Written by:

- Opening Bell

- July 31, 2024

- 4min read

Inflation Trends and Rate Decisions

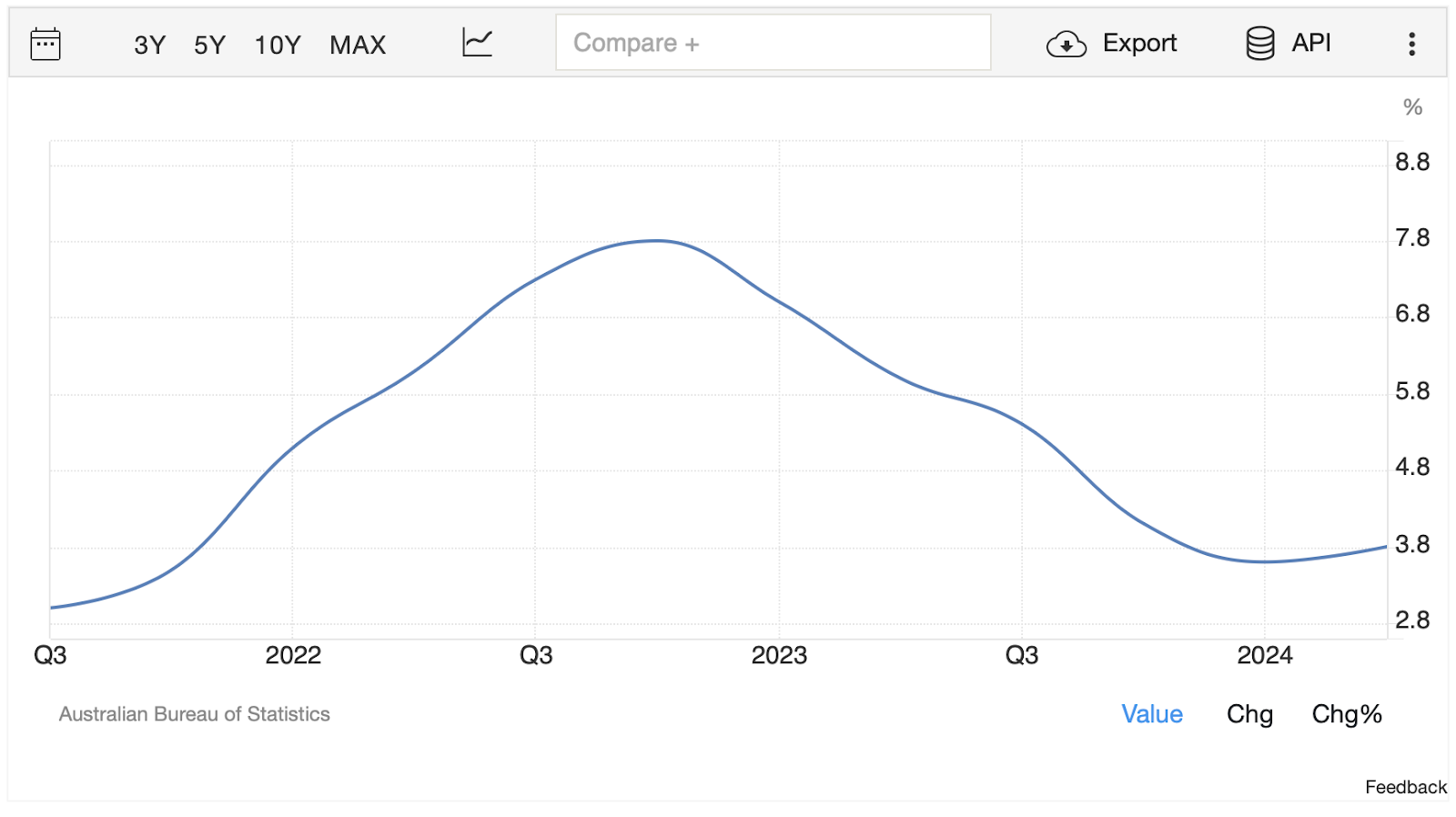

The recent inflation data from Australia presents a mixed bag. Headline inflation remained stubbornly high, rising by 1.0% quarter-on-quarter (QoQ), pushing the annual rate to 3.8% year-on-year (YoY) for Q2 2024, up from 3.6% in Q1. While June’s inflation dipped slightly to 3.8% YoY, this was largely expected and attributed to base effects.

AUD: Inflation Challenge

Monthly inflation figures showed a 0.53% increase, a rate that needs to halve on average to align with the Reserve Bank of Australia’s (RBA) target range of 2-3%. Currently, annualised inflation is hovering between 4.6% and 3.3%, depending on the time frame considered, reflecting a slow but inconsistent decline. The lower six-month measure is expected to rise next month, barring a significant drop in consumer prices as the negative January figure falls out of the annual calculation.

RBA’s Dilemma: To Hike or Not?

The upcoming RBA meeting on 6 August poses a crucial decision point. Some suggest holding rates steady, given the slightly positive core inflation figures, which indicate a possible slowdown in inflationary pressures. However, the continued strength in retail sales—up 0.5% month-on-month (MoM) in June following a 0.6% rise in May—suggests robust domestic demand that could prevent inflation from falling within the RBA’s comfort zone in the near term.

