Written by:

- Quarterly Forecast

- March 31, 2026

- 9 min read

Q2 2026 Forex Outlook: USD, EUR, JPY & Top FX Trades to Watch

Q2 does not look like a straightforward directional quarter for forex. The market keeps trying to price de-escalation, but oil, inflation and policy expectations are still tied to an unstable geopolitical backdrop. That leaves the quarter feeling reactive rather than settled. The better opportunities are not broad one-way trades, but relative-value trades where policy, growth and inflation are pulling currencies in different directions.

The broad policy picture reflects that shift. The Fed is on hold and cuts have been pushed back. The Bank of Japan still carries the strongest tightening bias in G10. The ECB and BoE remain on hold, but renewed inflation pressure does not fix weak growth. The RBA has already delivered a March hike and still carries a higher-for-longer bias, while the RBNZ looks softer and more conditional. Together, that keeps the dollar supported early in Q2, the yen with the strongest policy tailwind, the euro as the weakest major, and AUD better placed than NZD in the commodity bloc.

| Download Full Report: Get the full Q2 2026 FX Outlook with detailed policy paths, macro scorecards, scenario risks, and technical setups across the major pairs. |

Why Q2 looks reactive rather than directional

This is no longer just a geopolitical premium story. Damage to energy infrastructure, disrupted Hormuz flows and persistent supply shocks mean the market cannot simply price a return to normal. Oil may dip on a hopeful headline, but the underlying supply risk has not been fully removed. That keeps inflation risk alive and makes central banks slower to turn easier.

That also explains why the quarter can swing between risk-on and risk-off reactions depending on the headline. The market wants relief, but the structure underneath still favours caution. In practical terms, traders should spend less time looking for the single strongest currency and more time looking for pairs where the macro split is wide enough to create clearer relative moves.

The central-bank map for Q2

The Fed remains on hold in the 3.50% to 3.75% range, and the key change is not the hold itself but the repricing around it. Expectations for easier policy have been pushed further out as oil risk has become more prominent. Higher oil prices are no longer just a commodity story. It is a policy variable that can delay or reduce the probability of Fed easing. That is why USD downside is no longer a simple call. The dollar still looks supported through early Q2, and only becomes less stable later in the quarter if growth softens enough, and oil calms enough, for deferred easing expectations to rebuild.

| Currency | Central Bank | Current rate | April | May | June |

| USD | Fed | 3.50%–3.75% | Hold | Hold | Hold (cuts pushed back) |

| EUR | ECB | 2.00% | Hold | Hold | Hold |

| GBP | BoE | 3.75% | Hold | Hold | Hold (split risk) |

| JPY | BoJ | 0.75% | Hold (hike risk live) | Hold | Tightening bias remains |

| CHF | SNB | 0.00% | Hold | Hold | Hold |

| AUD | RBA | 4.10% | Hold | Hold | Hold (higher-for-longer) |

| NZD | RBNZ | 2.25% | Hold | Hold (conditional hawkish risk) | Hold (conditional hawkish risk) |

| CAD | BoC | 2.25% | Hold | Hold | Hold |

The table above keeps the broad policy path together. The sharper relative-value story still comes from how these policy stances interact with growth, inflation and energy exposure across each currency.

The BoJ remains the standout on the other side of the spectrum. A 0.75% policy rate is still low in absolute terms, but live hike risk and a tightening bias make it the strongest policy-upside story in G10. That does not automatically make JPY a straight-line winner against everything, but it does make yen strength one of the clearest relative themes in the quarter when paired against weaker macro profiles.

The ECB and BoE are both more awkward stories. They remain on hold, and inflation pressure can still keep the tone hawkish at the margin, but that does not solve the deeper issue. Europe still carries the weakest growth and energy mix, while the UK sits in the middle with sticky inflation, softer growth and uncertain policy direction. That keeps EUR structurally fragile and GBP more range-bound than decisive.

