Scritto da:

- Weekly Outlook

- Giugno 19, 2026

- 6 min di lettura

The Inflation Print That Could Reset the Rate Debate

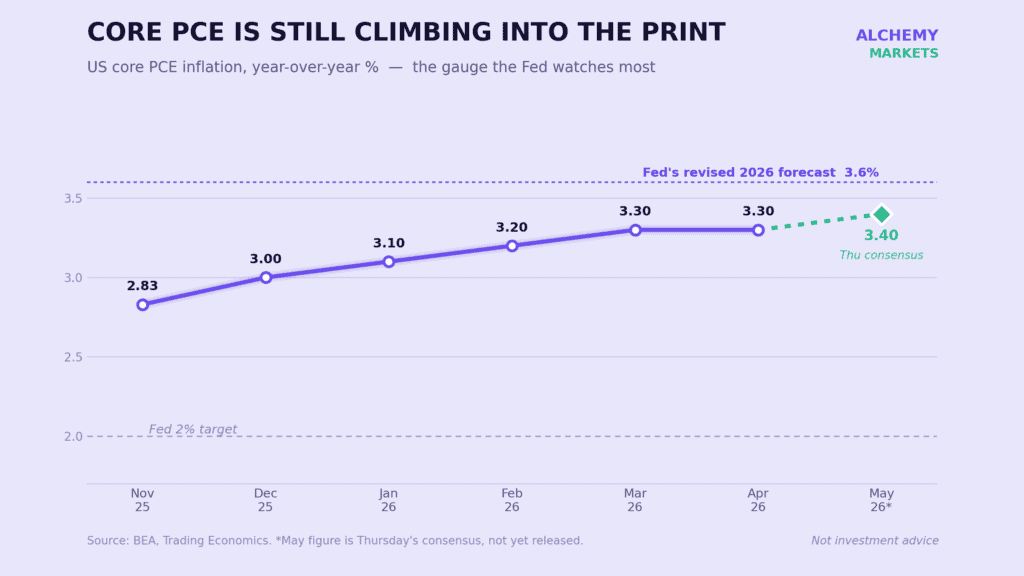

Last week handed markets a Fed that effectively banned the phrase “rate cut.” Kevin Warsh’s debut as Chair was supposed to confirm the dovish lean priced into rates earlier this year. Instead, the FOMC held at 3.50% to 3.75% for a fourth straight meeting and then quietly took a hatchet to its own guidance. The statement lost its easing bias, the dot plot flipped, and nine of eighteen participants now pencil in at least one hike before year-end. The median 2026 dot rose to 3.8% from 3.4% in March, with the inflation forecast revised sharply higher to 3.6% PCE and GDP nudged lower to 2.2%. Front-end yields led the selloff, the two-year jumping roughly 11 basis points, and equities closed in the red. The message was unambiguous: the only direction this committee is willing to discuss is up.

Here is where it gets interesting, and where the week ahead matters. There is a credible case that the Fed has this backwards. The jobs market rebound looks less convincing once you strip out health, social care and hospitality, which together account for a quarter of employment but two thirds of this year’s growth. Wage pressure outside those pockets is muted. Housing rents are barely rising, and given housing’s heavy weight in core inflation, that should drag the index lower as the year progresses. Add softer fuel, a reversal of recent airfare spikes and fading tariff effects, and the hawkish pivot starts to look like insurance the Fed may not need. Europe tells a similar story, where Lagarde is warning about second-round effects while food inflation actually fell sharply in May across the eurozone, the UK and parts of Eastern Europe. The UK ran this exact film a year ago: hawks sounded the alarm on food, taxes and the minimum wage, then watched those fears evaporate by February. The market is positioned for higher and stickier. The contrarian read is that by this time next year, central banks will be quietly preparing the ground to go lower.

That tension is precisely why this week’s data carries weight. We get the first hard read on whether the inflation scare has substance or is, as the doves suspect, already fading.