Despite the market’s initial reaction to the inflation data, which saw the AUD weaken as expectations for an August rate hike diminished, the broader economic indicators support a case for tightening. We still see a 25 basis point (bp) rate hike as the most likely outcome to manage inflation expectations and bring the cash rate target to 4.6%.

USD: Fed’s Stance and Market Reactions

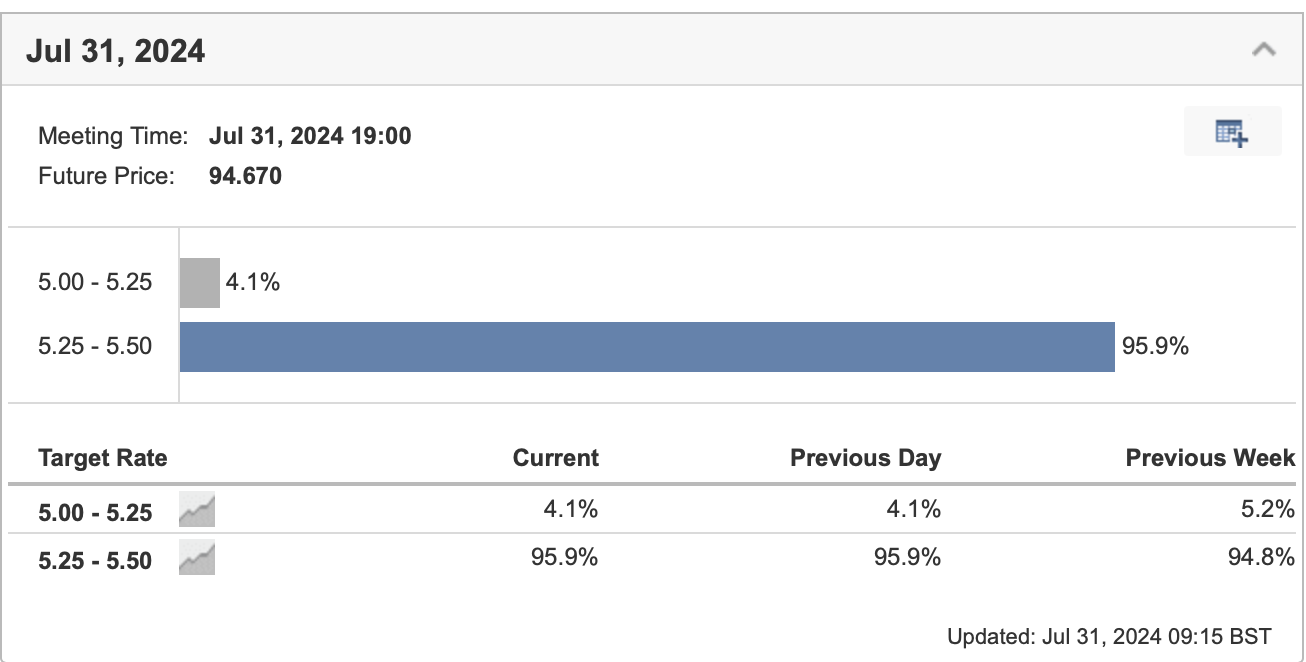

Source: CME

The Federal Reserve’s policy decisions continue to dominate market sentiment. Today’s Federal Open Market Committee (FOMC) meeting is widely expected to maintain the current rates. However, attention is focused on Chair Jerome Powell’s statements, particularly any hints about a possible rate cut in September. This follows a pattern from 2019 when the Fed laid the groundwork for easing measures while acknowledging strong economic performance.

While there is no clear consensus on Powell’s likely remarks, his historically dovish stance might lead to USD-negative headlines. The market is already pricing in a 25bp cut in September, reflecting expectations of a cautious approach from the Fed to avoid undue economic slowdowns, especially given recent positive disinflation trends and a softening labour market.

The dollar faces downside risks today, but Friday’s payroll data could be a more significant driver for FX markets, potentially overshadowing today’s announcements.