In the commodity bloc, AUD and NZD are no longer equal. The RBA has already moved back to 4.10% and still carries a higher-for-longer bias, which gives AUD more upside optionality when risk conditions stay calm. The RBNZ, by contrast, remains on hold with only conditional hawkish risk. NZD can still bounce in short risk-on windows, but it lacks the same policy support. CAD sits somewhere else again. Firmer oil can cushion CAD, but a deeper energy shock can still favour USD if it delays Fed easing and pushes the market into a more defensive stance.

The strongest currency themes for Q2

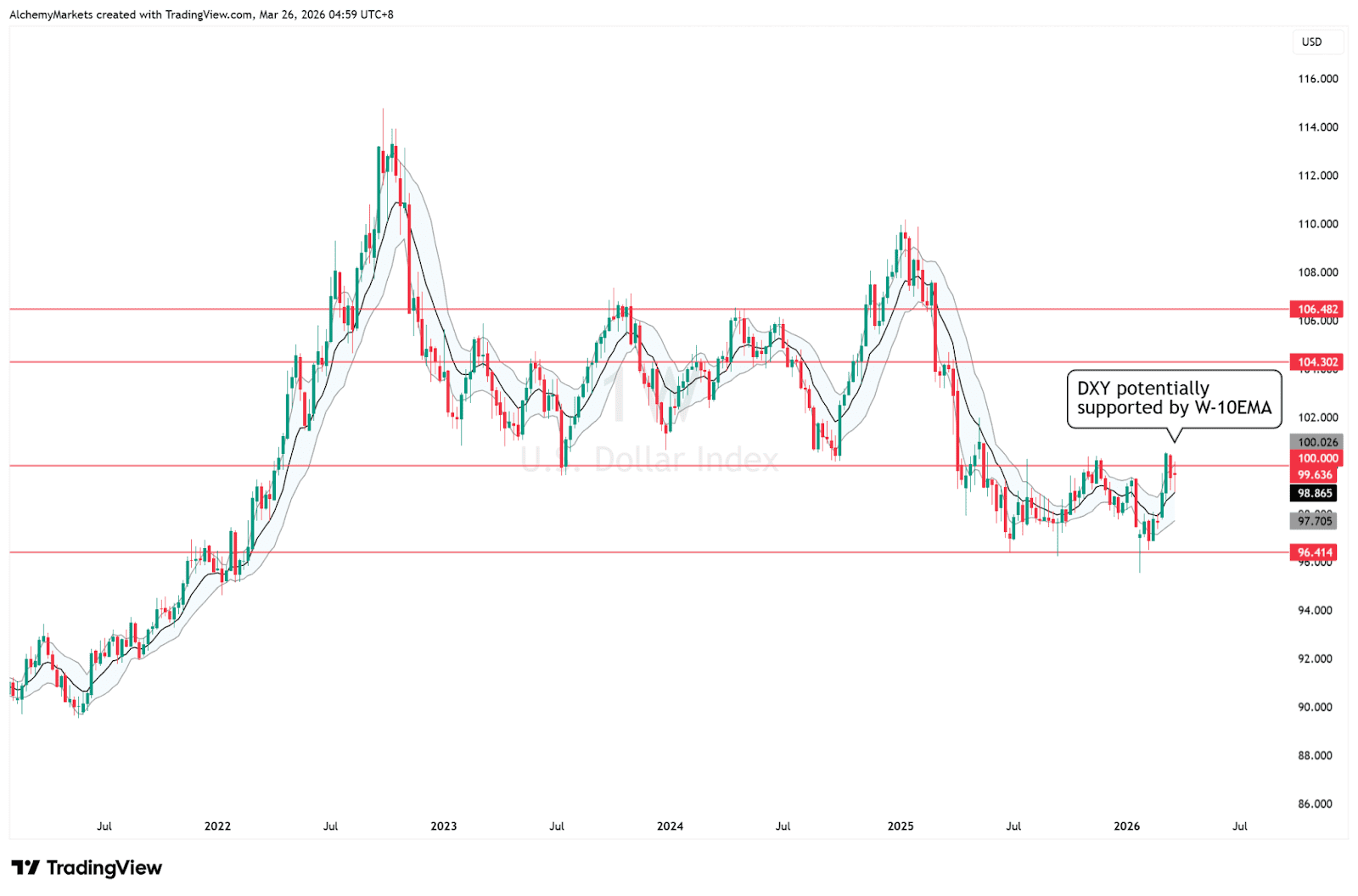

The dollar still looks supported early in the quarter, but it does not look like a broad breakout story. The better way to think about USD is as a supported currency whose edge fades only if slower growth starts to pull rate-cut expectations back into view later in Q2. That makes DXY more of a support chart than a breakout chart. As long as the weekly trend support holds, broad dollar support remains intact.

