Written by:

- Quarterly Forecast

- April 1, 2026

- 6 min read

Q2 2026 Equities Forecast: SPX, Nasdaq, Dow, DAX & FTSE 100

Q2 2026 looks like a transition quarter, not a clean trend quarter. The macro backdrop is leaning toward slower growth, firmer energy costs, and central banks that are less able to ease quickly than markets would like. The Fed held rates at 3.50% – 3.75%, the ECB kept rates unchanged and explicitly flagged higher energy prices as an upside inflation risk and downside growth risk, and the Bank of England also held Bank Rate at 3.75%. At the same time, March business surveys have softened in the U.S., euro area, and UK as higher energy costs feed through to activity and inflation expectations.

So the right framing is:

Technical structure first. Macro explains why breakouts may struggle to hold.

Macro overlay for Q2 2026

1) Energy / oil

This remains the key macro variable for Q2. Higher oil is already feeding into inflation expectations, pressuring margins, and weighing on activity. A sustained move higher keeps central banks cautious and caps equity upside.

2) Central banks

The Fed, ECB, and BoE all held steady. That matters because markets were leaning toward easier policy. Sticky inflation reduces the room for quick cuts, meaning equities lose a key tailwind.

3) Growth data

PMIs are softening rather than collapsing. That creates a difficult middle ground: not weak enough for aggressive easing, not strong enough for clean upside trends.

4) Valuation / positioning

Markets entered Q2 from elevated levels. That makes them more sensitive to macro disappointments, but also creates room for sharp technical rebounds when positioning gets stretched.

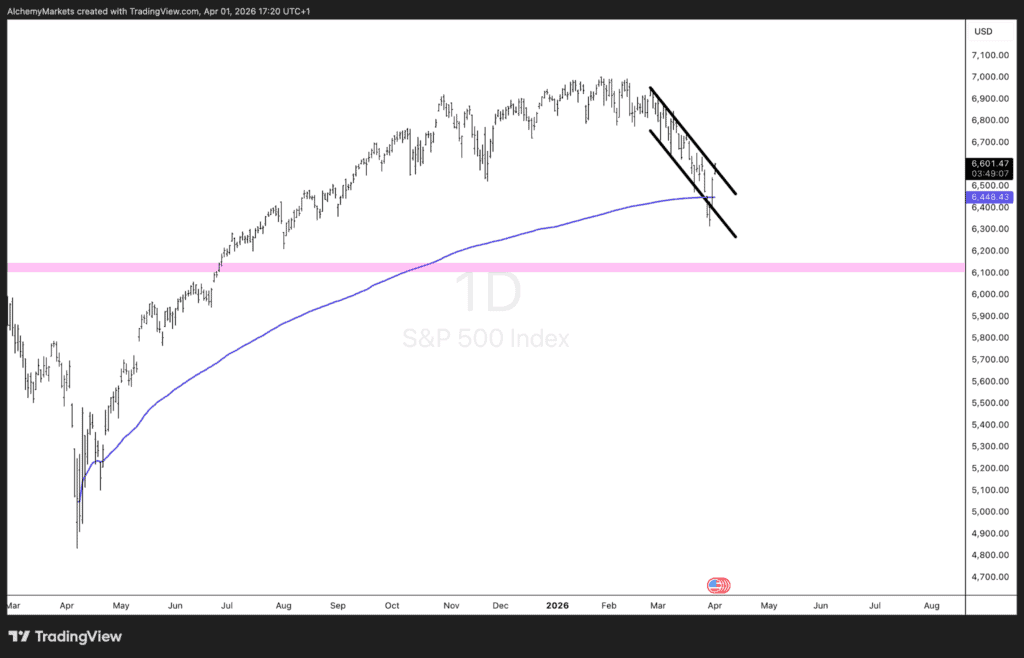

S&P 500 (SPX) – Q2 2026 forecast

Technical view

The weekly structure has improved slightly. Price is attempting to break out of the short-term descending channel, suggesting the correction may be transitioning into a recovery attempt rather than extending cleanly lower. However, this is not a confirmed trend re-acceleration—more a shift into a broader range.

Macro backdrop

This still fits the macro mix: softer activity, elevated energy, and a Fed on hold. That environment allows rebounds, but makes sustained breakouts harder to maintain.

Q2 expectation

Base case: range-bound with upside attempts.

- Upside scenario: break higher toward 6,800, with scope to test 7,000 if inflation pressure eases

- Downside scenario: rejection brings price back toward 6,100–6,200 support

Bias

Neutral, with two-way opportunity rather than directional conviction.

