Written by:

- Weekly Outlook

- March 28, 2026

- 4 min read

S&P 500 Cannot Be Protected by Anchored VWAP — Oil Shock Drives Markets Into a Risk-Off Week

Last Week’s Market Theme: Geopolitics Over Everything

Last week, financial markets were driven by one dominant force: geopolitical tension in the Middle East leading to a surge in oil prices and renewed inflation fears.

This wasn’t a normal macro week where data like inflation or growth took center stage. Instead, markets were reacting to headline risk and supply shocks, particularly in energy. Oil prices surged aggressively, and that fed directly into concerns that inflation could reaccelerate just as central banks were hoping it would cool.

That shift caused a clear “risk-off” move:

- Equities sold off sharply

- Volatility increased across assets

- Bonds struggled as inflation expectations rose

- Traditional support levels began to fail

What stood out most was how quickly sentiment changed. Just weeks ago, markets were pricing in a relatively stable environment. Now, the narrative has flipped to “higher inflation for longer” and potential policy uncertainty.

In simple terms:

Markets are no longer trading data — they’re trading risk.

Week Ahead: Economic Data Takes a Back Seat (But Still Matters)

Even though geopolitics remains the main driver, this week brings several important economic releases that could shape how central banks respond.

United States: Jobs and Consumption in Focus

Retail Sales (Wednesday)

Retail sales are expected to show some strength, largely due to solid auto sales. However, the bigger concern is underneath the surface.

Higher energy prices act like a tax on consumers. When people spend more on fuel, they tend to cut back elsewhere. That means discretionary spending could weaken, even if headline numbers look decent.

There’s also a possibility that manufacturing data surprises to the upside. We’ve already seen signs in Europe that manufacturing is holding up better than services, possibly because businesses are front-loading orders ahead of further price increases.

Key takeaway:

Headline strength may mask weakening consumer demand.

Non-Farm Payrolls (Friday)

This is the big one.

The labour market has effectively stalled over the past year. Outside of a few sectors like government and healthcare, job growth has been weak or negative.

February’s loss of 92,000 jobs was likely exaggerated by temporary factors like weather and strikes. A modest rebound is expected, but the broader trend remains soft.

This puts the Federal Reserve in a difficult position:

- Inflation may rise due to oil

- But employment is not strong

That creates a key question:

Will the Fed “look through” energy-driven inflation, or react to it?

Eurozone: Confidence Shock and Inflation Reversal

Economic Sentiment (Monday)

Confidence across Europe has taken a clear hit.

Consumers are dealing with two major fears at once:

- Rising prices

- Geopolitical uncertainty

This combination has pushed sentiment sharply lower. Businesses are also feeling the pressure, particularly in services, while manufacturing has been more resilient.

Watch for:

Signs of stress in energy-intensive industries.

Inflation (Tuesday)

Inflation is expected to move higher again, largely due to energy.

This marks a shift from the recent period where inflation seemed to be stabilizing. That “comfort zone” for central banks is now under threat.

The implication:

The ECB may have less flexibility than markets previously expected.

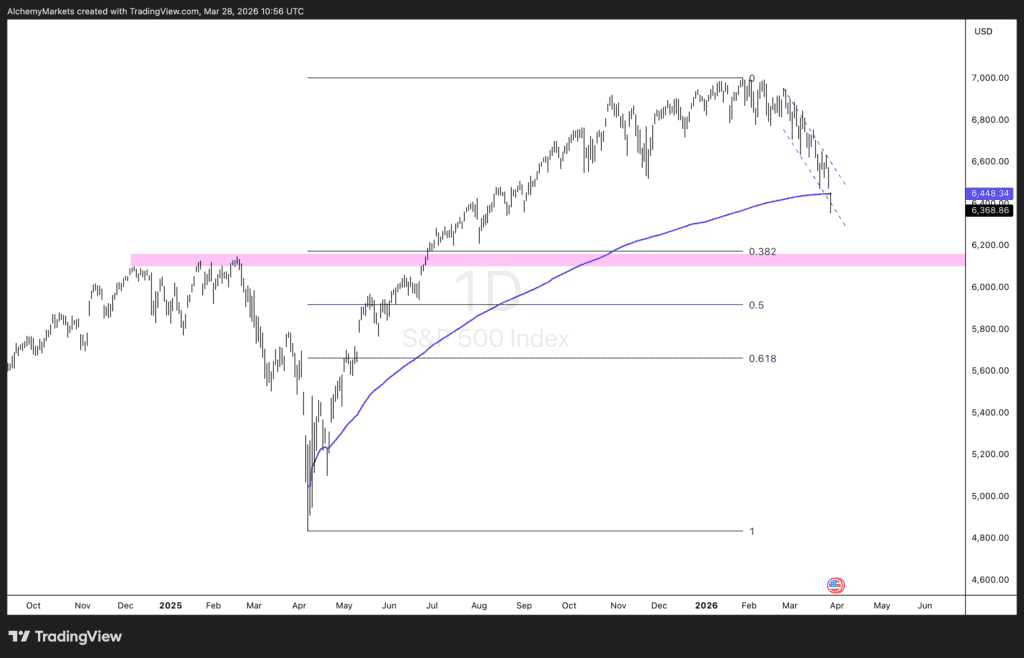

S&P 500 Technical Outlook: Anchored VWAP Fails to Hold

From a technical perspective, last week’s price action in the S&P 500 was telling.

The market broke below the anchored VWAP from the April 2025 lows, a level that had previously acted as strong dynamic support. The fact that price could not hold this level highlights just how aggressive the selling pressure has become.

When key support tools like VWAP fail, it often signals a shift in market structure rather than just a short-term pullback.

Now, attention turns to a key confluence zone below:

- December 2024 resistance

- February 2025 resistance

- 38.2% Fibonacci retracement from the April 2025 lows

This area becomes the next logical level where buyers may attempt to step in.

The key idea:

Old resistance may now act as new support — but only if sentiment stabilises.

Final Thoughts: A Market at a Crossroads

Markets are entering the week with a clear tension between:

- Geopolitical-driven inflation risk

- Weak underlying economic momentum

If oil prices remain elevated, inflation fears will likely continue to dominate. But if economic data weakens further, central banks may be forced to stay patient.

For equities, the technical picture has clearly deteriorated. The failure of anchored VWAP suggests that this is more than just a shallow dip.

Going into the week ahead:

- Watch oil prices first

- Then watch the jobs report

- And finally, see whether key technical levels hold

Because right now, macro is in control — and technicals are reacting, not leading.