Chart 1. DXY weekly

The yen has the strongest policy tailwind. That matters because it gives JPY a firmer foundation than the market’s more reactive risk currencies. The euro remains the weakest major because hawkish repricing cannot repair weak growth or heavy exposure to imported energy pressure. Sterling is stronger than EUR in relative terms, but still lacks the macro edge needed for a strong directional trend. AUD has upside optionality, especially relative to NZD, while CHF remains more useful as a quiet hedge than as a pure rate trade. CAD remains conditional rather than outright bullish because oil can support CAD at the margin without preventing USD from outperforming if the shock keeps the Fed tighter for longer.

The best FX pairs to watch in Q2

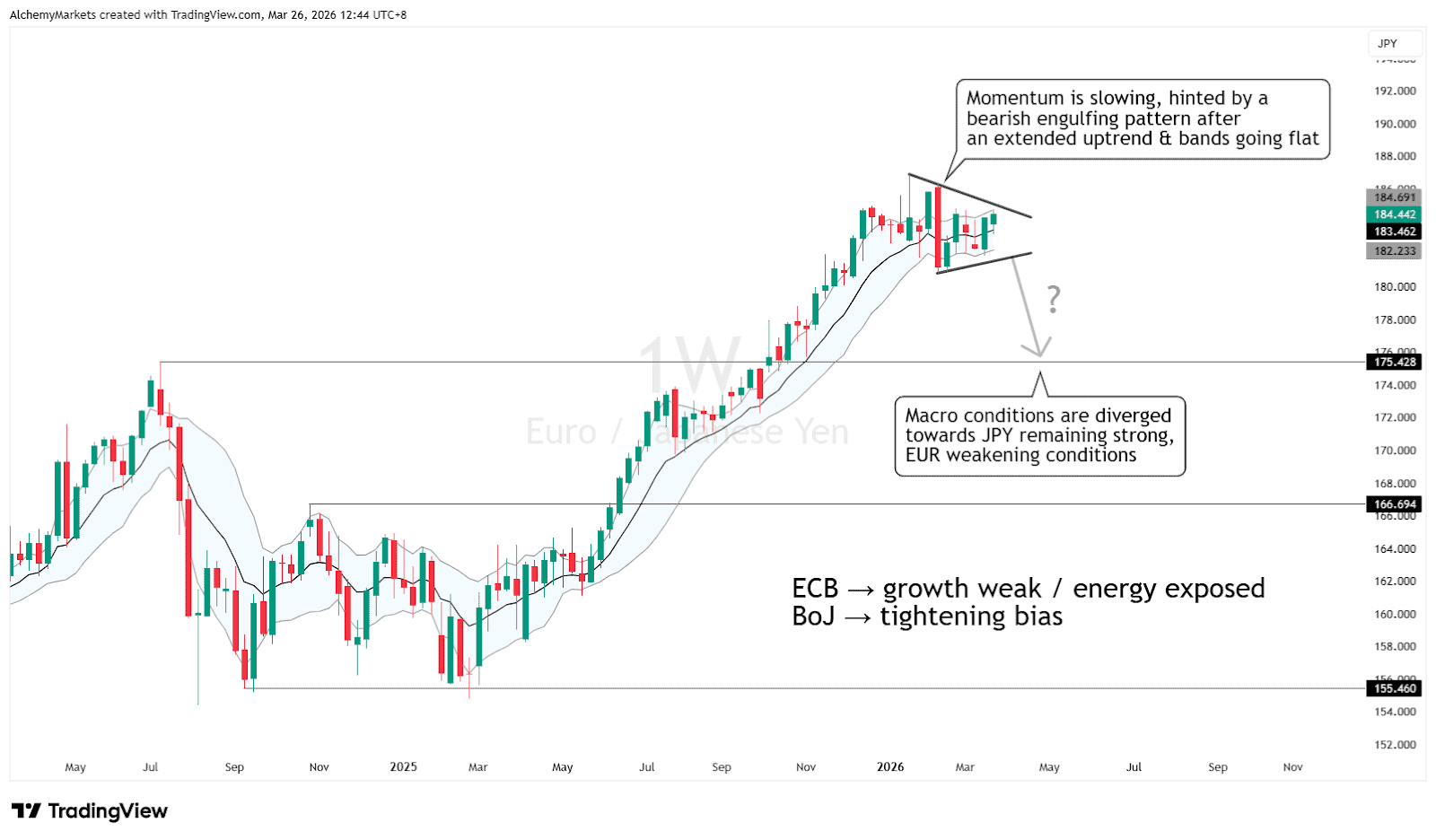

EURJPY looks like one of the strongest expressions in the whole report. The macro split is obvious: ECB growth fragility versus BoJ tightening bias. On the chart side, momentum has slowed after an extended move higher, and bearish rotation risk would rise if rallies start failing into resistance. This is the sort of pair where macro divergence and structure can work together rather than against each other.

