Scritto da:

- Opening Bell

- Giugno 17, 2026

- 5 min di lettura

Kevin Warsh’s First FOMC as Fed Chair: What Will He Say?

Kevin Warsh will lead his first FOMC decision as Federal Reserve Chair today, with markets expecting the Fed to leave rates unchanged at 3.50%-3.75%.

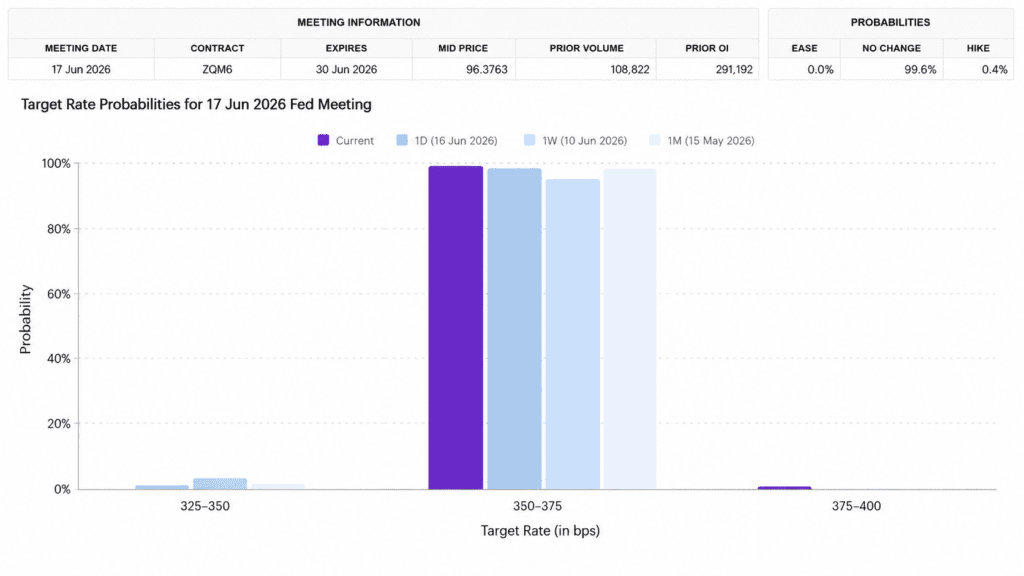

Fed funds futures currently show a 99.6% probability of a hold, a 0.4% probability of a hike, and no expected chance of a cut. Markets will focus on Warsh’s press conference, the updated dot plot and whether the Fed still sees its next move as a cut.

No Rate Change Expected Today

The current FedWatch distribution leaves little room for an immediate surprise.

Coming into Wednesday, the probability of a cut has fallen to zero. A small 0.4% hike probability has appeared instead, while almost all pricing remains concentrated on a hold.

That does not mean markets expect Warsh to raise rates today. It shows that expectations have moved away from near-term easing.

Warsh’s language will determine whether that shift continues. A firm inflation message could keep the dollar and shorter-term Treasury yields supported. A softer assessment could bring rate-cut expectations back into later meetings.

Caption: Fed funds futures assign a 99.6% probability to unchanged rates, with no cut probability and a small 0.4% chance of a hike.

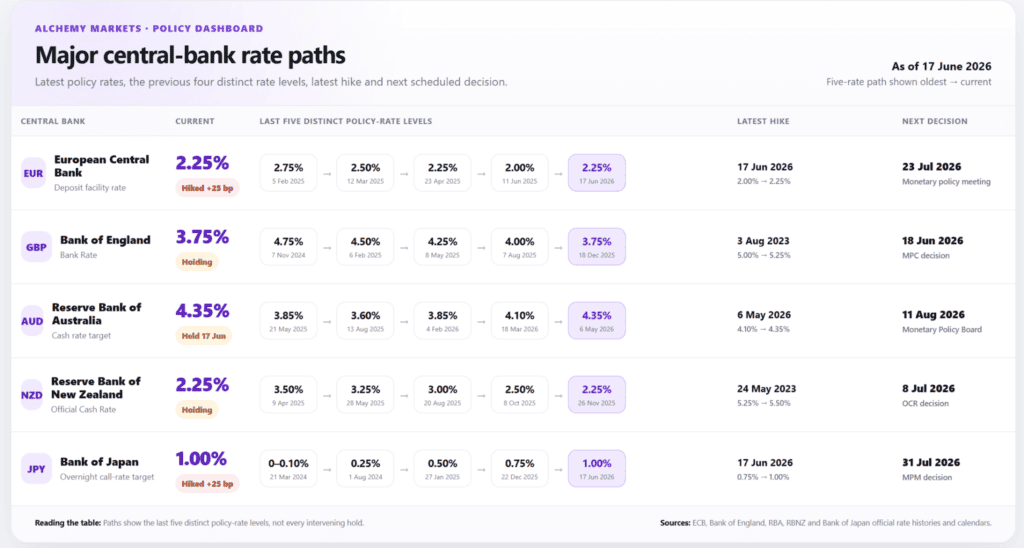

The Global Rate Cycle Has Split

The Federal Reserve is holding while several other major central banks have already moved towards tighter policy.

