CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. Most retail clients lose money when trading CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Oil Shock, Central Bank Friction & AI Earnings Resilience

Oil, USD Strength and Fragile Risk Sentiment

Markets head into the session caught between geopolitical-driven oil strength and resilient US growth signals, creating a clear divergence across asset classes. Crude continues to push higher on Middle East tensions, while equities—particularly outside the US—are showing signs of strain.

At the same time, the US dollar is firming, not purely on rates, but increasingly on risk dynamics and relative macro resilience. This is a key shift. Historically, oil spikes could weigh on the dollar, but in the current regime, the relationship has flipped.

USD: Oil Rally Now USD-Supportive

The Fed delivered what markets expected on the surface—but the details matter. The 8–4 vote split, with dissent both for and against easing bias, introduces policy uncertainty rather than clarity. This complicates any near-term dovish pivot narrative.

More importantly, the macro backdrop is doing the heavy lifting for the dollar.

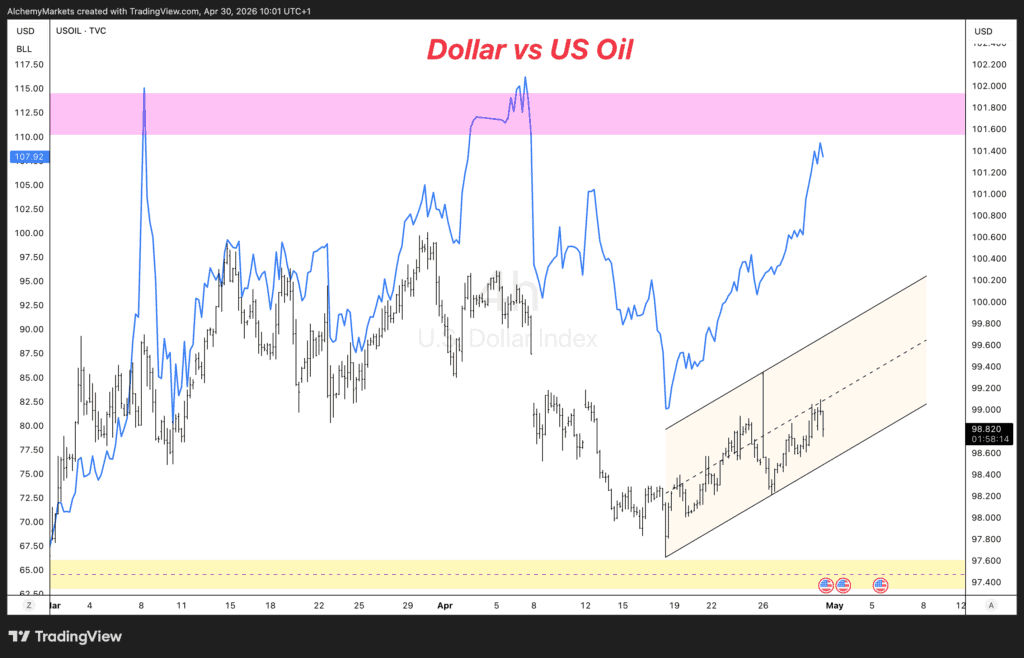

The chart below highlights the evolving relationship:

Oil (blue) continues to surge

DXY (candles) is lagging—but catching up

Chart Insight – Dollar vs Oil

DXY lagging the oil rally, but increasingly at risk of catching up higher as geopolitical risk drives safe-haven demand.

Key drivers:

Geopolitical premium in oil → USD bid (safe haven)

Eurozone vulnerability to energy shocks

Equity market fragility reinforcing USD demand

This is not a demand-driven oil rally—it’s a risk-driven shock, and that distinction is critical. As long as that holds, USD upside risks remain intact, with DXY potentially gravitating back toward the 100 level.