Chart 2. EURJPY weekly

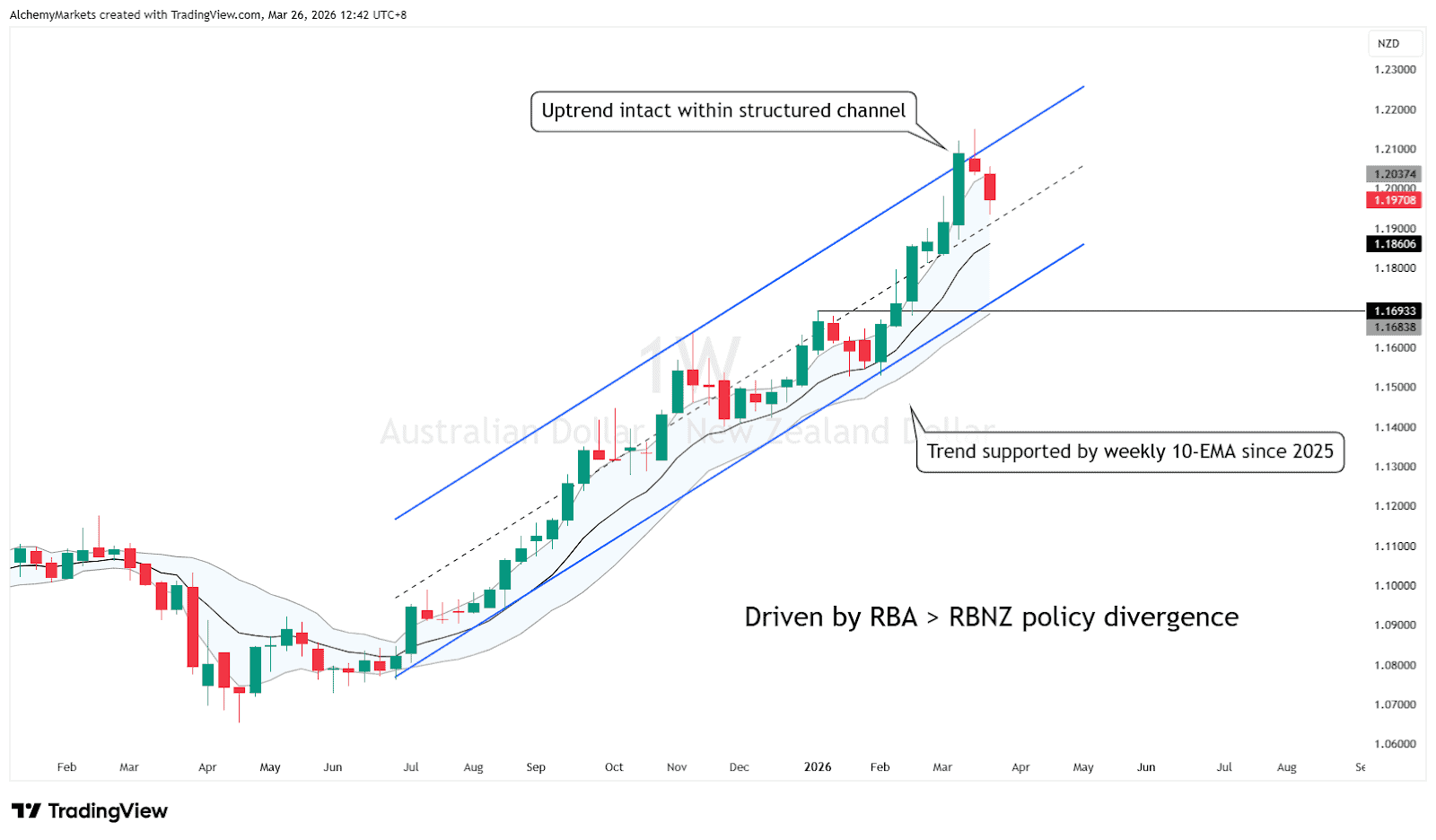

AUDNZD is the clearest trend expression in the commodity complex. The pair remains in a structured uptrend, the weekly EMA has repeatedly acted as support, and the macro driver is straightforward: RBA policy looks firmer than the RBNZ after the March hike. This is one of the few places where the quarter still offers a relatively clear directional divergence trade.