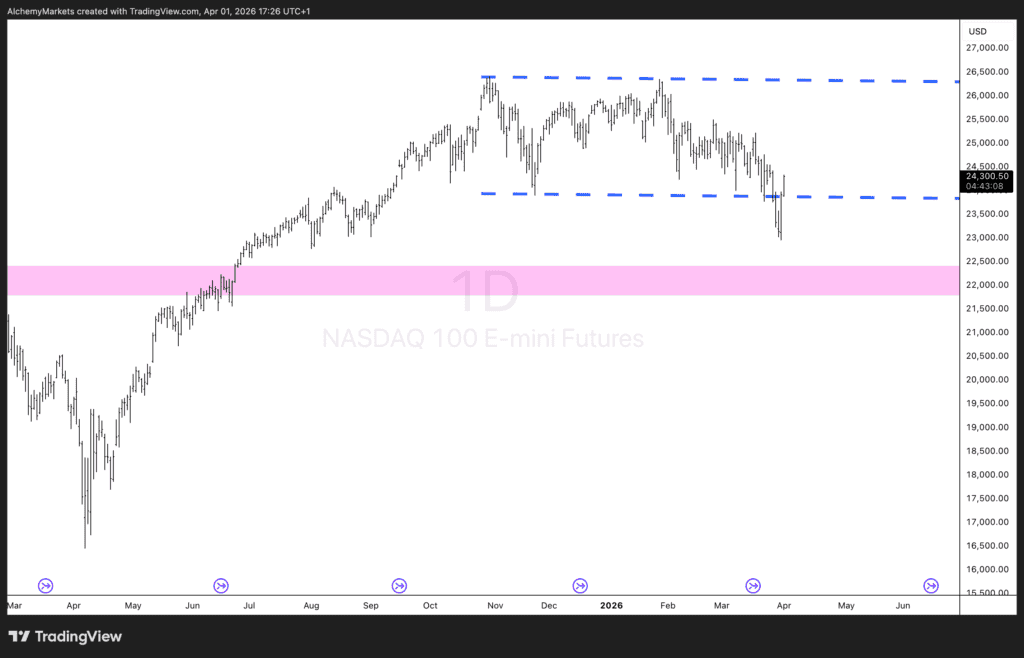

Nasdaq 100 (NQ) – Q2 2026 forecast

Technical view

Price has moved back inside its prior range, removing immediate breakdown risk. The structure now looks like a broad distribution range rather than a clean trend.

Macro backdrop

Still the most rate-sensitive index. Less dovish expectations and higher energy keep pressure on growth valuations.

Q2 expectation

- Near term: downside pressure toward 22,000 support

- Medium term: potential rebound toward 26,000–26,500 resistance

Bias

Range-bound and volatile. Rallies likely tactical unless the upper range is reclaimed.