EUR/USD: Rates Matter Less, Risk Matters More

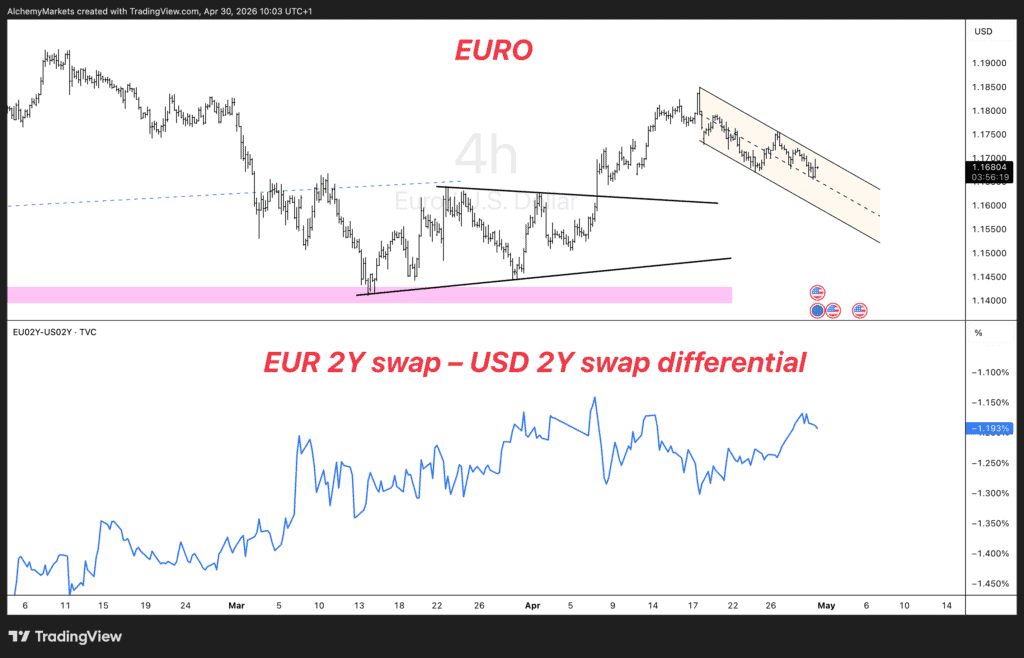

EUR/USD has become a function of global risk sentiment, rather than purely rate differentials.

While the EUR–USD 2Y swap differential has tightened, reflecting relatively more hawkish ECB expectations, the FX response has been muted.

Chart Insight – EUR/USD vs 2Y Differential

The EUR–USD 2Y rate differential has tightened, but EUR/USD is no longer fully tracking it—highlighting a breakdown in correlation.

What this tells us:

Rates still matter—but they are secondary

Equities and oil now dominate FX direction

EUR strength requires stable risk sentiment, not just ECB hawkishness

With oil rising and equities under pressure, the bar for EUR upside is high.

ECB: High Bar to Surprise

Markets are already pricing a meaningfully more hawkish ECB path, with ~80bp of tightening expected by year-end.

Because the current oil rally is driven by geopolitical risk, which boosts safe-haven demand for the dollar.

2. Does the ECB need to hike to support EUR?

Yes—but even that may not be enough unless risk sentiment improves.

3. Why isn’t EUR/USD following rate differentials anymore?

Because equities and global risk sentiment have become the dominant drivers.

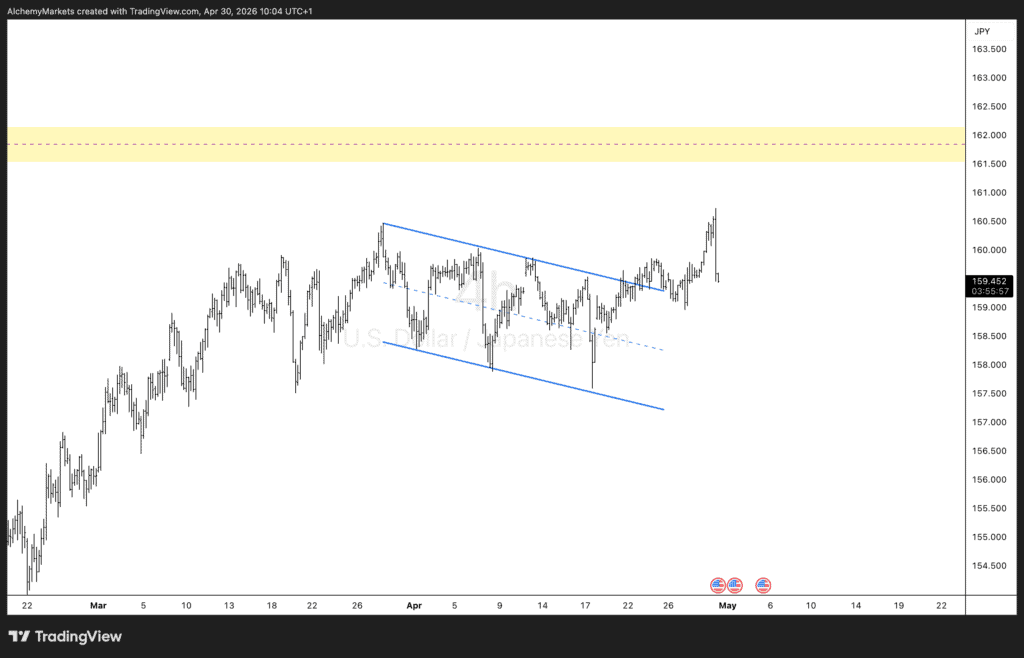

4. Is USD/JPY at intervention risk?

Yes, particularly above 162, though authorities may delay action.

5. Are tech earnings still strong?

Yes—especially in AI and cloud—but rising CapEx is the new concern.

6. What is the biggest market risk right now?

Further escalation in oil/geopolitics, which would strengthen USD and pressure risk assets.

Ansvarsfriskrivning: Endast i utbildningssyfte. Trading innebär betydande risker som kan leda till förlust av ditt kapital. Traders uppmanas att göra sin egen due diligence innan de investerar.