JPY: A Surprise Rate Hike and Its Implications

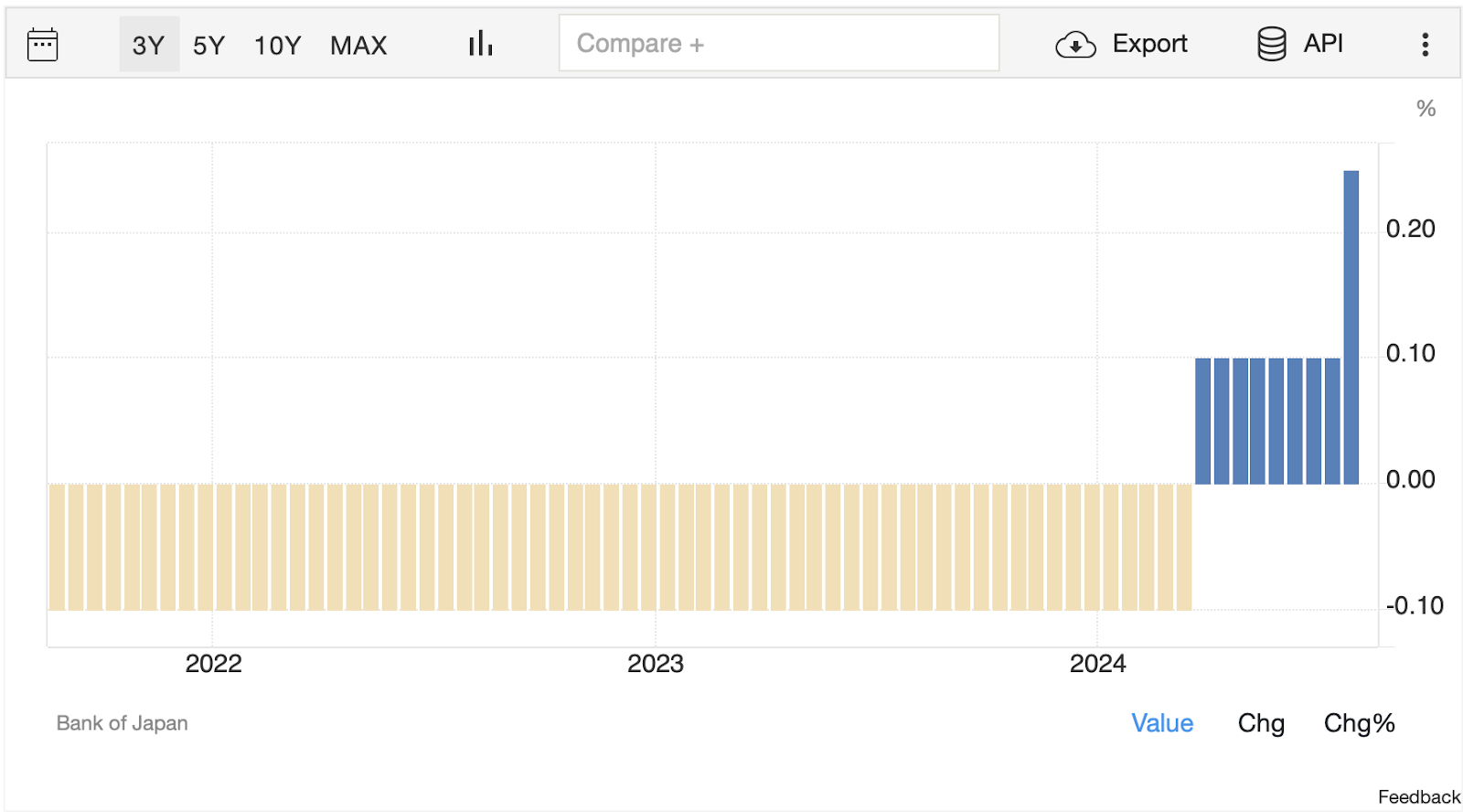

In a surprising move, the Bank of Japan (BoJ) raised interest rates to 0.25%, a decision not widely anticipated by the market. This shift marks a significant policy change, focusing more on long-term inflation projections, now expected to exceed 2.0% by 2025. The BoJ also announced a reduction in bond purchases, set to halve to around JPY 3 trillion by Q1 2026, signalling a tighter monetary stance.

Despite this hawkish shift, the JPY’s reaction was muted, with USD/JPY trading just above pre-announcement levels. This response might reflect market participants’ view of the rate hike as a peak and a potential return to carry trades involving the yen. The market’s subdued reaction could also be due to expectations of more aggressive reductions in bond purchases.

Looking forward, the BoJ’s future actions, particularly any further rate hikes, could significantly alter the yen’s carry trade dynamics. Today’s developments set the stage for potential volatility, especially if the Ministry of Finance’s FX intervention figures spark concerns about the sustainability of current strategies.

Euro: Growth and Inflation Data Impact

The Eurozone recently reported a modest 0.8% YoY growth rate for Q2, slightly better than expected. However, the focus is now on the July Consumer Price Index (CPI) flash estimates, with preliminary data suggesting an uptick in inflation, particularly in Germany, where CPI rose from 2.2% to 2.3%. This unexpected increase, coupled with a contraction in GDP, adds complexity to the European Central Bank’s (ECB) policy outlook.

Core inflation came out at 2.9%, which was expected to slow from 2.9% to 2.8% now potentially fuelling market speculation about future ECB rate cuts. The euro’s recent movements suggest a cautious approach, with support around the 1.0800 level as markets brace for the Fed’s decisions and upcoming payroll data.

Conclusion: Navigating Market Uncertainty

Today’s economic data underscores the complex landscape central banks are navigating. With inflationary pressures varying across regions, monetary authorities face tough decisions on rate adjustments. The next steps from the RBA, Fed, BoJ, and ECB will be crucial in shaping the near-term market outlook, especially for forex traders. As always, investors should stay tuned to economic indicators and central bank communications to gauge market sentiment and potential policy shifts.