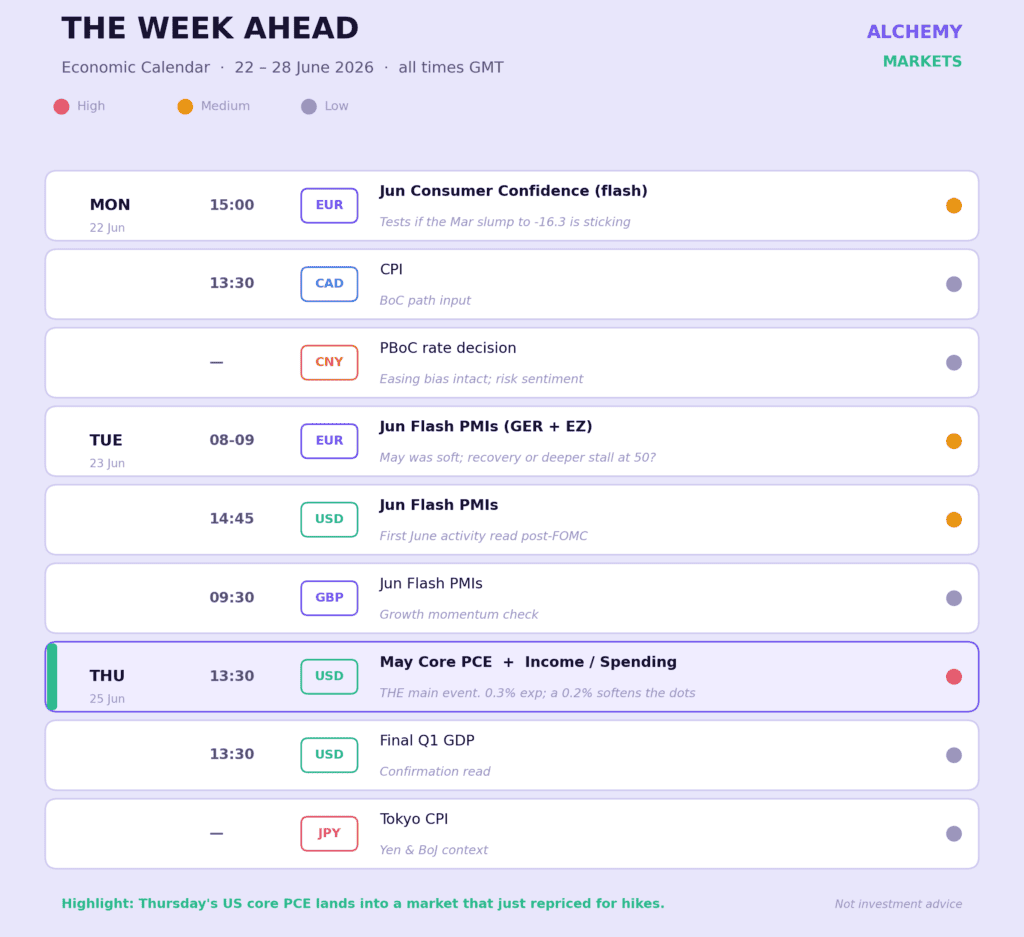

Economic Calendar — Week of 22 to 28 June 2026

The standout is Thursday’s US core PCE, the Fed’s preferred inflation gauge, landing into a market that has just repriced for hikes. Flash PMIs on Tuesday give the first global activity read for June, and eurozone confidence frames the demand side. All times GMT.

Two things to watch on Thursday. First, the savings rate within the income and spending report. It is grinding toward record lows, which hints at consumer stress beneath decent headline spending. Second, the balance of risk on core PCE. The setup from already-released CPI and PPI points to around 0.3% month-on-month, but the softer-leaning details suggest 0.2% is the more likely surprise than 0.4%. A 0.2% would land directly on the dovish side of the Fed’s freshly hawkish framework and force the market-versus-Fed gap back open.

