Scritto da:

- Weekly Outlook

- Giugno 13, 2026

- 6 min di lettura

The Peace Premium Comes Due: Fed, BoE & the Oil Comedown

For three months, one chokepoint in the Persian Gulf wrote the macro narrative for everyone. The Strait of Hormuz did the work that data usually does — it set the inflation path, it set the dollar’s tone, it set the risk mood. Brent ripped from the low-$60s to north of $110 at the peak, and every central bank on earth suddenly had the same problem handed to them by the same map.

That chapter is now closing. Over the weekend, reports landed that Washington and Tehran have agreed the “final” text of a peace deal, the clearest signal yet that the supply shock has an expiry date. Oil eased, equities caught a bid, and for the first time since February the tape is being allowed to trade on something other than a missile headline.

Here’s the catch, and it’s the whole point of next week: de-escalation doesn’t hand you back the old world. It hands you a world where the inflation that the war injected is still sitting in the system — in fuel, in shipping, in the lag before household energy bills reset — while the catalyst that caused it fades from the front pages. That’s the awkward gap central banks have to navigate, and it’s why a single week containing the Fed, UK CPI, UK jobs and the Bank of England is going to matter far more than the calm price action suggests.

And they are emphatically not aligned. The consensus that normally binds the major central banks has fractured along the fault line the oil shock opened. Some are leaning hawkish into the inflation overshoot; others are insisting the next move is still, eventually, a cut. Next week is where those diverging reaction functions get tested against live data — and where the dollar, gilts and crude all have to pick a side.

The non-obvious read: the war was the easy part to trade. The peace is harder. A fading premium pulls oil lower even as the inflation it left behind keeps the hawks talking — and that tension is exactly what the price action is starting to whisper before the calendar confirms it.

The week ahead — economic calendar

(All times BST / GMT+1. Consensus figures indicative and subject to revision into the events.)

Wednesday 17 June

- FOMC Rate Decision, Statement & Dot Plot — 19:00 | Press conference 19:30. The event of the week. Rates expected on hold, but this is the quarterly Summary of Economic Projections, so the dot plot is the story. With momentum improved and fuel-driven inflation elevated, the risk is that more officials pencil in a hike before year-end than a cut — a genuinely awkward backdrop for new Chair Kevin Warsh, installed by a president who wants borrowing costs lower. Watch how high the median dot drifts; a median above the current rate would be the loudest hawkish signal on the page.

- UK CPI (May) — 07:00 | Consensus: rebound from April. Inflation was artificially softened in April by Easter timing and should bounce back. Too early to pin much on second-round effects from the conflict, and too early to see the full oil/gas pass-through — household energy bills stay capped until July. Lands less than 24 hours before the BoE, so it sets the tone for the vote.

Thursday 18 June

- UK Jobs / Labour Market — 07:00. Arriving hours before the Bank decides. Last month’s figures were grim, including a sharp drop in payrolled employment — the key question is whether those numbers get revised higher.

- Bank of England Rate Decision — 12:00. Hold expected, but the vote split is the trade. Chief Economist Huw Pill dissented alone in April; a recent speech all but confirms Megan Greene joins him. Base case is a 7–2 hold — the hawkish risk is Claire Lombardelli and/or Catherine Mann making it 6–3 or tighter. The more dissenters, the more a 2026 hike moves from tail risk to base case.

Lower-tier, worth a glance:

- US Retail Sales (May) — 13:30. Flattered by higher nominal prices at the pump; strip that out and the control group likely stays subdued.

- US Industrial Production (May) — 14:15. Manufacturing output should keep getting a lift from the data-centre rollout and the broader tech investment cycle.

The thread tying it together: every one of these prints feeds the same question — with the war premium draining out of oil, does the inflation it created stay sticky enough to keep the hawks in control? The Fed’s dots and the BoE’s vote count are two different committees answering that exact question in the same 18 hours.

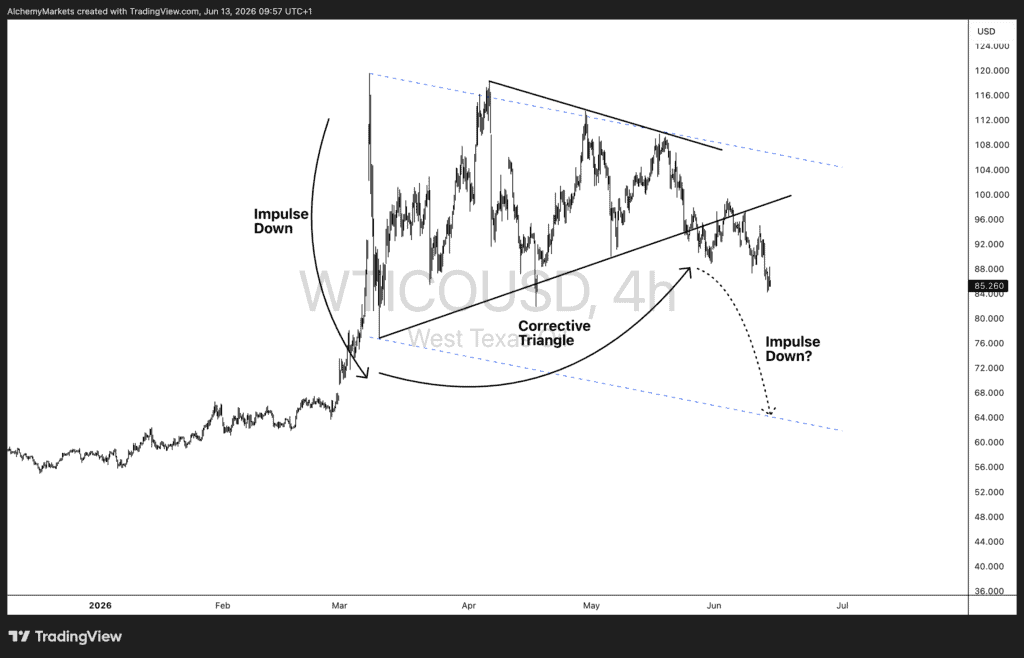

Technical focus — WTI Crude (WTICOUSD, 4H)

The chart has been telling this story ahead of the headlines, and it’s lining up for a potential sequel.

Cast back to early March: oil printed a violent impulse down off the ~$120 spike, the first crack in the war premium. What followed wasn’t a recovery — it was a corrective triangle, the textbook consolidation that forms between impulse legs while the market digests. Price has spent three months coiling inside that structure, chopping between a rising lower bound and the descending upper boundary of the broader channel, never convincingly reclaiming the highs.

Now the apex is behind us and price is leaning on the lower edge again, hovering in the mid-$80s. With the US–Iran conflict cooling and the supply-disruption bid deflating, the fundamental fuel for another upside spike is being pulled away just as the technical structure resolves lower. That’s the confluence: a corrective pattern that wants to break down, meeting a catalyst that’s fading exactly when bulls need it most.

The roadmap on the chart asks one question — Impulse Down? A decisive break and hold below the triangle’s lower bound opens the path toward the descending channel’s lower boundary, projected into the low-to-mid $60s as the dashed channel support slopes through the coming weeks. That would be a clean measured continuation of the move that started in March.

The invalidation is equally clean: oil doesn’t move in a straight line, and any re-escalation — a stalled deal, a Hormuz flare-up — would slam the war premium straight back into the price and reclaim the triangle. Watch the lower channel boundary as the decision line. While price respects it from above, the structure favours the sellers; a strong reclaim of the triangle flips the script.

The market is doing what it always does — pricing the change in narrative before the narrative is officially confirmed. Peace is being negotiated on the wires; the chart is already trading the comedown.