Chart 3. AUDNZD weekly

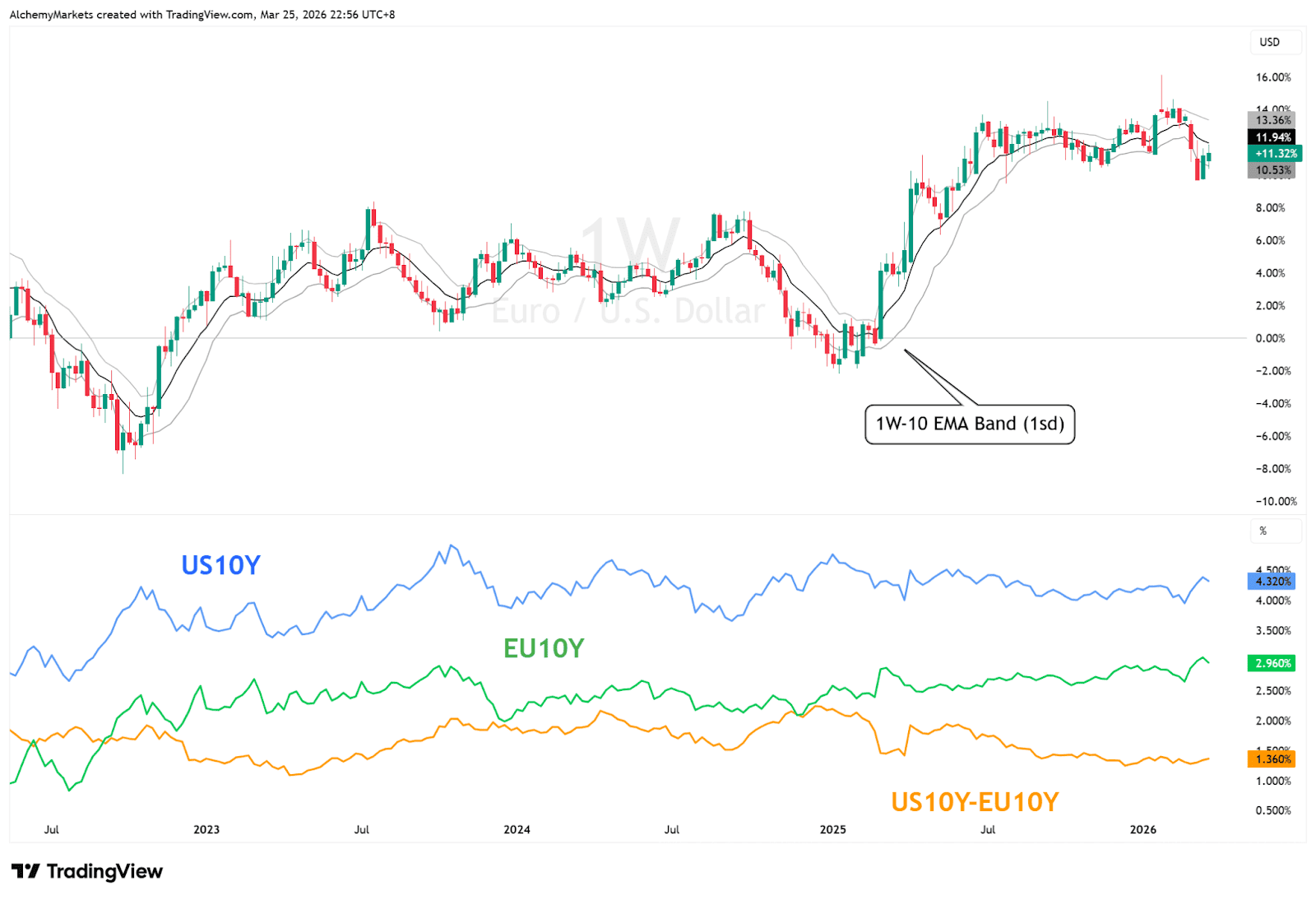

EURUSD still looks like a fade-strength market rather than a convincing bullish reversal. The spread continues to favour the dollar, price has slipped back below its weekly trend band, and a more hawkish ECB still does not fix Europe’s weak growth and energy problem. That means squeezes higher are possible, especially if the dollar softens on growth concerns later in the quarter, but the broader Q2 read still favours rallies failing unless the pair can reclaim and hold weekly structure.

Chart 4. EURUSD weekly

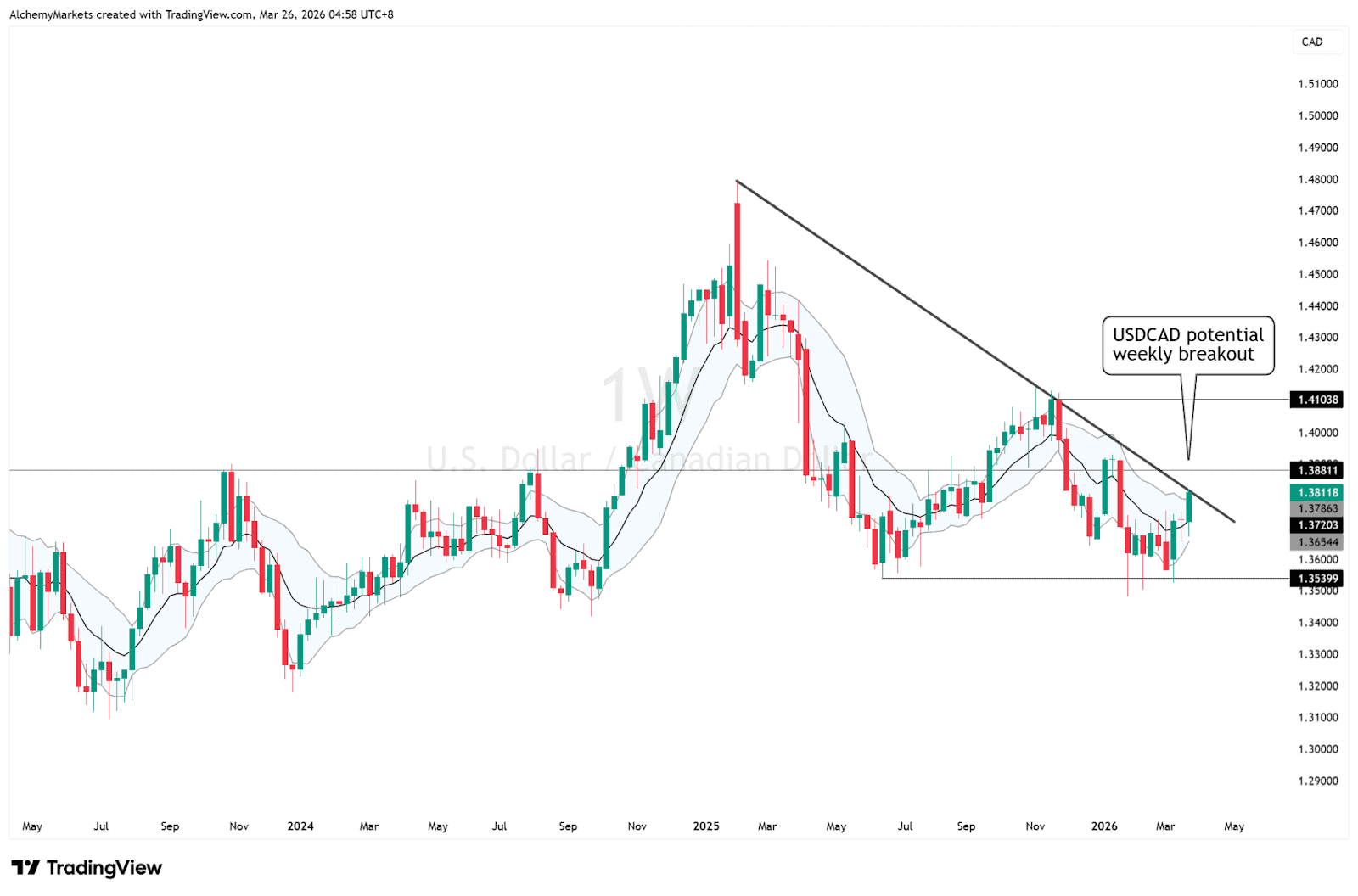

USDCAD is one of the stronger USD expressions, but only if the oil story stays balanced. Firmer oil can cushion CAD, which is why this is not a one-variable trade. Even so, the pair still looks more constructive than USDCHF because the structure is firmer and the relative macro setup remains supportive if Fed easing stays delayed. It becomes more attractive if oil cools rather than spikes.

Chart 5. USDCAD weekly

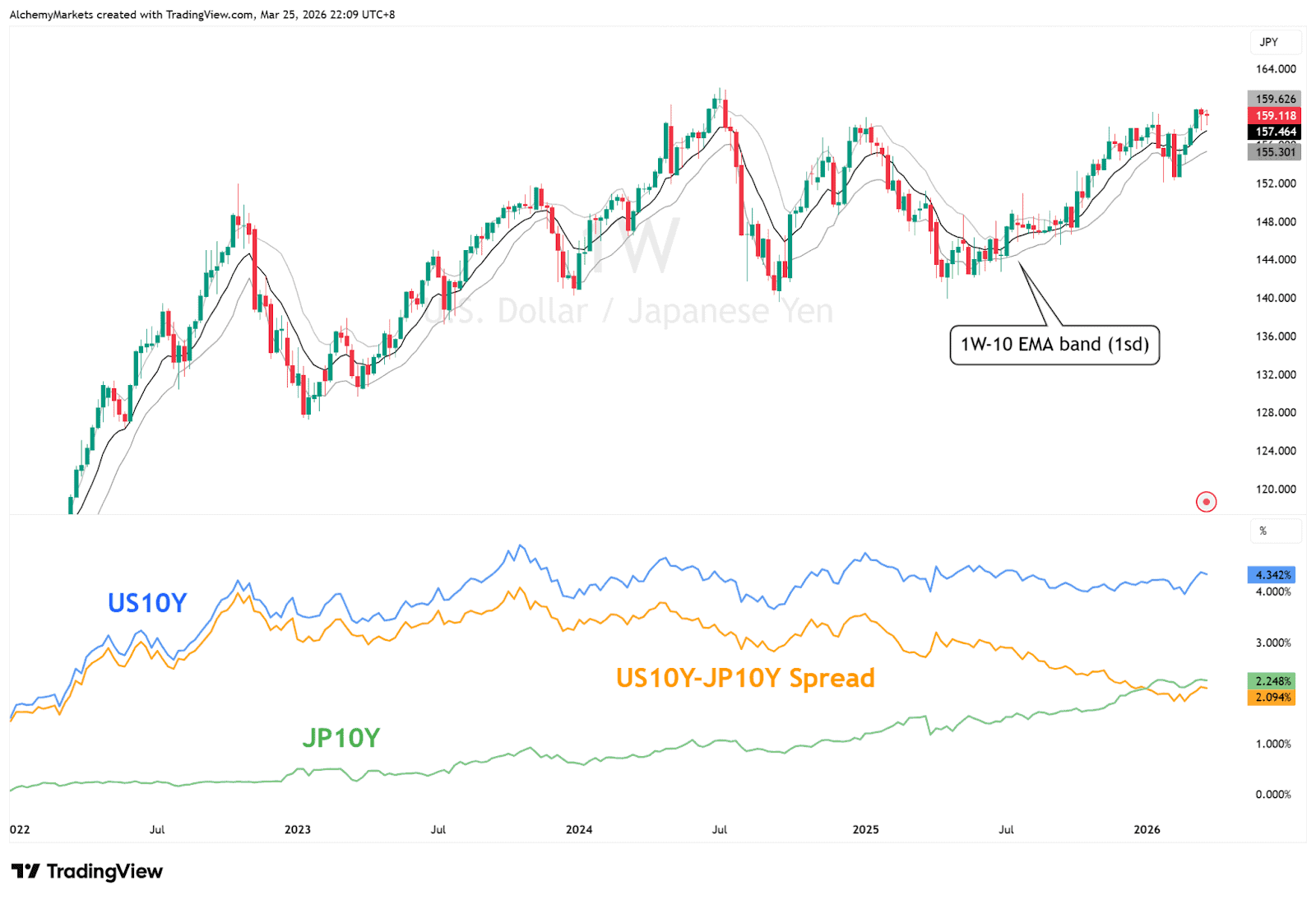

USDJPY remains tradable, but it is no longer a straightforward chase-higher market. The U.S.-Japan yield spread still supports carry, yet BoJ tightening risk means pullbacks can deepen quickly if the spread compresses. That leaves the pair in a buy-dips category rather than a breakout category. It is still useful, but less straightforward than EURJPY or AUDNZD for a quarterly view.

Chart 6. USDJPY weekly

Why headline risk still matters

One reason this quarter looks so reactive is that Q1 already established a repeatable market pattern. Signals of progress were followed by short-term relief, then contradiction or escalation within a day or two, and then repricing once the market realised the underlying tension had not disappeared.

The same instability also showed up in the data. January payrolls beat expectations, February payrolls then fell sharply, and the annual benchmark revision showed the labour backdrop had been weaker than previously reported. That combination matters because it reinforces the same lesson on both the geopolitical and macro side: the first reaction to a headline is tradable, but not reliable enough on its own. Confirmation from oil, rates and price structure matters more.

What matters most in Q2

The more likely outcome is a headline-driven quarter where oil stays elevated enough to support the dollar early, but not enough to create a one-way panic. A less likely but still possible outcome is a credible de-escalation that stabilises oil and allows a more sustained risk-on move. The key watchpoints are straightforward: Hormuz access, infrastructure damage, late-week political signalling, BoJ follow-through and any renewed repricing of Fed cuts. Those will tell traders whether Q2 remains a rotation market or starts to shift into something more directional.

Final outlook

The biggest mistake in Q2 would be treating forex as a simple directional story. This quarter is better understood as a divergence and rotation market. The dollar still has support early on, but not in a way that justifies a blind bullish view. The yen still has the strongest policy upside. The euro remains the weakest major. AUD looks stronger than NZD on relative policy support. GBP sits in the middle, CHF remains the quiet hedge, and CAD stays conditional because oil can help both sides of the pair depending on how the shock feeds into policy.

The best Q2 framework is simple enough: focus on the pairs where macro conditions are most clearly misaligned, let the weekly chart decide whether structure agrees with that view, and do not trust headlines without confirmation from oil, rates and price. In this quarter, divergence matters more than direction.