The European Central Bank raised its deposit rate to 2.25%. The Reserve Bank of Australia has increased its cash rate to 4.35%, while the Bank of Japan has raised its overnight rate to 1.00%.

The Bank of England remains at 3.75%, with its next decision due on 18 June. The Reserve Bank of New Zealand is holding at 2.25% after cutting rates during the previous easing cycle.

Recent hikes from the ECB, RBA and BoJ make an immediate Fed cut harder to justify.

The banks are not following identical paths, but they are responding to similar inflation risks, including higher energy costs and the possibility that those costs spread into services and wages.

Caption: The ECB, RBA and BoJ have recently raised rates, while the BoE and RBNZ remain on hold after earlier easing.

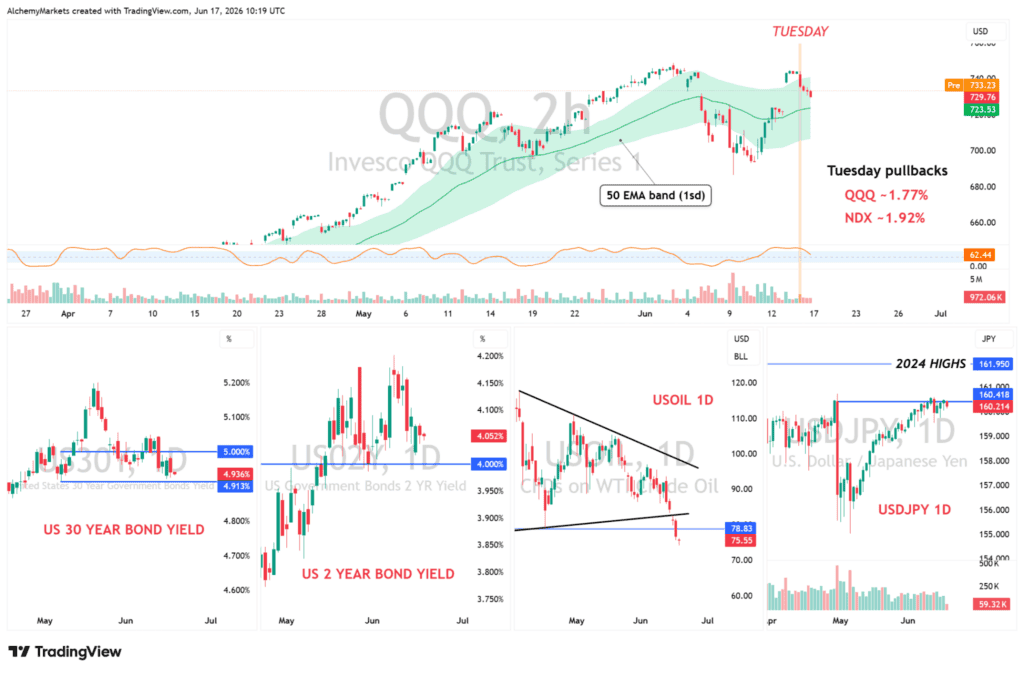

Quick Market Recap Ahead of the Decision

- QQQ fell 1.77%, while the Nasdaq 100 declined 1.92%.

- QQQ approached its two-hour 50 EMA band, which has supported several pullbacks since April.

- QQQ volume was lighter during parts of the decline.

- Oil continued to fall, reducing some immediate inflation pressure.

- US Treasury yields have eased from the beginning of the month, but the dollar remains firm.

- USDJPY stayed close to its recent highs despite the Bank of Japan’s rate hike.

Caption: Technology shares pulled back before the FOMC while oil declined, Treasury yields remained elevated and USDJPY held near its recent highs.

Tech Approaches Its Two-Hour 50 EMA

QQQ, the ETF for the Nasdaq 100, has moved back towards its two-hour 50 EMA band after Tuesday’s 1.77% decline. The area has supported several pullbacks since April, although the FOMC reaction will determine whether it holds again.

A rise in the US two-year yield after Warsh’s press conference would place more pressure on technology shares. A fall in yields would support a rebound from the EMA area.