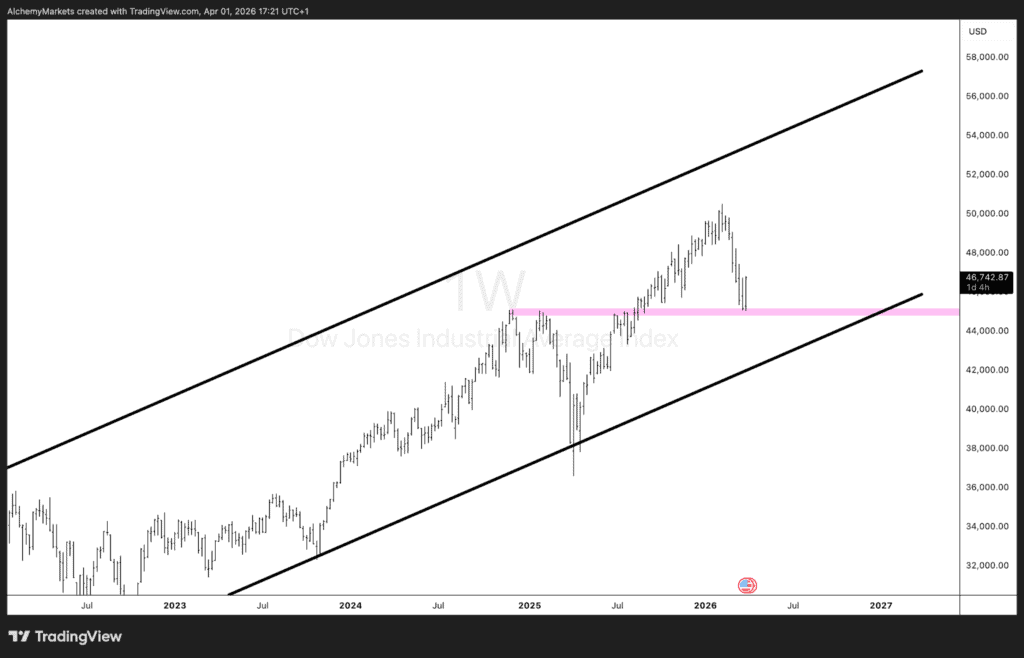

Dow Jones Industrial Average (DJI) – Q2 2026 forecast

Technical view

Price is sitting on the 45,000 support zone, now acting as the key pivot. The broader ascending structure remains intact, but this is a test of trend support.

Macro backdrop

More defensive composition continues to suit a slower-growth, sticky-inflation environment.

Q2 expectation

- Breakdown: move toward lower channel support

- Medium term: likely bounce from lower structural support

Bias

Relatively constructive versus Nasdaq, but still range-bound overall.

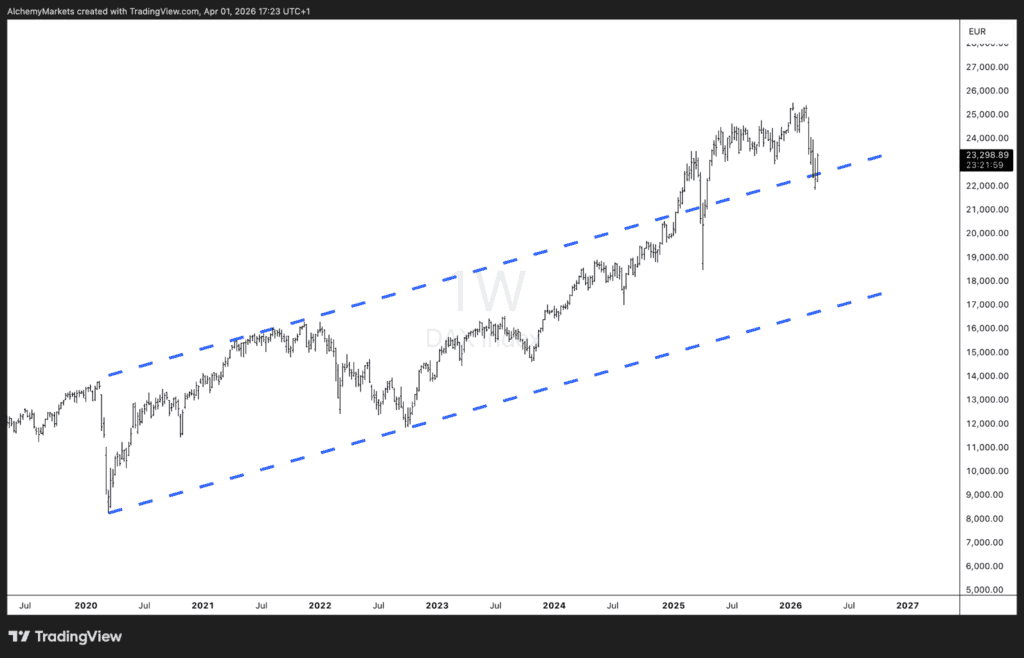

DAX – Q2 2026 forecast

The DAX daily chart still sits inside a long-term rising channel, but price has pulled down from the upper boundary and is now testing the middle-to-lower portion of that structure near 22,600. That is a meaningful technical inflection: it is still an uptrend on a broad basis, but momentum has clearly cooled.

The problem is not the long-term trend. The problem is follow-through.

Macro backdrop

That matches the macro backdrop in Europe. Euro area growth nearly stalled in March, the ECB kept rates unchanged, and it explicitly warned that the war in the Middle East raises inflation risks while hurting growth. Reuters also reported euro zone industry was already weak even before the latest energy shock. Germany is one of the most exposed large equity markets when energy and industrial activity become the issue.

Q2 expectation

Base case: volatile, headline-driven, and weaker than U.S. defensives on a relative basis.

Bias: neutral-to-bearish for Q2 unless energy pressure eases quickly.

Levels from the chart

- Support: around 22,500–22,600

- Lower channel support: mid-to-high 21,000s

- Resistance: 24,000, then 25,000 area

Forecast

My Q2 view on DAX is unstable upward structure, but poor trend quality. It can bounce sharply, but macro headwinds argue against a clean sustained advance in the quarter.

