Source: Refinitiv

USD: June Retail Sales and the Fed’s Dovish Outlook

The June US retail sales report came in stronger than anticipated, with headline sales remaining flat month-over-month, defying expectations of a 0.3% decline. This unexpected steadiness was despite notable drops in motor vehicle sales and gasoline station sales. However, more stable segments showed resilience, indicating underlying strength in consumer spending. Despite these positive figures, real retail sales are still approximately 4% below their 2021 peak. This points to slower growth in consumer spending, coupled with moderating inflation and rising unemployment rates, potentially influencing future Fed rate decisions.

The data did little to shake the market’s dovish stance on the Federal Reserve. A rate cut in September is fully priced in, with an additional 65 basis points of easing expected by year-end. The US dollar’s resilience amidst these dovish bets can be attributed to emerging „hedges“ against higher inflation, tariffs, and geopolitical risks, particularly with a Trump re-election looming as more likely after recent events.

Previously, there was a case for short-term USD weakness based on US macroeconomic news. However, current price action suggests a more balanced outlook for the dollar. We could see periods of USD strength over the summer as markets prepare for potential impacts from the „Trump trade“ ahead of the November elections.

Today’s US data calendar includes housing starts, building permits, and industrial production for June. Additionally, the Federal Reserve will release the Beige Book this evening, which might highlight regional job market strains, possibly reinforcing a dovish shift in Fed communications.

We anticipate some stabilisation in USD crosses by the week’s end. The commodity FX sector remains fragile, with the Canadian dollar recently hit by lower-than-expected CPI figures, leading us to predict a 25 basis point rate cut from the Bank of Canada next week, aligning with market expectations.

GBP: June CPI and the Bank of England’s Dilemma

Source: ONS

This morning’s UK CPI report for June indicated minimal progress on the disinflation front. Headline, core, and services inflation remained unchanged from May, contrary to expectations for a slight slowdown. With services inflation stabilising at 5.7% YoY in June, the Bank of England (BoE) is unlikely to see this as justification for further easing ahead of its August 1 meeting.

The pound is trading stronger this morning as markets reassess dovish expectations in the Sonia curve. The current pricing suggests a slight reduction in expected rate cuts for August and year-end. The longstanding prediction of the BoE commencing an easing cycle in August now seems less likely post-CPI report, with markets potentially pushing back expectations for an initial cut to September. Any BoE rate cut could have a significantly negative impact on the pound.

Markets in the UK are also anticipating two 25 basis point cuts in 2024, which aligns with our projection of three cuts in total. With the policy rate at 5.25%, considerably higher than the eurozone’s, the BoE has more room for cuts.

Today’s core CPI reading was expected to be 3.4%, with some economists forecasting 3.6%. The actual 3.5% figure is mildly disappointing but not sufficient to alter the broader outlook of upcoming rate cuts. The likelihood of an August rate cut now seems reduced, with a September move becoming more probable.

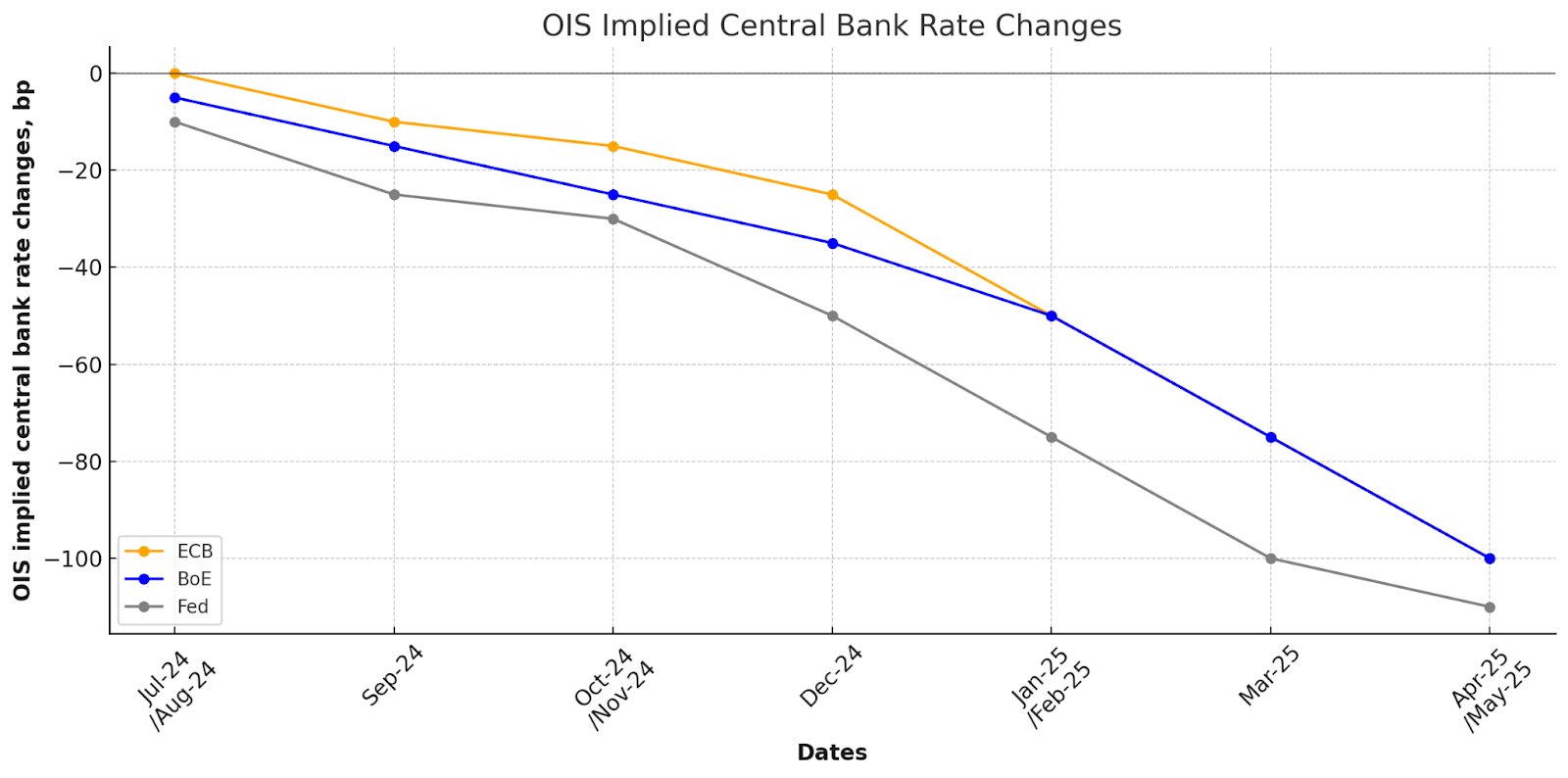

EUR: ECB Rate Cut Expectations and US Spillover Effects

Eurozone rates are now pricing in 48 basis points of cuts for 2024, nearing two full 25 basis point cuts. Our baseline scenario also allows for two additional cuts this year, though current pricing seems somewhat stretched. To validate such pricing, a moderate probability of three cuts should be considered, given the potential for only one cut remaining viable.

Squeezing in a third cut in October appears unlikely, given the European Central Bank’s (ECB) quarterly projections. Governing Council member Knot has expressed a preference for quarterly rate-cut decisions to incorporate updated economic forecasts. A single 50 basis point cut also seems implausible as inflation remains sticky and recession risks low.

Recent US CPI figures have driven the shift towards more ECB cuts in 2024. However, the extent of this influence is limited. In the US, the narrative for rate cuts is gaining stronger momentum, with 63 basis points of Fed cuts priced in by December, indicating potential for further cuts. Consequently, the 2-year USD-EUR swap differential may narrow, as downside risks for the front end of the EUR curve are limited.

GBP/USD Outlook

Given the recent data, GBP/USD is advancing towards the next resistance level at 1.31 – 1.315 with the RSI sitting in the oversold region. If price bounces off the resistance line this can potentially start a formation of a Double Top chart pattern. This movement reflects the broader macroeconomic landscape, with GBP strength tied to the latest inflation data and shifting rate expectations in both the UK and the US. The interplay between dovish Fed expectations and the BoE’s cautious approach to easing will continue to shape this currency pair in the near term.

Conclusion

In summary, the FX market is navigating a complex landscape of diverging monetary policies and economic indicators. While the US dollar remains resilient amidst dovish Fed expectations, the pound shows strength on steady inflation figures. The euro, influenced by both domestic and US economic developments, faces a nuanced path ahead. As always, traders should stay attuned to ongoing macroeconomic data and central bank communications to navigate these dynamic markets effectively.

Check out our yesterday’s Opening Bell: TRIANGLES EVERYWHERE IN THE MARKET WITH DOVISH FED SPEECH