Falling Oil Gives Warsh More Room to Hold

US oil has fallen from its recent highs and broken below its previous low at 78.83. Lower oil reduces pressure on short-term inflation expectations. But more importantly, it also lowers the immediate need for the Fed to consider another increase.

MOU Negotiations Still Remain Fragile

The geopolitical backdrop remains unsettled. Iran has said that a final agreement with the United States requires Israel to withdraw from Lebanon, while Israel has rejected that condition.

Oil could reverse higher if negotiations weaken or regional fighting increases. Warsh is therefore unlikely to treat the recent decline as a permanent reduction in inflation risk.

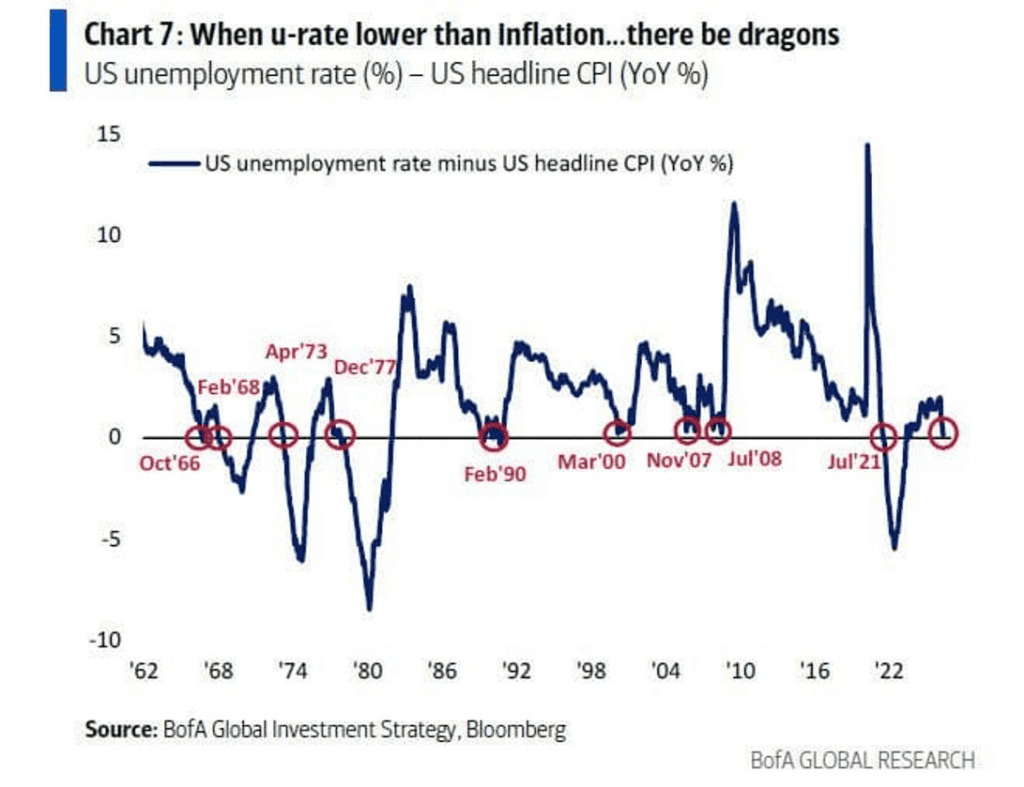

Inflation Still Limits a Dovish Shift

However, one big story everyone may be missing is that the gap between the US unemployment rate and headline inflation is close to zero. Historically, similar readings have appeared when inflation remained high relative to labour-market weakness.

Those conditions can restrict the Fed’s ability to ease policy even when growth begins to slow.

The comparison is not a direct market-timing signal. It supports a cautious policy stance from Warsh, while inflation remains above target.

Caption: The gap between US unemployment and headline inflation is close to zero, leaving the Fed with limited room to signal easier policy.

What to Watch From Warsh

- The dot plot: Whether officials still project cuts during 2026.

- Inflation: Whether lower oil changes the Fed’s assessment of price pressure.

- Policy direction: Whether Warsh describes the next move as open in both directions.

- US two-year yield: The clearest immediate signal of how markets interpret the meeting.

- DXY and USDJPY: A stronger dollar would support the higher-for-longer reading.

- QQQ: A hold above the two-hour 50 EMA would keep the recent upward structure intact.

The FOMC statement is due at 18:00 UTC on 17 June (2:00 p.m. New York time), followed by Warsh’s press conference at 18:30 UTC (2:30 p.m. New York time).

Bottom Line

The core story remains the same as it has for the past three months: the Federal Reserve is in a difficult position. It has no immediate need to raise rates, but inflation and labour-market conditions still do not provide a convincing case for cuts.