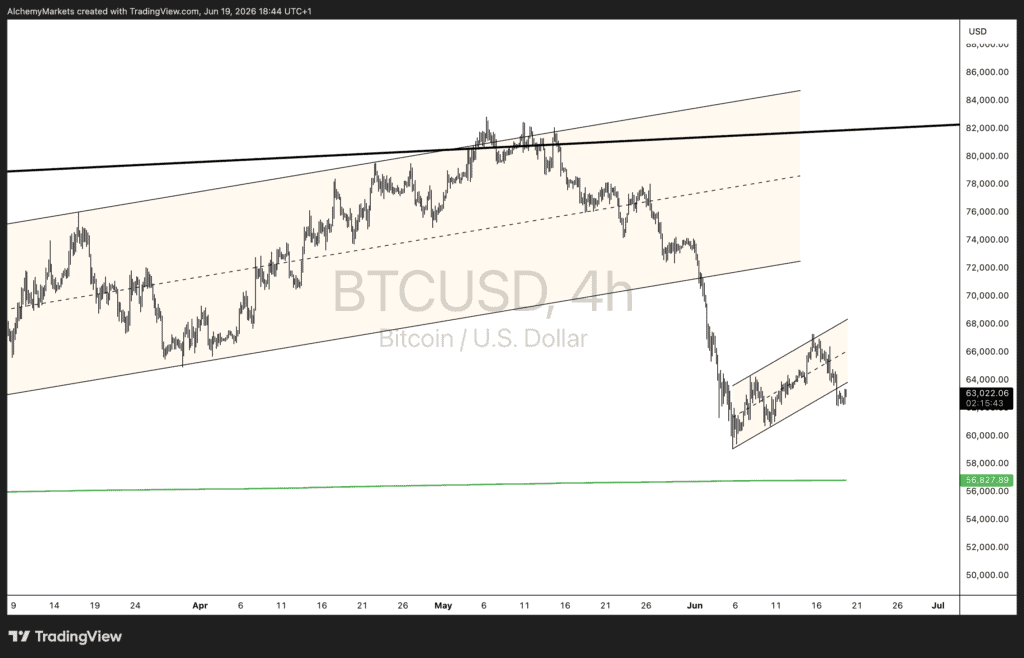

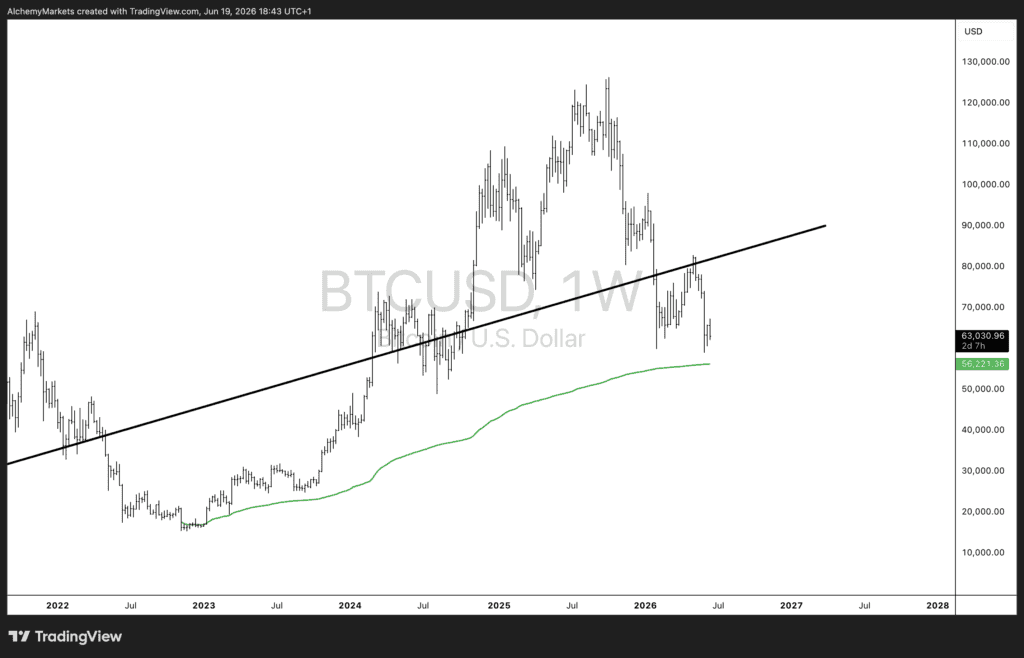

BTCUSD — Breaking Out, But VWAP Is Watching

Bitcoin trades at roughly 62,900 after a sharp June flush. The setup is worth laying out top down, because the lower timeframe story only makes sense against the higher timeframe structure.

Lower timeframe (daily). Price has carved out a small ascending channel off the June lows near 60,000 and is pressing the upper boundary around 63,000. This is a clean short-term breakout attempt from the recovery base. The character of the move has shifted from impulsive selling to a measured grind higher, which is constructive in isolation.

Higher timeframe context (daily and weekly). The problem is what sits overhead. The June break shattered the broad ascending channel that had governed price from the February lows through the May highs near 82,000, and BTC is now recovering from beneath it. That prior channel base, around 72,000 to 73,000, has flipped from support to resistance. More immediately, the anchored VWAP from the cycle lows sits as the line in the sand the breakout has to contend with. Price reclaiming the small channel is one thing; pushing through the VWAP anchored from the lows is the harder test, and that is where I would expect the first genuine stall.

On the weekly, the larger trend structure is still intact. Price holds well above the long-running multi-year ascending trendline and the rising green moving average near 56,000 to 56,500, which has tracked the bull phase since the 2023 base. So the weekly says the primary uptrend is not broken; the daily says we are in a corrective recovery trying to repair the damage from the May top.

The read: this is a breakout off the lows with room to extend on the lower timeframe, but the anchored VWAP and the underside of the broken channel are the natural points where momentum gets tested. A clean reclaim of those levels reopens the path back toward the May range. A rejection there keeps this firmly in the “recovery bounce inside a larger correction” bucket. The weekly trend gives bulls the benefit of the doubt; the daily demands they prove it through VWAP first.