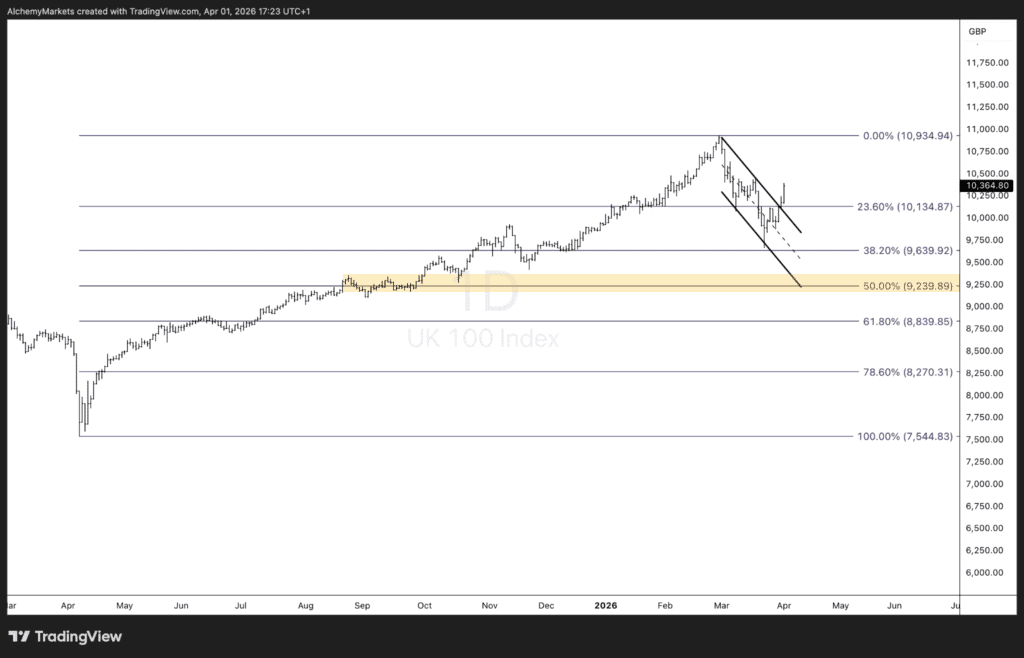

FTSE 100 – Q2 2026 forecast

Technical view

The FTSE is approaching a near-term ceiling around 10,400, suggesting potential short-term exhaustion after the recent rebound.

Macro backdrop

Its exposure to energy, commodities, and defensives continues to provide relative support in an inflation-sensitive environment.

Q2 expectation

- Near term: stall around 10,400

- Downside: rotation toward ~9,250 support

- Medium term upside: 11,250 if macro stabilises

Bias

Relative outperformer, but not immune to volatility.

Relative ranking for Q2 2026

From strongest expected relative behaviour to weakest:

- FTSE 100 – best hedge against sticky inflation / higher energy

- Dow – defensive stability

- S&P 500 – range-bound, two-way

- DAX – macro vulnerable

- Nasdaq 100 – most unstable under current conditions

Q2 2026 scenario framework

Bull case

Oil cools, inflation improves, rate cuts get priced back in, and growth stabilises.

→ Broad upside, with Nasdaq leadership returning.

Base case

Oil remains elevated but stable, growth slows modestly, and central banks stay cautious.

→ Range-bound, rotational, and macro-sensitive.

Bear case

Oil spikes, inflation expectations rise, and growth deteriorates more sharply.

→ Equity downside led by Nasdaq and DAX.

Bottom line

Q2 2026 should still be treated as a volatile, macro-driven, range-bound quarter. The difference now is that markets are no longer cleanly rolling over—they are attempting to stabilise and push higher within that range.

The technical picture shows loss of trend quality, not full breakdown, and the macro backdrop explains why: higher energy prices, softer activity, and central banks that cannot quickly pivot to easing.

PM-style conclusion:

- SPX: range-bound with upside attempts

- Nasdaq: volatile, range-driven, least stable

- Dow: defensive relative strength

- DAX: macro-sensitive and fragile

- FTSE 100: best relative resilience

The key shift for Q2 is:

Expect two-way price action, failed breakouts, and tactical moves rather than sustained trends.

So the playbook becomes:

- Trade levels, not narratives

- Stay flexible on direction

- Focus on relative strength, not broad index beta

You may be interested to read our: