Skriven av:

- Weekly Outlook

- maj 1, 2026

- 7 min läsning

Fed Uncertainty, Inflation Risks, and the Week Ahead

Financial markets are entering a more complex phase. What once seemed like a clear path toward rate cuts has shifted into something far less predictable. Central banks—especially in the United States—are no longer guiding markets toward easing with confidence. Instead, policymakers are signaling caution, flexibility, and a growing sensitivity to incoming data.

This evolving backdrop is critical for investors. It’s no longer just about what central banks will do—it’s about how expectations are changing, and where markets may still be misaligned with reality.

The Federal Reserve: From Clarity to Caution

The Federal Reserve is currently holding interest rates steady in the 3.50%–3.75% range. While this pause has been consistent across recent meetings, the tone behind it has shifted meaningfully.

Previously, markets interpreted the Fed’s stance as a temporary pause before eventual rate cuts. Now, policymakers are emphasizing uncertainty. Some officials have openly acknowledged that the next move could be either a hike or a cut, depending entirely on how economic data evolves.

This shift reflects a broader change in thinking. Rather than guiding markets toward a specific outcome, the Fed is positioning itself to react. That introduces a two-sided risk environment—something markets haven’t had to price in for quite some time.

Why the Narrative Has Changed

Two main forces are driving this shift in central bank messaging.

1. Inflation Risks Are Re-Emerging

Energy prices have become a renewed source of concern. Geopolitical tensions—particularly in the Middle East—have increased the risk of supply disruptions, pushing oil prices higher. This feeds directly into inflation, especially through fuel and transportation costs.

There is now a credible risk that inflation could stabilize above target levels, rather than continuing its decline. This complicates the case for rate cuts and forces policymakers to remain cautious.

2. Economic Growth Remains Resilient

Despite higher interest rates, the broader economy has not weakened enough to justify immediate easing. Labor markets, while showing some signs of cooling, are not deteriorating sharply.

This resilience limits the urgency for the Fed to act. If growth remains intact and inflation risks persist, policymakers have little incentive to cut rates prematurely.

Market Expectations: A Reset in Progress

Markets have already begun adjusting to this new reality.

Earlier in 2026, investors widely expected a series of rate cuts beginning mid-year. That view has now been largely abandoned. Current pricing suggests interest rates are likely to remain steady for an extended period, with only a small chance of a single cut.

More notably, there is now a growing probability that rates could even move higher again in the future. This represents a significant shift from the previous consensus.

What’s happening is not just a reaction to current conditions—it’s a recalibration of expectations.

Why This Transition Matters

Markets tend to move most when expectations change, not when events occur as predicted. Right now, we are in the middle of such a transition.

The idea of “higher for longer” is becoming more accepted, but it is not yet fully embedded in asset prices. This creates a period of adjustment where volatility can increase, and different sectors react in varying ways.

Several key implications emerge from this environment:

- Valuation pressure remains: Higher interest rates reduce the present value of future earnings, weighing on growth-oriented and high-multiple sectors.

- Inflation sensitivity increases: Industries tied to energy costs or consumer spending may experience more pronounced swings.

- Market reactions become more data-driven: Each economic release has the potential to shift expectations meaningfully.

In short, the market is moving from a one-directional outlook to a more balanced—and uncertain—framework.

The Real Catalysts Now

With central bank meetings largely priced in, attention shifts to incoming data and external factors that can influence policy expectations.

Inflation Data

Consumer price and personal consumption expenditure figures will play a central role. Stronger-than-expected readings could push markets toward pricing in rate hikes, while softer data may revive the case for cuts.

Energy Prices

Oil remains a critical variable. Sustained high prices could reinforce inflation concerns, while a decline would ease pressure on both consumers and policymakers.

Labor Market Trends

Employment data will help determine whether the economy is slowing enough to justify policy easing. A weakening labor market could shift expectations quickly.

Central Bank Communication

Even subtle changes in tone—such as removing references to potential rate cuts—can have an outsized impact on market sentiment.

Week Ahead: Key Economic Events

Looking ahead, next week’s economic calendar provides several important data points that could influence market direction.

United States

Non-Farm Payrolls (Friday)

The labor market remains one of the most closely watched indicators.

Recent trends show a sharp slowdown in job creation, with average monthly gains of just 20,000 since early 2025. This suggests that even during periods of stronger economic growth, hiring momentum has been limited.

Given the current backdrop—marked by geopolitical tensions and economic uncertainty—expectations are modest. A gain of around 50,000 jobs for April appears plausible, with hiring likely concentrated in sectors such as education and healthcare.

However, the picture is mixed. While some indicators, like employment indices and layoff announcements, point to weakness, others—such as jobless claims—remain relatively stable. This divergence increases the importance of the official payrolls figure.

A significant deviation from expectations could quickly alter market sentiment.

ISM Services Index (Tuesday)

The services sector has been a key pillar of economic strength, but signs of softening may emerge.

Rising energy costs are beginning to weigh on business activity and consumer demand. As gasoline prices climb, households may become more cautious with spending, potentially impacting service-related industries.

A modest decline in the ISM services index would reinforce the view that economic momentum is gradually slowing.

Consumer Sentiment

Consumer confidence is another area to watch closely. Higher fuel costs and concerns about purchasing power are likely to dampen sentiment.

There is a possibility that confidence measures could approach new lows, reflecting increased anxiety about financial conditions and job prospects.

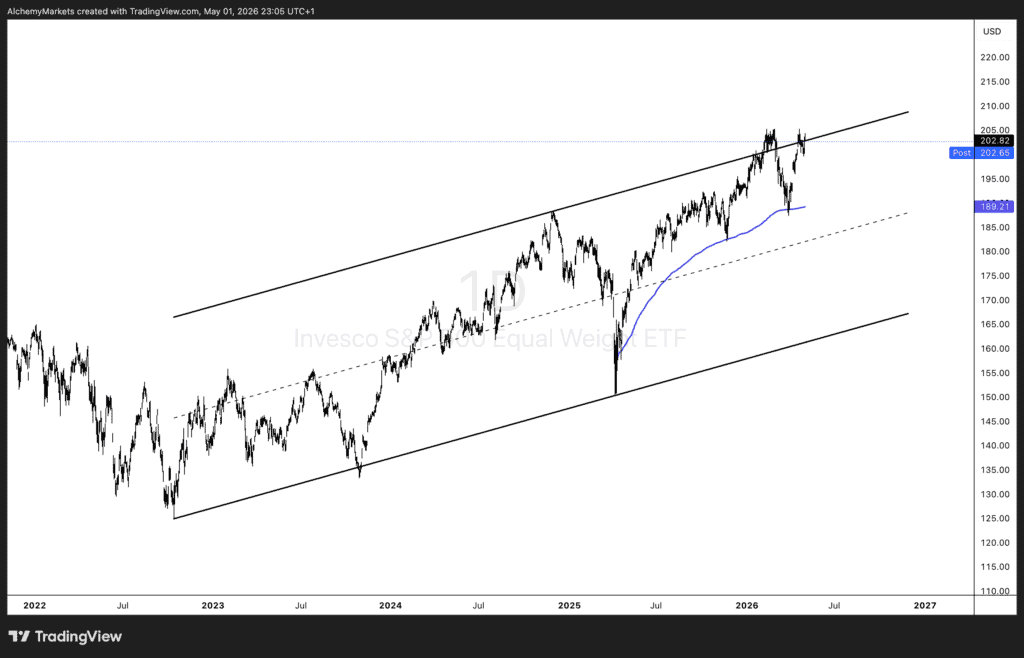

Technical Analysis: RSP (Equal Weight S&P 500 ETF)

From a technical perspective, the equal-weighted S&P 500 ETF (RSP) offers useful insight into broader market behavior beyond mega-cap stocks.

Currently, the ETF is trading near the upper boundary of an ascending channel, around the $202 level. This area has acted as resistance, suggesting that upward momentum may be limited in the near term.

If the price fails to break above this level convincingly, a pullback becomes increasingly likely. In such a scenario, the next key support zone sits around $190.

This level represents a potential minimum downside target within the current channel structure. A move toward this area would align with a broader consolidation phase, particularly if macroeconomic data introduces additional uncertainty.

For now, price action suggests the market is testing its upper limits, with risk skewed toward a near-term correction rather than continued acceleration.

Final Thoughts

Markets are navigating a transition period defined by shifting expectations and increased uncertainty. The Federal Reserve is no longer guiding toward a clear outcome, and investors are adjusting accordingly.

This environment demands a different approach. Rather than focusing solely on central bank decisions, attention must shift to the data and external factors that shape those decisions.

As the week ahead unfolds, economic releases—particularly in the United States—will play a critical role in determining the next phase of market direction.

In times like these, understanding not just what is happening, but how expectations are evolving, becomes the true edge.