

If price reaches this zone:

- A failure to hold could signal exhaustion and the start of a broader repricing

- Acceptance above it would require improving macro confirmation, which currently looks uncertain

Given the macro backdrop, the balance of risks leans toward this zone acting as support rather than a breakout catalyst, at least initially.

The Real Shift — Expectations vs Reality

What makes this environment particularly interesting is timing.

We are likely entering an early-to-mid expectation adjustment phase:

- The data is beginning to turn

- But positioning and estimates haven’t fully caught up

That gap is where opportunity tends to emerge.

Key signals to watch over the coming sessions:

- Does soft data continue to deteriorate?

- Do equities start underperforming even on positive headlines?

- Do analysts begin revising earnings expectations lower?

If those dynamics start to align, this PMI print won’t be dismissed as noise — it will mark the start of a broader narrative shift.

Bottom Line

Europe isn’t just slowing — it’s slowing in a more problematic way.

With growth rolling over and inflation still elevated, the macro backdrop is becoming increasingly complex. Markets now have to price not just weaker activity, but the risk that policy remains restrictive into that weakness.

That’s not a collapse scenario.

But it is an environment where expectations may still be too optimistic — and where the surface resilience in equities could begin to give way to underlying pressure.